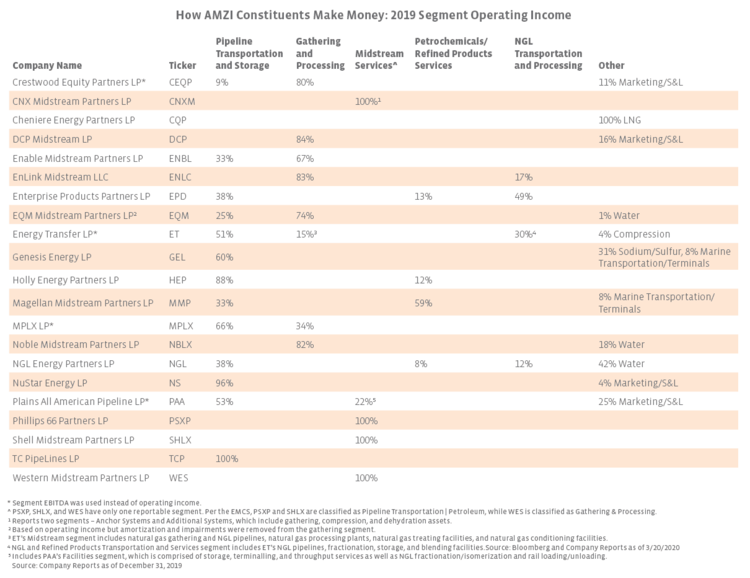

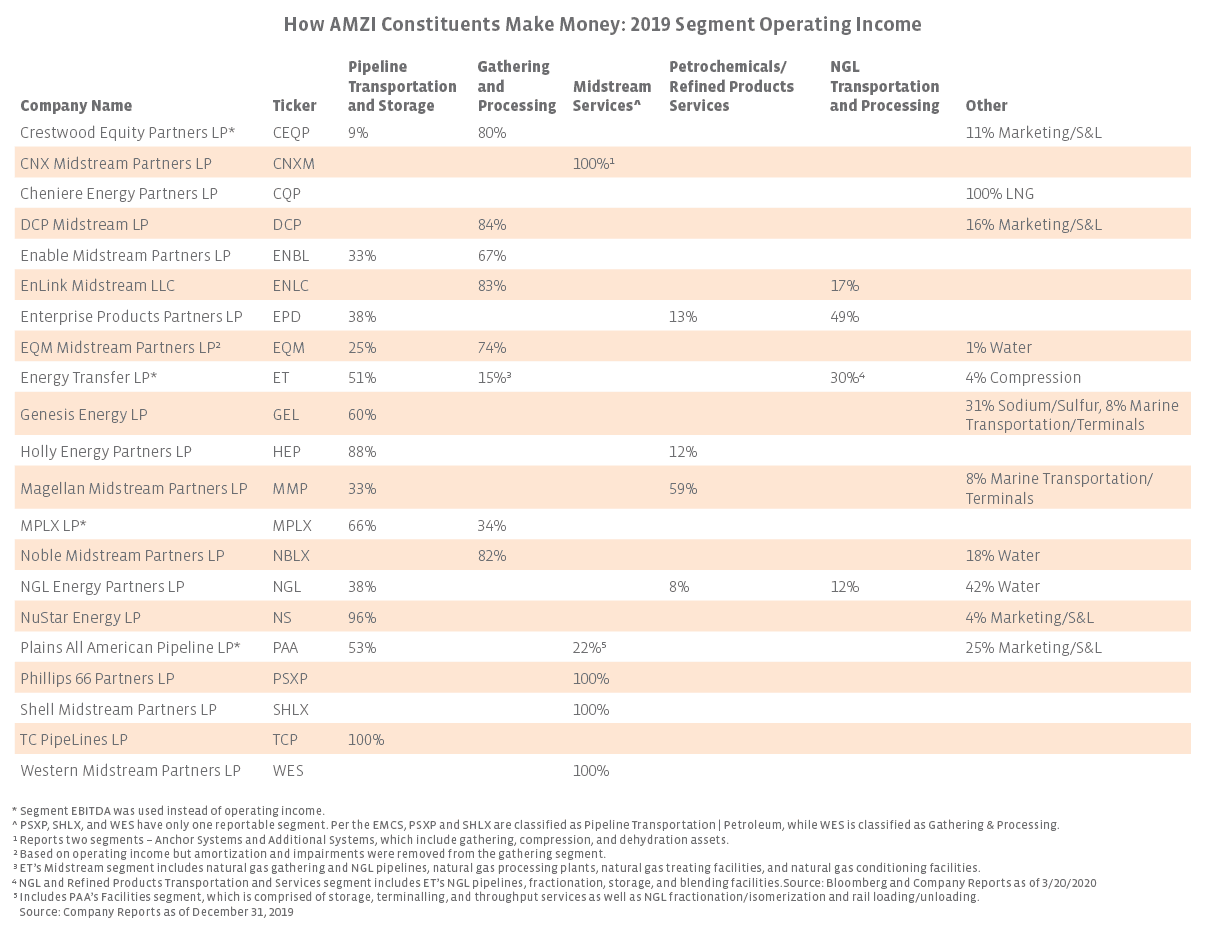

While pipelines are often considered the bread and butter of the MLP space, MLPs provide a wide range of midstream services, from gathering and processing activities near the wellhead to pipelines and terminals supporting distribution of gasoline and diesel further downstream. As discussed last week, most MLPs derive a majority of their cash flows from fee-based activities, which helps insulate midstream from commodity price volatility (read more). One important distinction to note is between gathering pipelines and long-haul pipelines. Gathering pipelines transport hydrocarbons from the wellhead to processing plants, fractionation facilities, or aggregation points for large-diameter pipelines, which then carry the hydrocarbons long distances. Gathering and processing (G&P) activities are often more sensitive to commodity prices as growth in these segments depends on new production, and processing contracts can sometimes carry commodity price exposure (read more). However, G&P companies have tried to limit commodity exposure in recent years by switching to fee-based contracts and hedging. About 25% of the MLPs in the AMZI by weighting are classified as Gathering & Processing. The three constituents that have announced distribution cuts this year – EnLink Midstream (ENLC), EQM Midstream (EQM), and DCP Midstream (DCP) – are all focused on G&P.

The table below shows the breakdown of MLP segment operating income for 2019, with most companies focused on traditional fee-based midstream businesses. Please note that segments were streamlined for comparison purposes, so there may be some variability between the table and company segment reporting. Notably, some of the largest MLPs, such as Enterprise Products Partners (EPD) and Energy Transfer (ET), have diversified operations that are vertically and geographically integrated, allowing them to benefit from activities along the entire midstream energy value chain. Many MLPs also own storage, which may become more desirable given the steep contango in crude markets incentivizing storage (read more). Outside of the normal realm of midstream activities, Genesis Energy (GEL) stands out for deriving 31% of its 2019 operating income from its Sodium Minerals and Sulfur Services segment, which includes soda ash production and sulfur extraction. Plains All American (PAA) reported 25% of its segment EBITDA came from its Supply & Logistics (S&L) segment in 2019 but previously guided to significantly lower S&L EBITDA comprising just 3% of the total in 2020 as crude spreads tighten, particularly in the Permian (read more). While G&P and other activities can have some variability, many MLPs perform core midstream activities that are fee-based and provide some protection in a tough commodity price environment.

Wondering about a company not included in the table below? For company classifications by their primary business activity, please refer to the Alerian Midstream Screener, which classifies midstream MLPs and corporations using Alerian’s Energy Midstream Classification Standard (EMCS).

{kind=link}