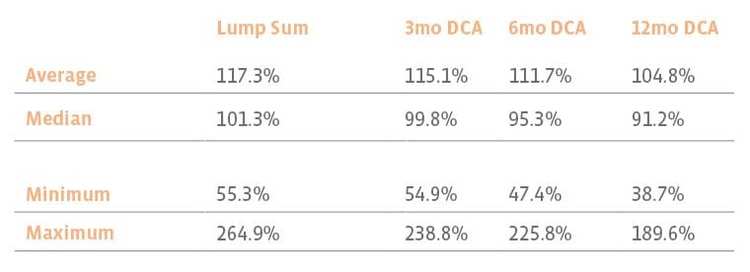

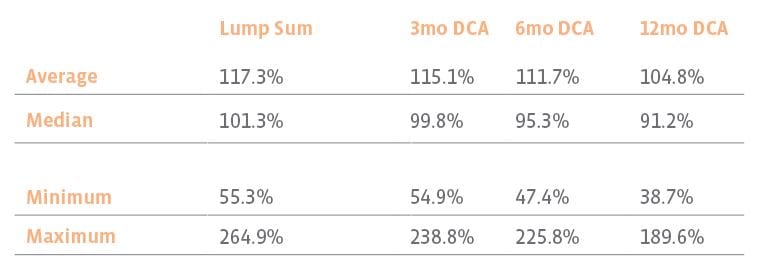

Over time, no matter how or when the MLP investment was made, as long as the portfolio got invested, that portfolio did well.

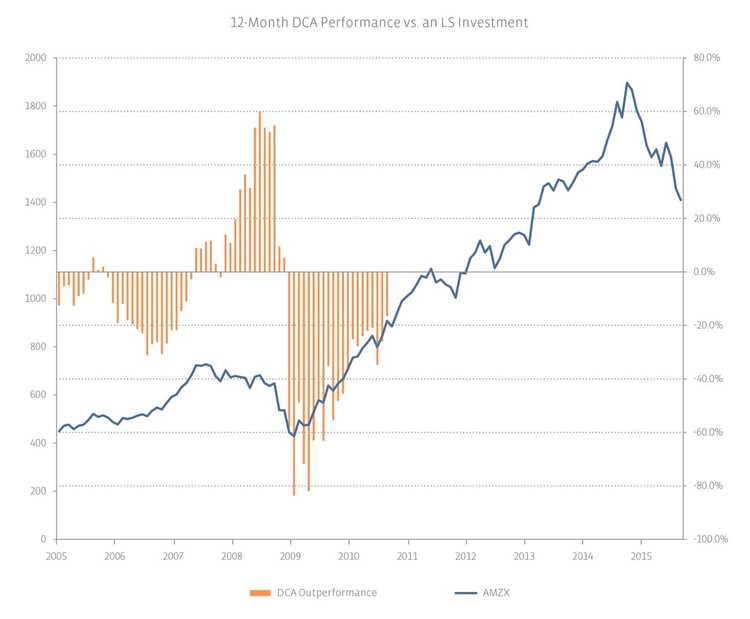

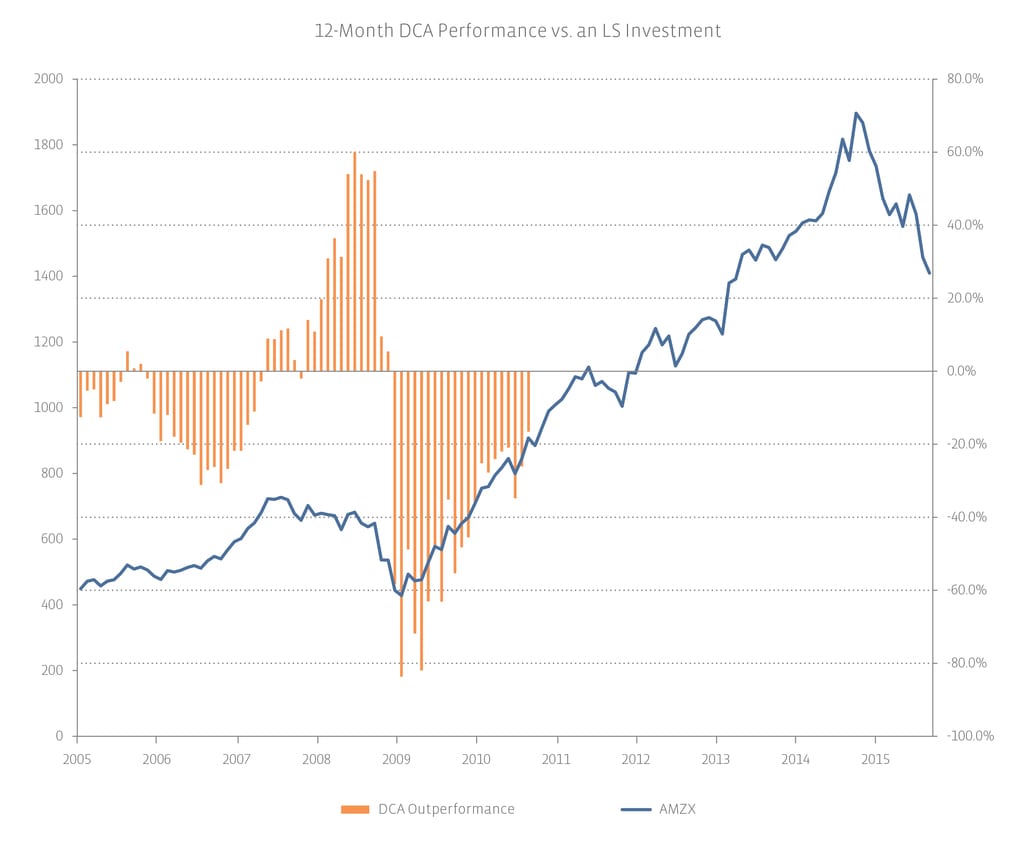

There are, however, notable times when the DCA portfolios outperform the LS ones—specifically, during a major downturn. Unfortunately, if you don’t know when or where the bottom is, it’s also impossible to know whether LS or DCA would be the best choice.

To provide some background: MLP performance started to suffer in mid-2007, before the financial crisis even began. At that time, among other things, institutions had highly levered positions (in MLPs and other sectors) that they began to unwind. It took months for this to begin to impact the banks and the broader financial system, leading to the crisis in mid-2008.

If an investor had used DCA to buy MLPs starting a few months before their July 2007 peak, all the way up until a few months before the December 2008 bottom, she would have significantly outperformed lump sum investors during that time. In other words, if you have been buying MLPs all the way down these past 11 months, take comfort in the fact that at least you didn’t deploy all your capital in that first transaction. Additional solace can be found in fund flows data and sell-side analyst recommendations suggesting that you weren’t and aren’t alone.

If you went all in on MLPs around the peak last fall, it’s worth mentioning that investors who bought in around the last major peak in July 2007, regardless of whether they used LS or DCA, still made between 50% and 96% over a five-year investment horizon.

MLPs are down over 20% year to date. In 2008, they finished the year down over 35%. I hope, for our collective sanity, that MLPs trade up from here and do so in the near term. I am my parents’ daughter, so I believe the right time to invest in MLPs was yesterday. Unless you’re my brother, you’re somebody else’s parents’ child. If you want protection in case MLPs fall further, perhaps DCA investing can help you sleep at night.

{kind=link}

{kind=link}