How did equity income indexes perform in 2021?

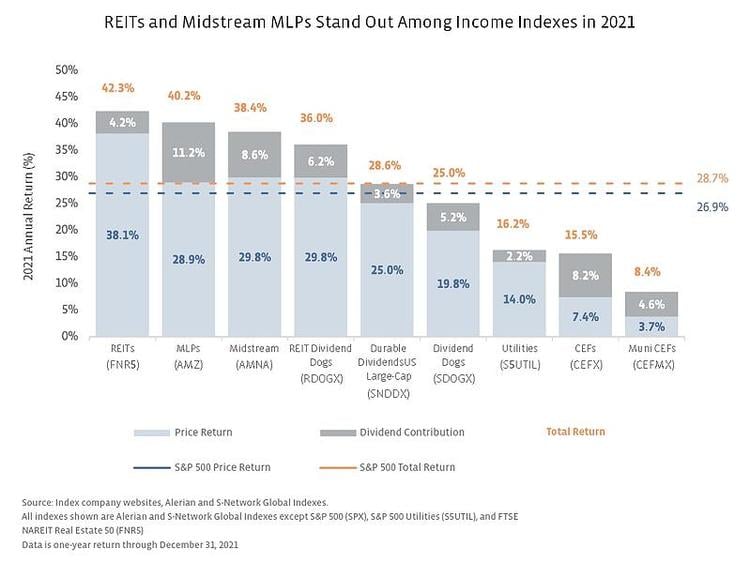

While all of the equity income indexes in the chart below provided positive price return in 2021, performance varied significantly. Given growing inflation concerns over the course of 2021, equity income investments with real asset exposure tended to provide standout performance, with REITs and midstream leading the way. Though Utilities also provide real asset exposure, the sector lagged the S&P 500 due in part to its more defensive characteristics, which are less desirable in a strong year for equities. The diversified equity income indexes below performed relatively in line with the broader market. Closed-end funds (CEFs) rounded out 2021 performance with modest price gains in the single-digits, though price returns tend to be less important as discussed below.

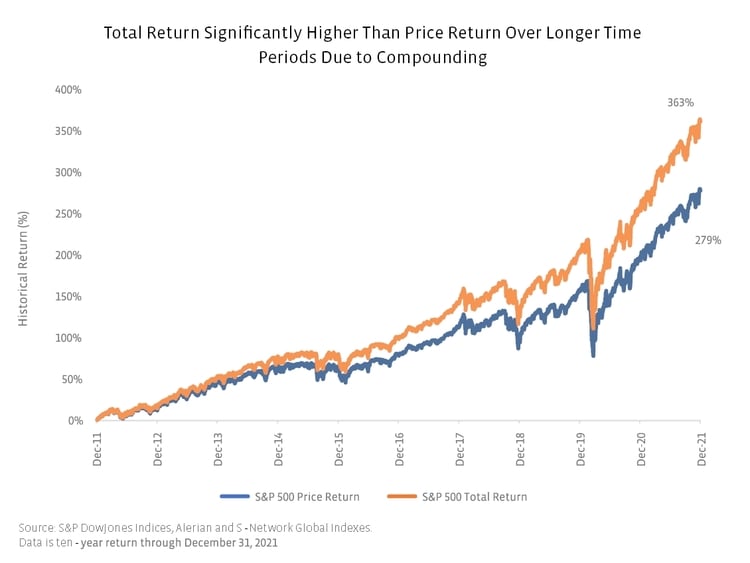

Dividend indexes were in line with the broader market on a total-return basis – Dividend indexes like the S-Network Durable Dividends US Large-Cap Index (SNDDX) and the S-Network Sector Dividend Dogs Index (SDOGX), which provide exposure to companies with higher dividend yields, should generally be evaluated using total returns. On a total-return basis in 2021, SNDDX and SDOGX were about in line with the S&P 500 as seen in the chart below. Some of the variance this year could also be attributed to the equity market rally, which seemed to favor high growth stocks, rather than value stocks. Many dividend paying companies, particularly those with higher yields included in these indexes, have a value tilt. Additionally, the equal sector-weighting of SDOGX provides more exposure to value-oriented sectors like energy and less exposure to growth sectors like information technology than broad market benchmarks.Generous payouts and energy recovery drove midstream outperformance in 2021 – Flush with free cash flow, the midstream space (including midstream MLPs) offers generous payouts and attractive yields in today’s low-yielding environment (see the most recent midstream dividend report here). All else equal, higher payouts can potentially enhance the total return profile. Additionally, midstream participated in a broad energy recovery as commodity prices improved during the year, which resulted in outperformance relative to the S&P 500 on a price-return basis. Midstream significantly outperformed on a total-return basis as it benefited from an 8-11% return contribution from dividends.CEFs focus less on price and more on income generation – Price returns for CEF indexes were lower than other income indexes, but distributions contributed significantly to total return. Price is arguably less important for CEFs than it is for traditional income stocks. Many CEFs pay out the majority of their earnings as distributions and keep their NAV generally stable (and price tracks NAV). Over short time periods, decreases in NAV (and therefore price return) may occur if unrealized earnings are used to fund distributions, which is not uncommon. But long-term, total return should be greater or equal to the distribution rate—otherwise this could indicate that distributions have been eating into the original invested principal.

