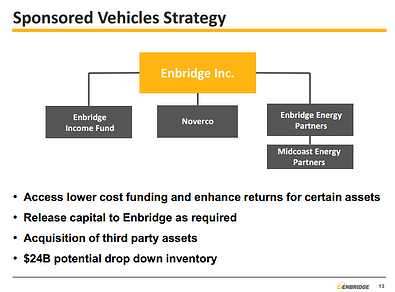

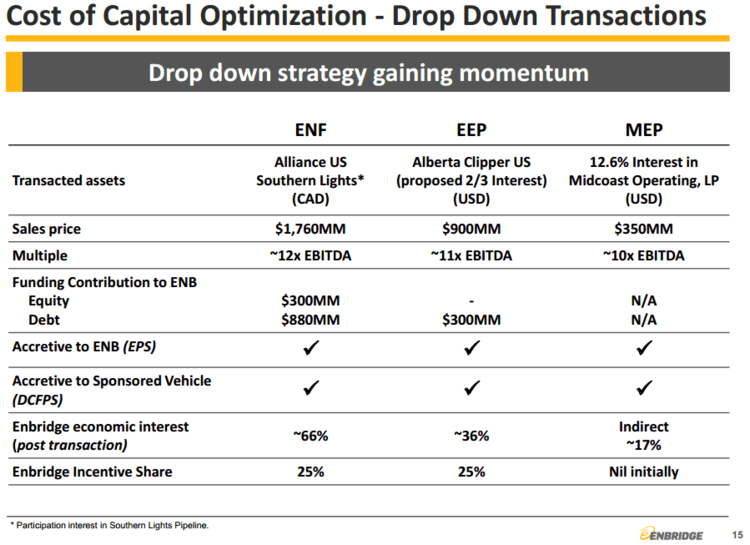

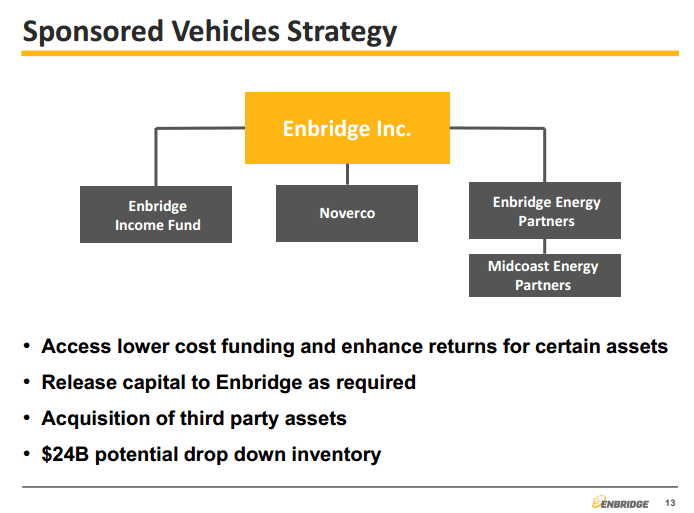

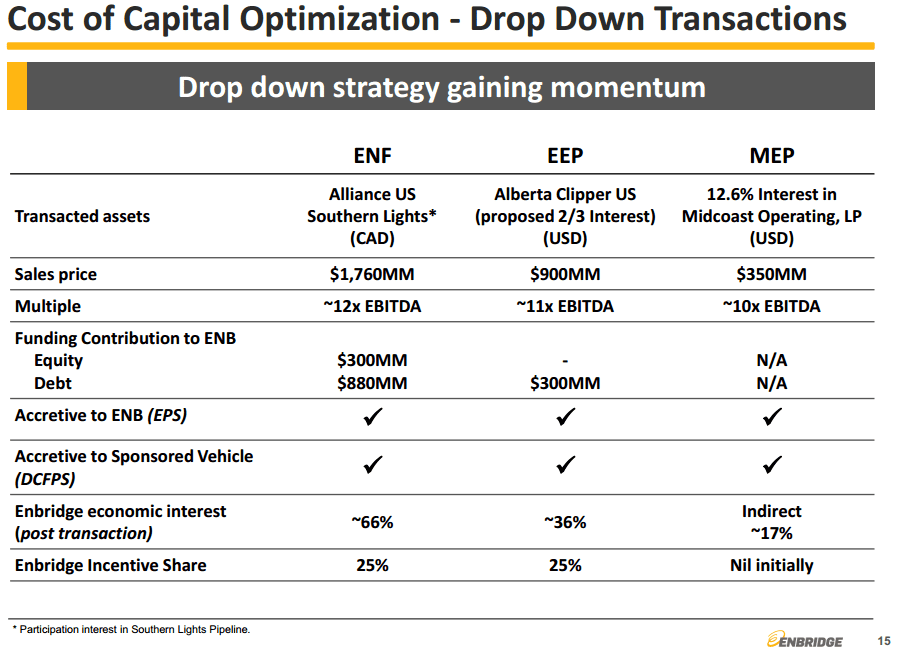

Like Teekay Corporation (TK), Calgary-based Enbridge Inc (ENB) is a parent company with several publicly traded subsidiaries that decided to host an analyst day this week. Unlike TK, however, ENB views its “sponsored vehicles”—Midcoast Energy Partners (MEP), Enbridge Energy Partners (EEP), Enbridge Energy Management (EEQ), and Enbridge