AMNA provides broad midstream representation.

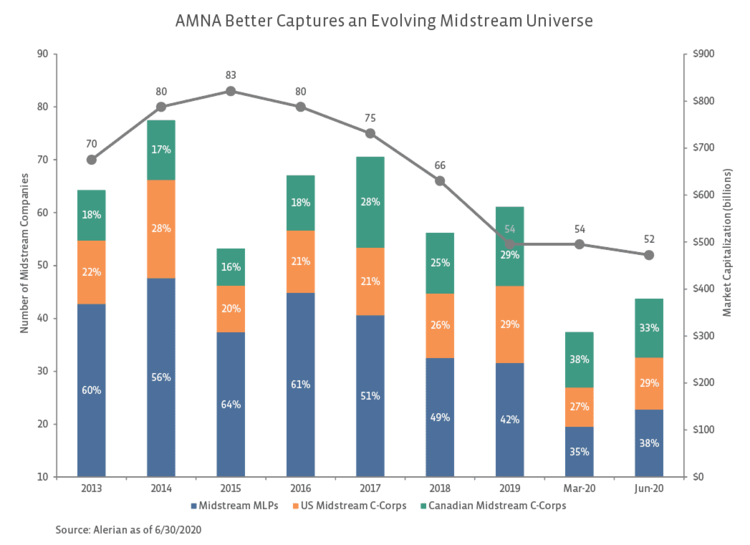

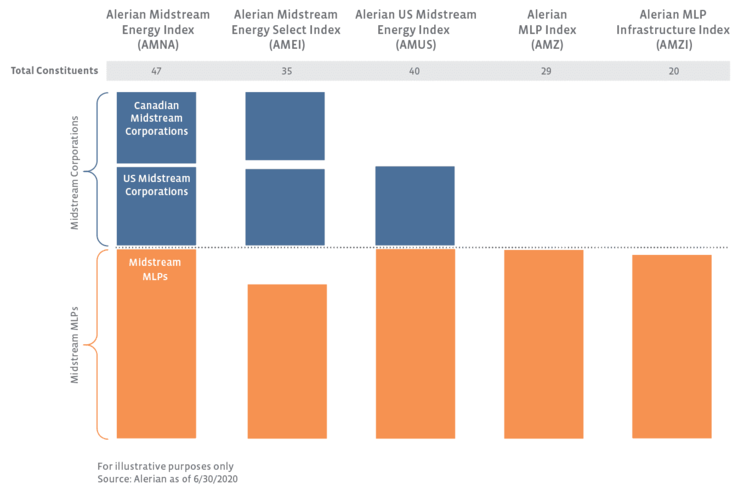

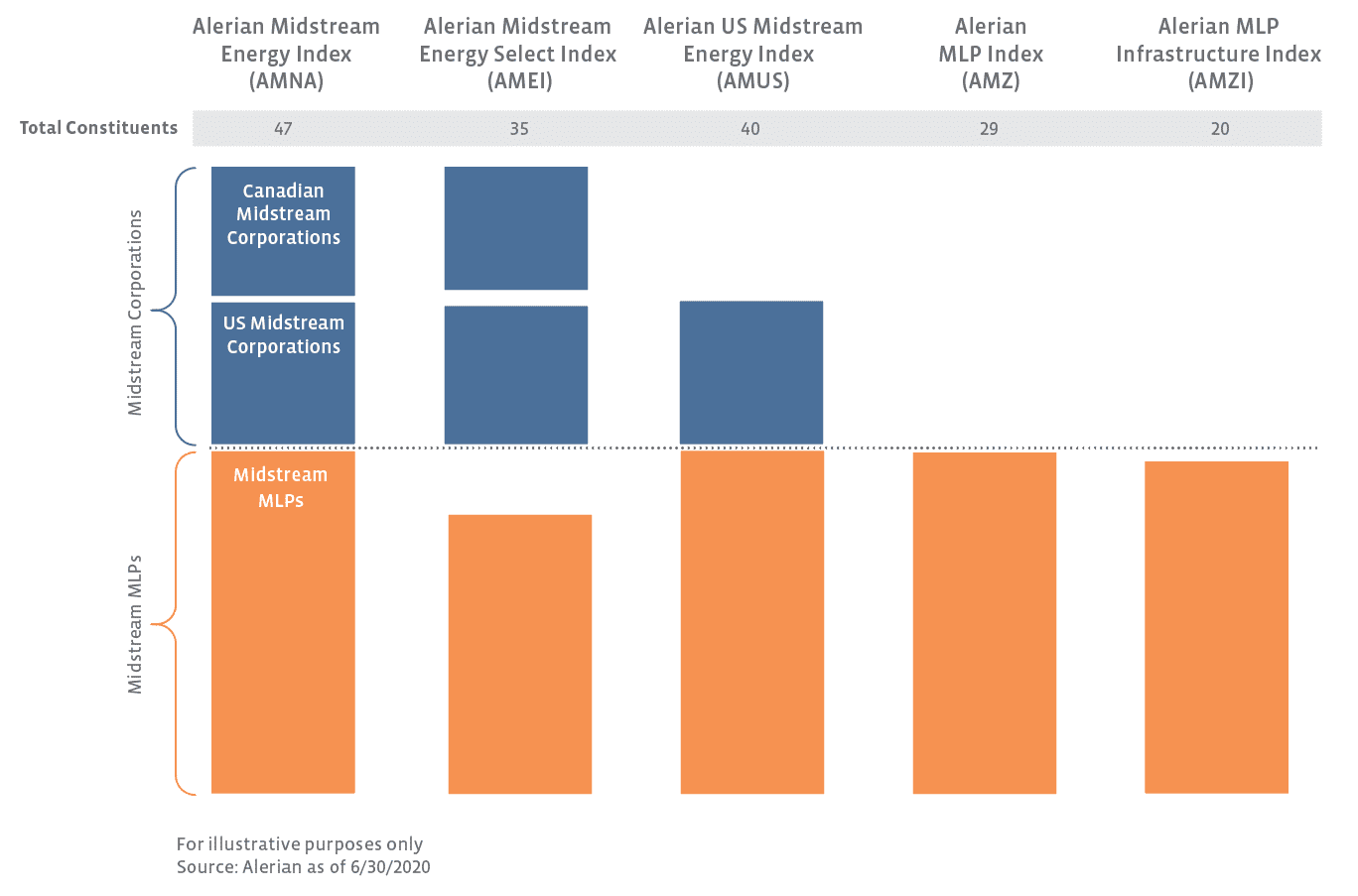

With the shift in the makeup of the midstream universe, the Alerian Midstream Energy Index (AMNA) was launched in June 2018 to provide superior sector representation, as shown below. (For an explanation of Alerian’s different indexes, please see this note.) The AMNA index includes MLPs as well as midstream corporations with principal offices in the US and Canada and has a modest liquidity requirement. Constituents must earn the majority of cash flows from midstream activities, which include Gathering & Processing, Liquefaction, Pipeline Transportation, Rail Terminaling, and Storage. As of June 30, 2020, AMNA had 47 constituents compared to 52 total companies in the universe. The index is weighted by float-adjusted market capitalization with a 10% cap.