Current Yields vs. History

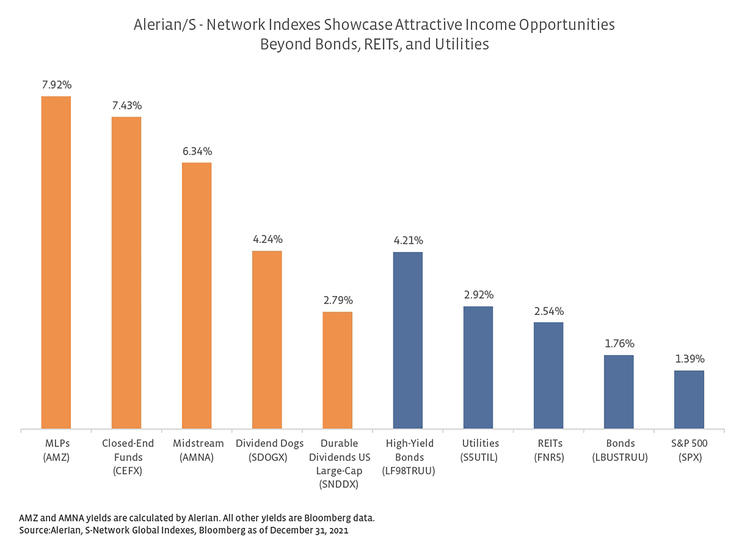

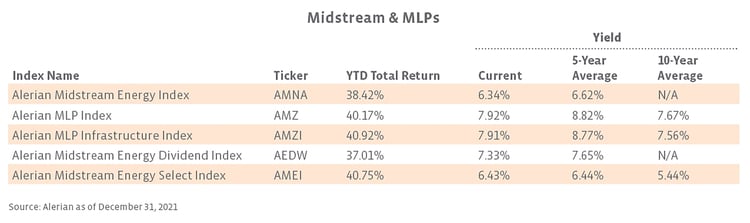

Midstream/MLPs offer attractive yields and provided a strong total return in 2021. Yields are slightly below five-year averages but marginally higher than ten-year averages.

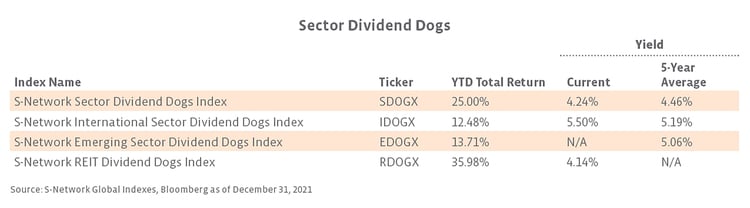

Yields offered by Sector Dividend Dogs are about in line with historical averages, with double-digit total returns in 2021.

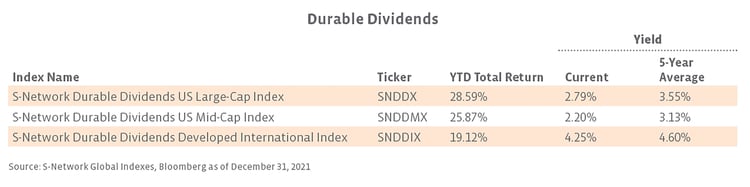

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes.

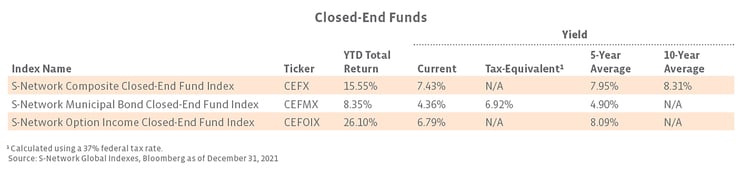

Though current yields are slightly below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio.

Related research:

Income Opportunities with Real Assets

Income Opportunities: Finding Income in an Inflationary Environment

3Q21 Midstream Dividends: No Cuts, Growth Profile Improving

Income Opportunities: High Yields Don’t Have to Mean Low Quality