Income Fund (ENF)—as low-cost funding mechanisms for the $27 billion capital program it will be undertaking through 2017.

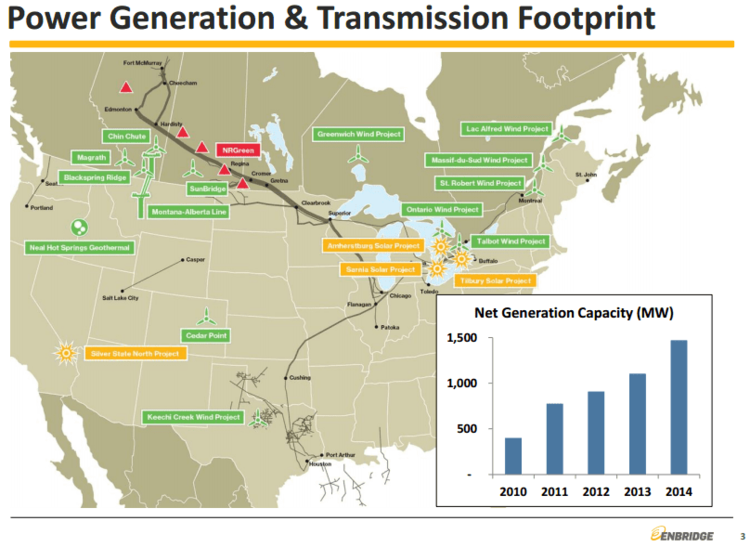

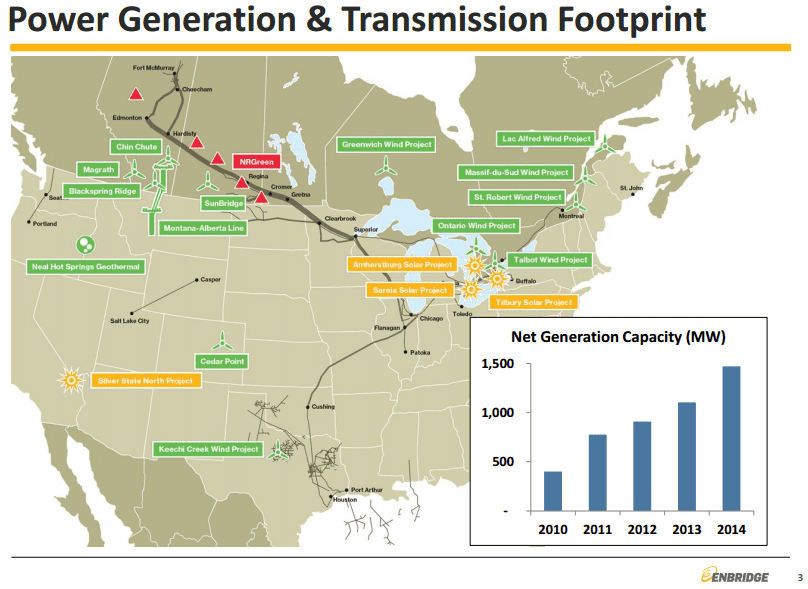

Some US readers may be surprised to learn that ENB, as an energy infrastructure company, has a sizeable portfolio of power generation assets. But research analysts covering the two industries often fall under the same umbrella, as hydrocarbons and electricity compete to heat homes and fuel cars.