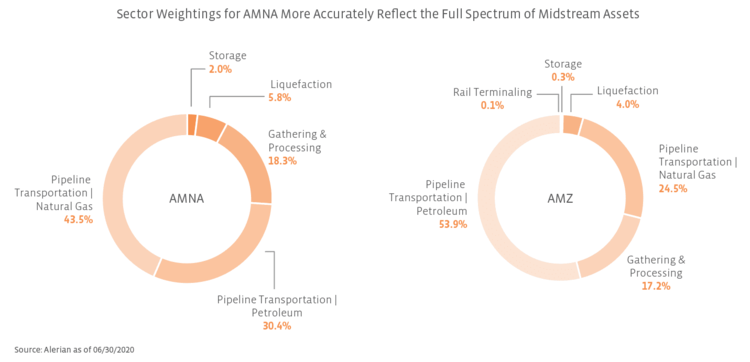

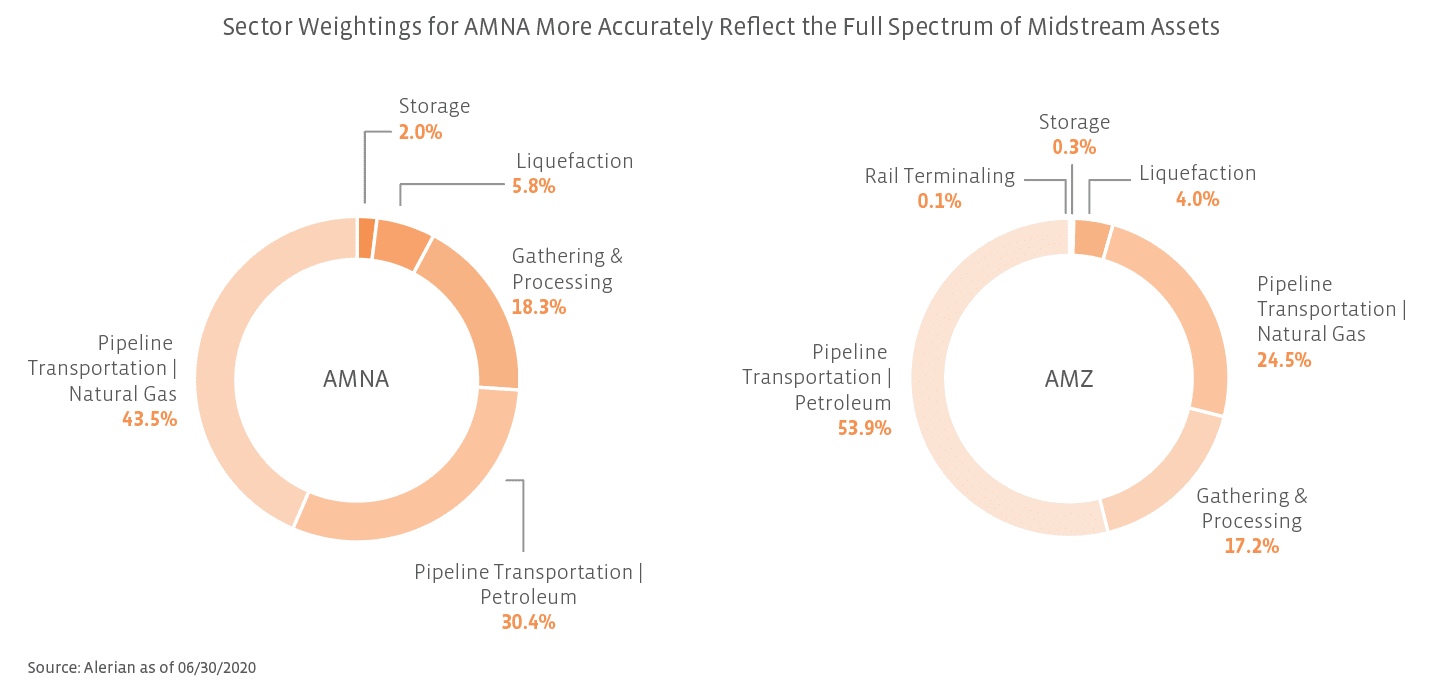

While there is a 10% cap on individual constituents, the AMNA Index does not have limitations on the portion of the index allocated to MLPs. This differentiates AMNA and its US subset, the Alerian US Midstream Energy Index (AMUS), from other Alerian indexes. If an investment vehicle such as a mutual fund or exchange-traded fund owns more than 25% MLPs, the fund will be taxed as a corporation (read more). Given these tax guidelines, benchmark indexes intended for these RIC-compliant funds limited MLP exposure at the cost of more accurate sector representation. AMNA also provides more comprehensive exposure to the full spectrum of midstream assets. MLP-only indexes tend to be lacking in exposure to interstate natural gas pipelines and have a greater exposure to companies involved in the pipeline transportation of petroleum, as shown in the comparison of sector weightings for AMNA and AMZ below.

Canadian midstream companies should not be overlooked.

