Insights at a Glance: Not All Natural Gas Pipelines Are Equal

Since the oil price war began earlier this month, we have focused primarily on crude’s fall and the consequences for midstream. However, with the price of natural gas at Henry Hub hitting a 25-year low last week at $1.60 per million British thermal unit (MMBtu), natural gas pipelines are also a worthy topic of discussion. While natural gas pipelines may seem like they are all the same (i.e. steel in the ground), their customer bases are a key differentiating factor in a low-price environment. Supply-push pipelines are more susceptible to fluctuations in prices since they take away gas from producing areas. For instance, gathering pipelines, which carry gas to processing facilities, are more susceptible to decreased producer activity. Another example is Permian gas pipelines, which carry associated gas from the basin to markets along the Gulf Coast with largely producer customers. Demand-pull pipelines, in contrast, provide gas to demand centers such as utilities, power plants, LNG facilities, and industrial plants. In a lower price environment, demand-pull pipelines benefit from the steadier flows driven by continued utilization from these end customers, even as coronavirus has had some impact on industrial demand. Keep in mind that contract protections may also differ. Acreage dedications for gathering pipelines that grant exclusivity to the volumes in a given area are not as strong as take-or-pay contracts for gas pipelines that provide fees even if the customer does not fully use its committed capacity. To be clear, gathering pipelines can have stronger contract protections like minimum volume commitments – it just depends on the midstream company.

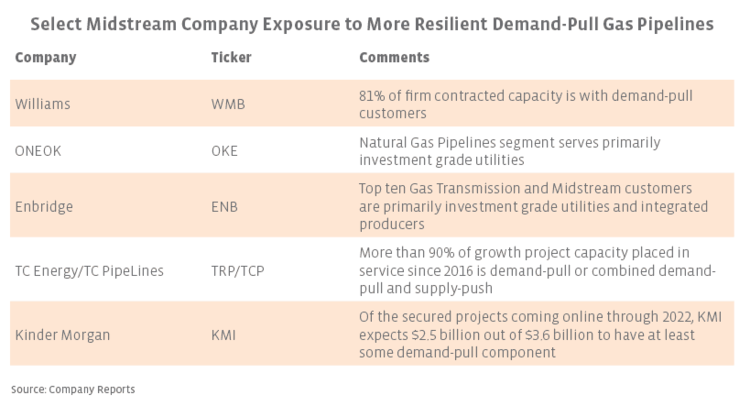

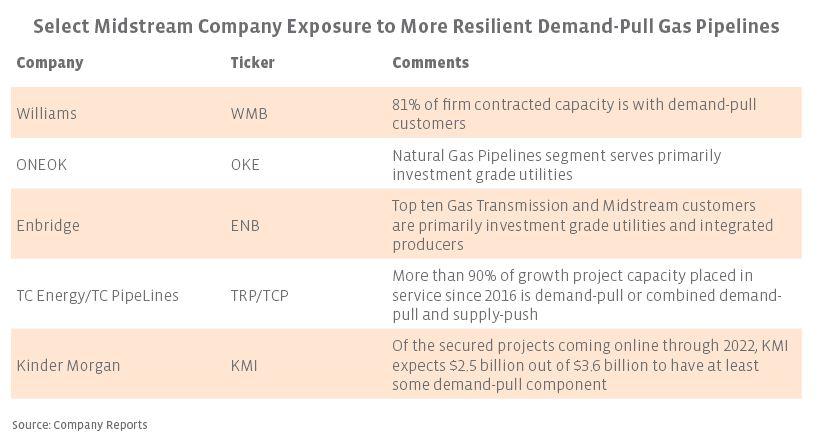

Over the last month, a few companies have provided further disclosures on the demand-pull customer bases for their natural gas pipelines. Williams (WMB) reported that 81% of contracted capacity for its gas transmission business is with utilities, power, industrial, and LNG customers. ONEOK’s (OKE) Natural Gas Pipelines segment primarily serves investment grade utility customers, although a percentage was not provided. Similarly, Enbridge (ENB) said the top ten customers for its Gas Transmission and Midstream segment are primarily investment grade utilities and integrated producers. Kinder Morgan (KMI) lists its natural gas growth projects as demand-pull or supply-push. Of the secured projects coming online through 2022, KMI expects $2.5 billion out of $3.6 billion to have at least some demand-pull component. Since 2016, TC Energy (TRP) and TC PipeLines (TCP) together have placed $4.2 billion in demand-driven or combined demand-pull and supply-push growth projects in service, representing more than 90% of completed growth projects. While we highlighted only a few companies in this piece, large, diversified natural gas pipeline providers can benefit from demand-pull exposure in an environment where natural gas production growth is stalled by low prices.

{kind=link}