As global prices have fallen over the past few months, some buyers have chosen to cancel or defer some cargoes, with 20 or more June loadings expected to be canceled and as many as 45 US cargoes canceled for July. With the US benchmark price at Henry Hub recently overtaken by European prices and sitting nearly even with Asian prices recently, US cargoes have become uneconomic, which in combination with weak demand from buyers has led to cancellations. On its recent earnings call, Cheniere Energy (LNG) management explained that the company allows long-term customers to suspend or cancel cargoes with appropriate notice. In these instances, the company still receives a fixed liquefaction fee, and its marketing arm has the ability to move the canceled volumes in the marketplace. Per Bloomberg, Cheniere reportedly had as many as 30 requested loadings canceled for July compared to at least 10 in June according to the same article. Notably, Cheniere was one of a handful of midstream names to reconfirm prior financial guidance for 2020 (read more), while Cheniere Energy Partners (CQP) reiterated 2020 distribution growth guidance of 5.7% at the midpoint (read more).

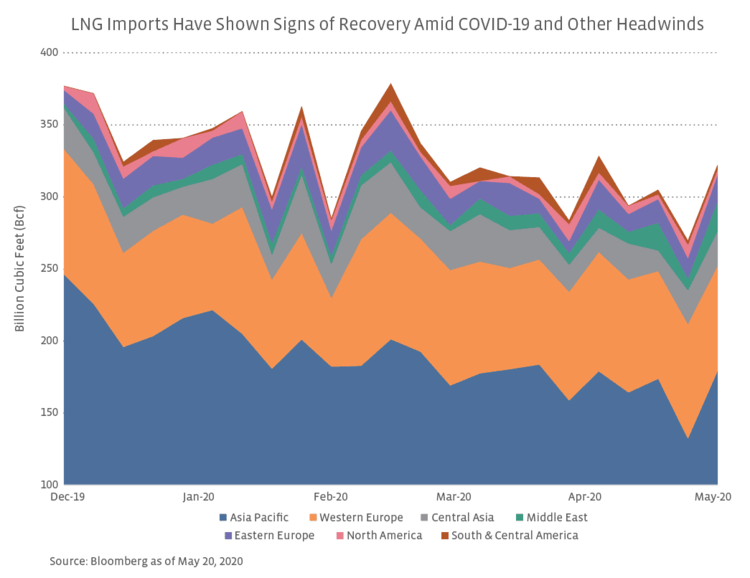

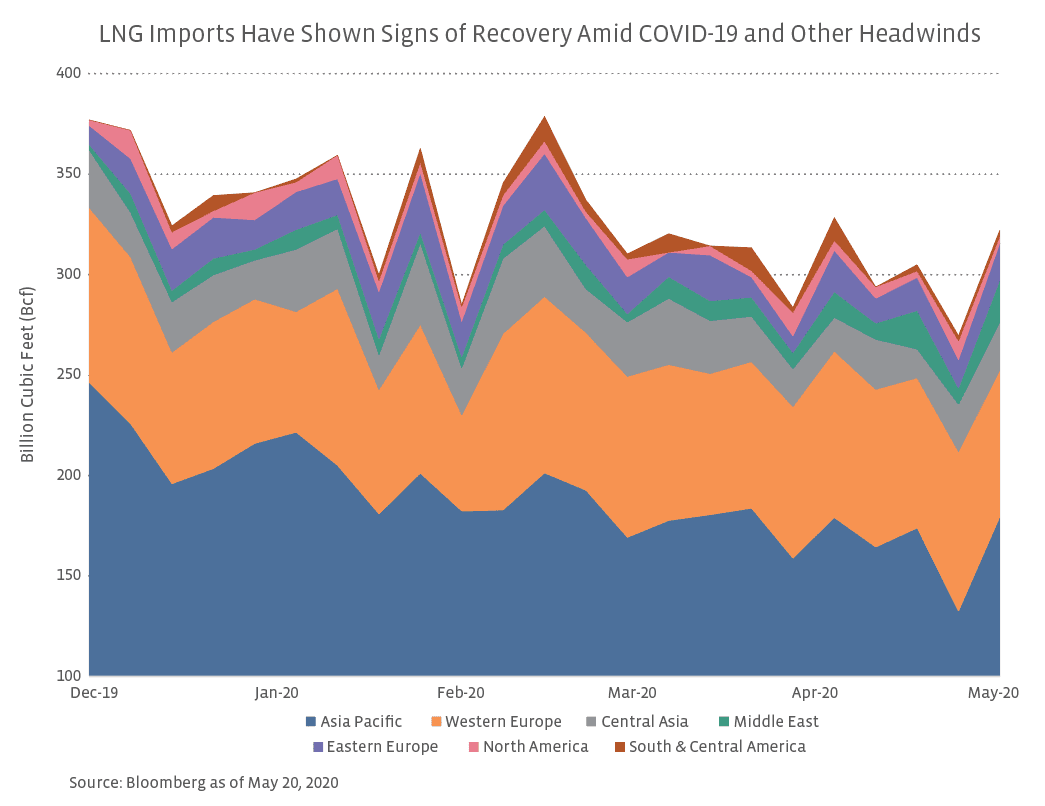

LNG import volumes showing signs of recovery in Asia.