As you might expect in an analyst day presentation from a company with a broad footprint across the continent, Enbridge spends a lot of time thinking about the macro drivers that affect its businesses. Here are two examples:

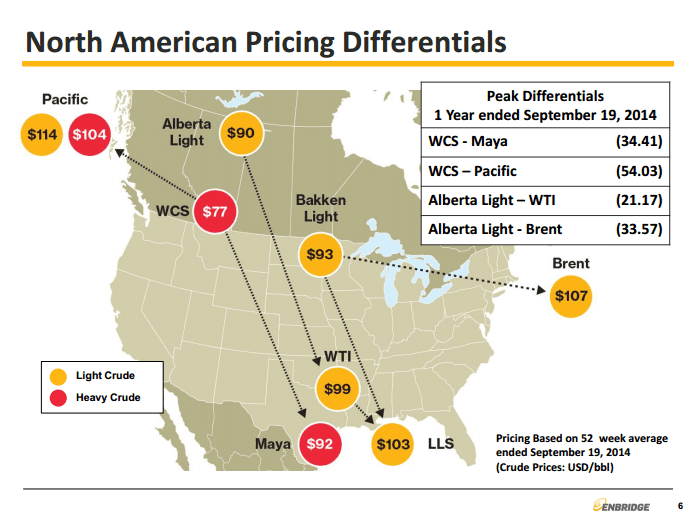

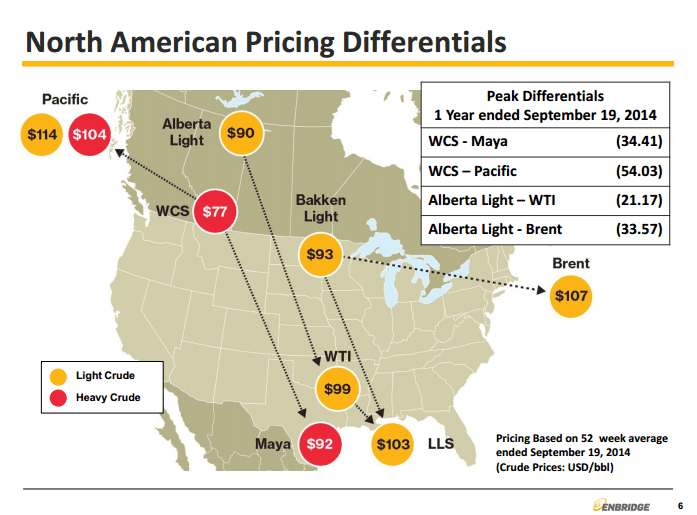

The first shows how pricing drives infrastructure investment. If you can buy a barrel where it’s cheap, and sell where it’s expensive, that difference, less the transportation cost, is your profit. Pipelines are one of the cheapest ways to transport hydrocarbons, making them a very attractive way to close these pricing differentials. Enbridge isn’t interested in speculating on how wide these differentials will get or how long they will persist, but rather on signing up customers who are interested in doing so for a flat fee.