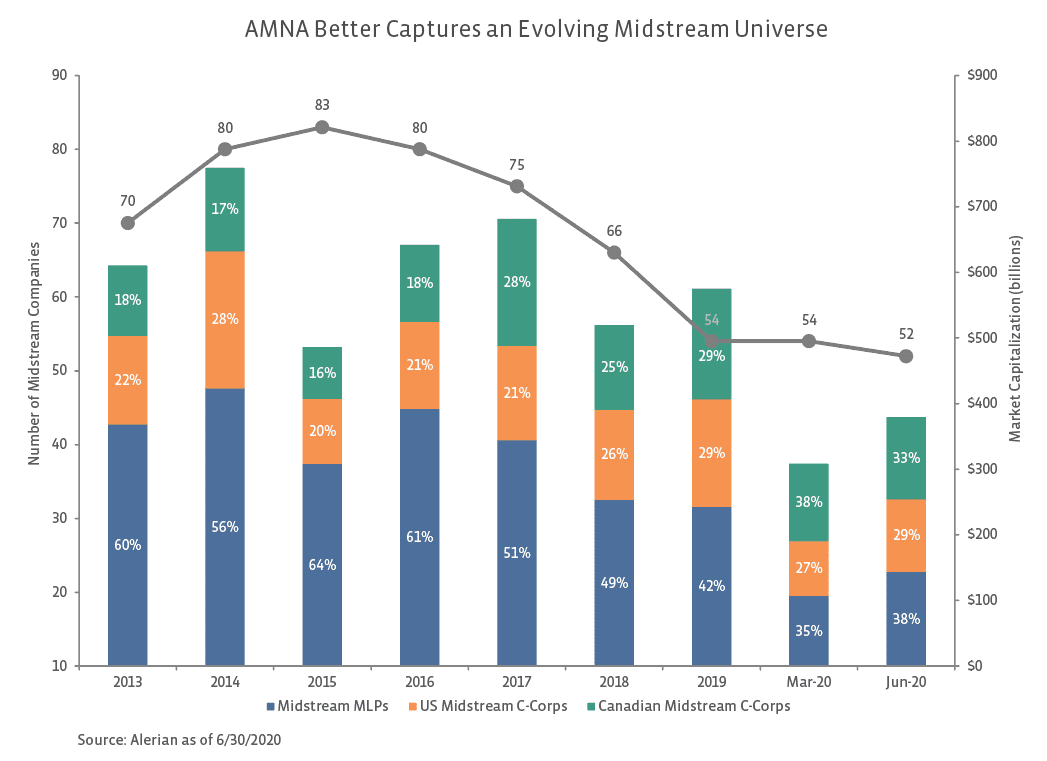

The US and Canadian energy markets have become increasingly intertwined. Canada is the biggest provider of energy imports to the US, and Canada is the second-largest customer for US energy exports after Mexico. In addition to market integration, there is also significant cross border asset ownership by Canadian and US midstream companies. Furthermore, after the severe volatility to start this year, Canadian corporations accounted for the greatest share of the universe at the end of March 2020 (read more). While MLPs have since overtaken Canadian corporations in terms of market cap share, Enbridge (ENB) and TC Energy (TRP) are the largest midstream companies by market cap. Clearly, Canadian midstream corporations should not be overlooked. However, for those investors limited to owning US companies, the Alerian US Midstream Energy Index (AMUS) would be a more relevant benchmark.

AMNA exemplifies the benefits of an allocation to midstream.

