Insights at a Glance: Framing Current MLP and Midstream Valuations Against History and Past Downturns

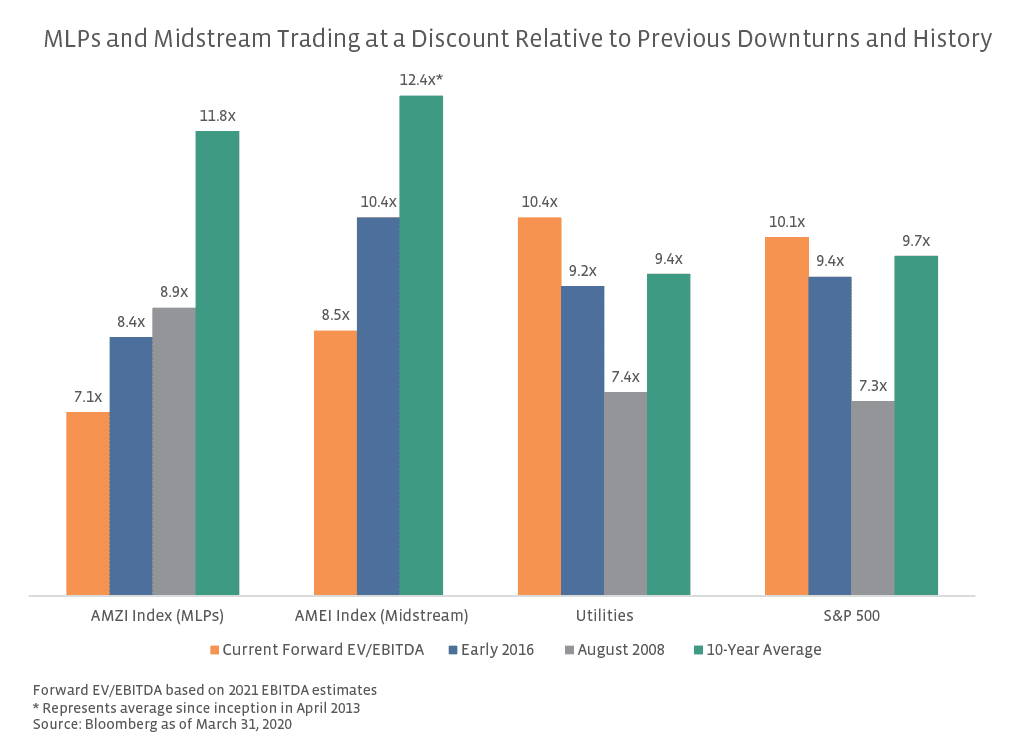

March was a historically tough month for midstream given the start of an oil price war and continued coronavirus uncertainty that together have lowered equity valuations in the space. While uncertainty remains, investors may be seeking further clarity on midstream investment considerations, including valuations. The chart below includes updated EV/EBITDA metrics for the MLPs of the Alerian MLP Infrastructure Index (AMZI) and the MLPs and North American midstream corporations of the Alerian Midstream Energy Select Index (AMEI) as of the end of March, in addition to long-term averages and data from recent energy downturns for historical context. The calculated EV/EBITDA multiple compares the current enterprise value to 2021 consensus EBITDA based on Bloomberg estimates. For more on MLP valuations and why EV/EBITDA is the valuation metric used in this piece, please see this 2019 white paper on MLP valuations.

The overall takeaway from the data is that the valuation metrics for both indexes currently represent significant discounts to history and to recent downturns. The current forward AMZI EV/EBITDA multiple is more than one turn lower than it was at its minimum during the energy downturn in March 2016 and nearly two turns below its trough in August 2008 during the financial crisis. Similarly, the AMEI Index is trading almost 2.0x below its low in January 2016 of 10.4x and almost 4.0x below its average since inception of 12.4×. These metrics help put today’s valuations into context. As an example, consider that the 8.4x EV/EBITDA multiple for the AMZI from March 2016 was recorded shortly after WTI crude reached its relative low of $26.21 per barrel the month prior, levels that are similar to where crude is trading today. Midstream also continues to trade at a large discount to Utilities, represented by the S&P 500 Utilities Index (S5UTIL), and the S&P 500 Index (SPX) on a forward EV/EBITDA basis. Notably, both midstream indexes are trading about four turns below their historical average forward EV/EBITDA multiples, while the valuations for Utilities and the S&P 500 are above their ten-year averages. While some re-rating for midstream may be warranted by changes over the last few years, like the prevalence of MLP distribution cuts, investors have to balance these with other improvements made by the space (read more).

{kind=link}