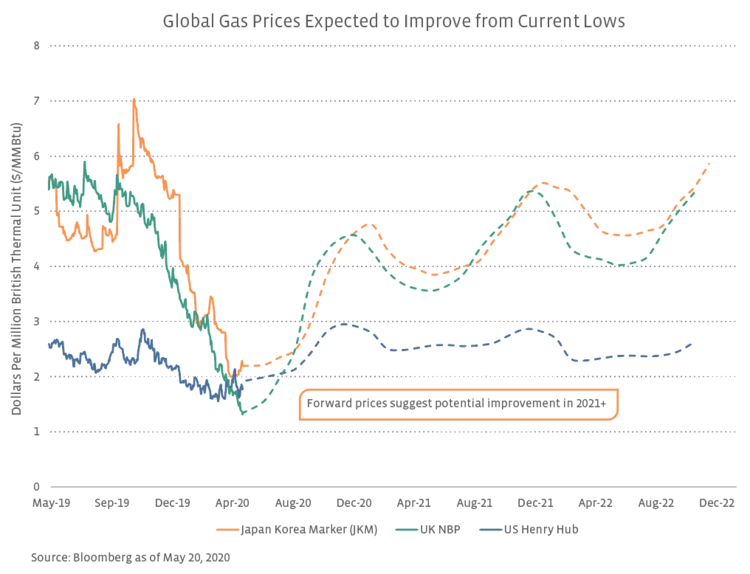

Given the region was impacted by COVID-19 earlier this year, Asia is being closely watched for signs of a potential recovery in energy demand. In March, Chinese LNG importer PetroChina invoked force majeure on some of its LNG import agreements, following the lead of the country’s largest LNG importer CNOOC in early February. While US exporters only had minor exposure to these two companies, the declarations were an indicator of the coming decline in LNG import volumes. As shown in the chart below, LNG imports have declined over the last few months but are showing signs of a potential recovery. Per Bloomberg, total global LNG import volumes were 322 Bcf for the week ended May 15, representing a nearly 20% increase from the previous week and residing near the highest levels since mid-April. China has marginally increased its purchases of US LNG, with three cargoes arriving in April – the first since March 2019 – and four more landing in May. The cargoes arrived in China after the country reportedly granted tax waivers to some LNG importers in early April, which helped alleviate the burden caused by 25% tariffs on US imports that were implemented last year. India, which has imposed COVID-19 restrictions on a timeline similar to the US, has started to see gas demand recover slowly as economic activity resumes. In general, purchases of LNG by Asian and European countries at low prices are likely to be capped by storage constraints as inventories continue to be elevated. In a recent presentation, an analysis by Cheniere showed European gas storage levels remain near record highs as imports have been robust this year against declining demand.

Where does the upcoming wave of US LNG projects stand amid current market conditions?

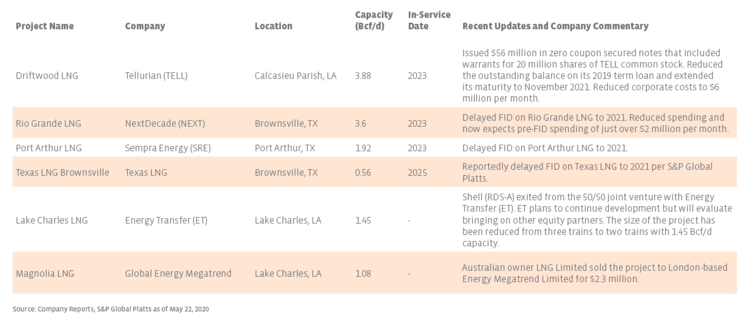

As companies continue to progress LNG projects, several have provided updates in recent weeks (see table below). Project development has been further complicated by uncertainty related to the coronavirus and the continuation of market headwinds. Notably, NextDecade (NEXT) and Sempra Energy (SRE) opted to delay making a final investment decision (FID) to 2021 for their respective projects, Rio Grande LNG and Port Arthur LNG. SRE had previously expected to take FID in mid-2020, while NEXT was targeting FID in the first quarter this year. On its 1Q earnings call, SRE cited the current market environment for its delay but said it was well positioned to advance the project. While Tellurian (TELL) has not announced any formal changes to its project timeline for Driftwood LNG, a spokeswoman recently said it would be hard to say when the company could reach FID on the project in the current environment. Both NEXT and TELL have also taken steps to secure liquidity by reducing costs and securing additional financing to pay down their term loans as they work towards FID on their respective projects. Other companies continue to operate on their previous timelines or have not yet released updates. Cheniere did not formally change its FID target for Corpus Christi Stage III, indicating on its 1Q earnings call that it expects the expansion to achieve FID in 2020 or 2021 dependent on securing commercial agreements.

The long-term fundamental thesis for LNG remains intact.

For now, the focus for LNG exporters is on weathering the current downturn, with contract protections certainly proving helpful. Looking ahead, there may be some reasons for optimism. Recent LNG demand erosion is likely temporary and expected to recover as governments loosen restrictions related to COVID-19. Over the long term, there is a fundamental case for growing LNG demand given its increasing use in developing economies and as a replacement for coal in power generation. While some projects will successfully come to fruition, others are at a greater risk of being delayed further or tabled completely, which is likely to tighten the supply-demand balance in the mid-2020s as additional LNG export capacity becomes necessary to meet growing demand. Companies that can successfully advance projects on a steady timeline and secure customers can put themselves in position to take advantage of these trends.

{kind=link}

{kind=link}

{kind=link}