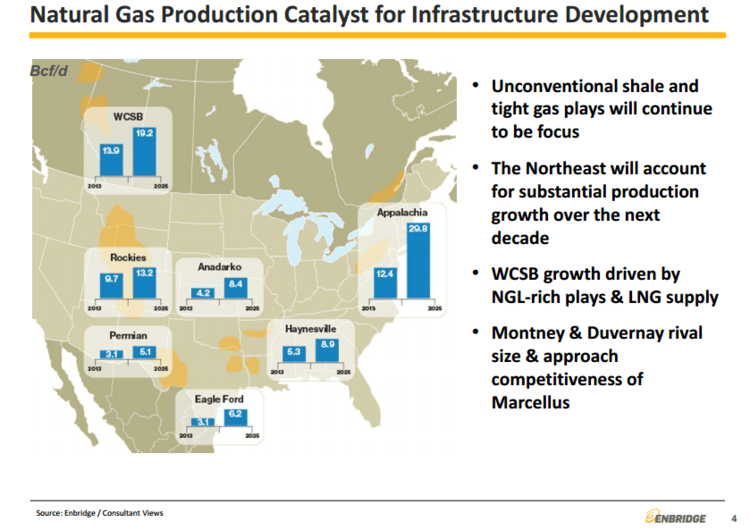

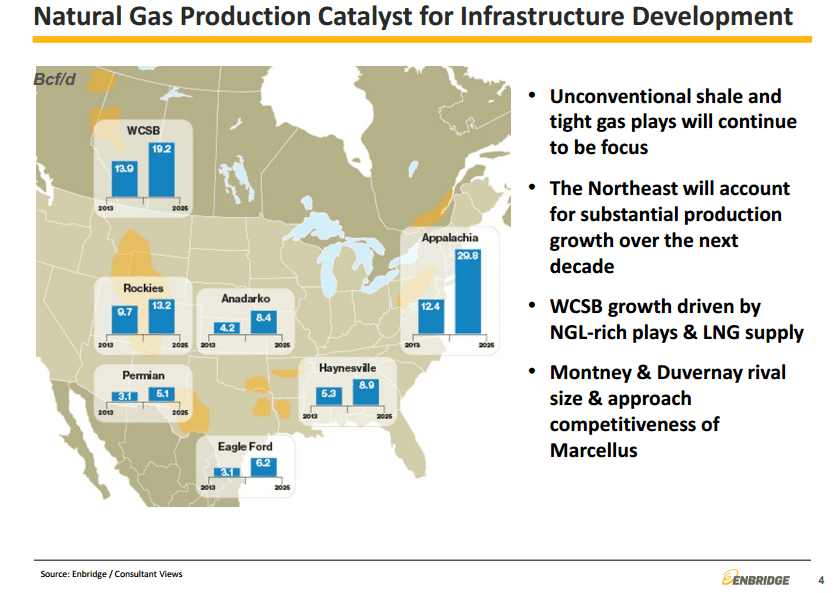

The second shows that natural gas production is expected to grow thanks to hydraulic fracturing and directional drilling, and as such, more pipelines must be built to provide necessary takeaway capacity.

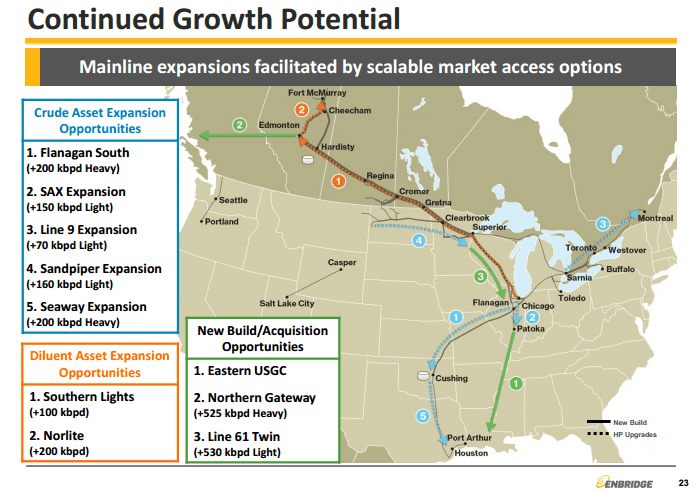

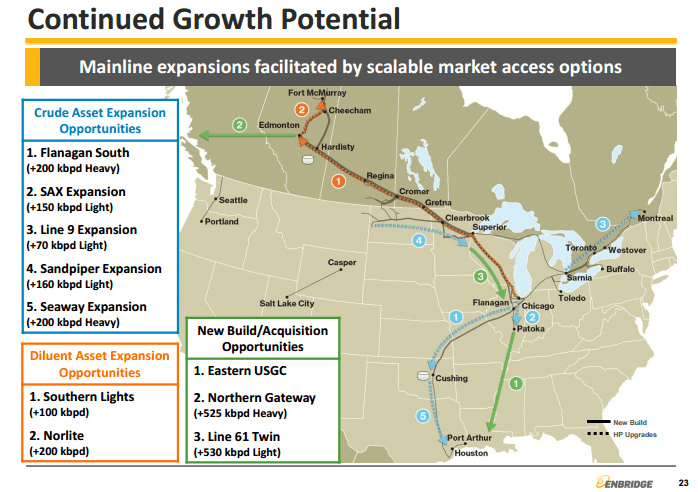

Finally, some investors are still asking whether Keystone XL will ever be built to provide takeaway capacity from the Canadian oil sands. While it has received extensive media coverage, there are other solutions available to producers in the region, like this one offered by Enbridge:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}