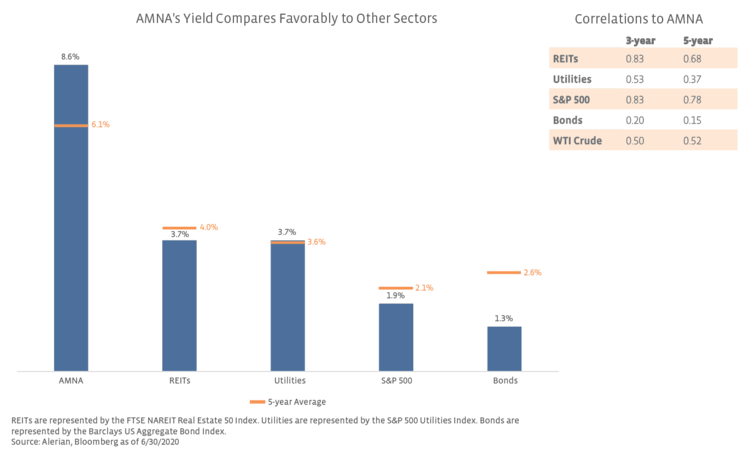

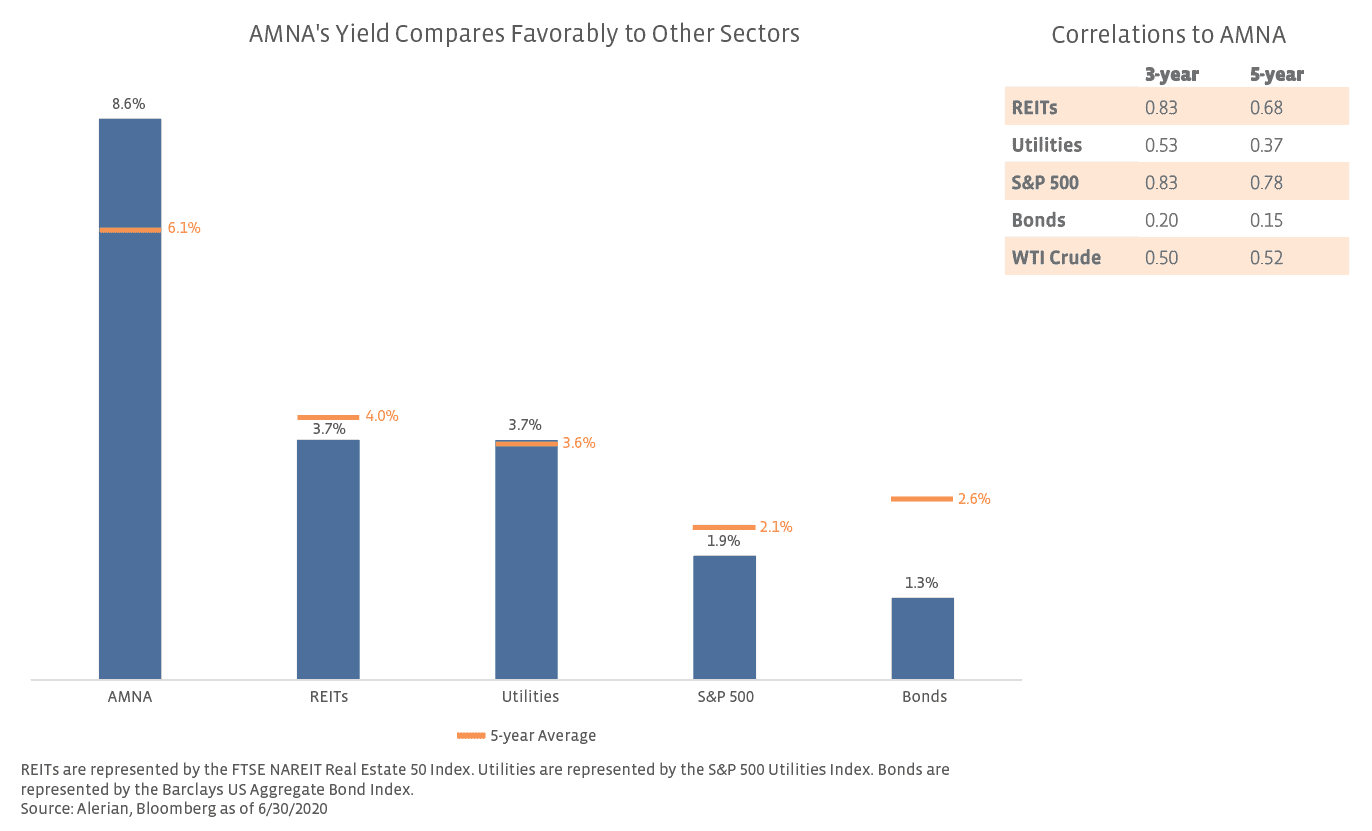

Given its broad representation, the AMNA Index can be useful for evaluating the benefits of a diversified allocation to energy infrastructure. Investors have historically been drawn to midstream for generous income with yields exceeding those of other income-oriented investments, as shown below. Despite elevated yields relative to history given macro headwinds (read more), it is important to note that companies with investment-grade credit ratings represented 83.0% of the AMNA index by weighting as of June 30, 2020. Additional benefits of an energy infrastructure allocation include real asset exposure, more defensive energy exposure given the fee-based nature of the midstream business model, and diversification. An allocation to midstream can enhance an income portfolio by increasing yield while further diversifying the portfolio given modest correlations with utilities and bonds, as shown below. Additionally, MLPs are not included in broader market indexes, which can provide another element of diversification.

As the midstream universe has evolved, there have also been a number of positive changes at the company level across the space in recent years. Midstream has reduced its dependence on equity capital markets and shifted towards self-funding equity growth capital. The vast majority of MLPs have eliminated incentive distribution rights from their structures, simplifying their businesses, lowering their cost of capital, and improving corporate governance. The energy infrastructure space has also taken steps to improve Environment, Social and Governance (ESG) reporting, with several companies providing annual sustainability reports (read more).

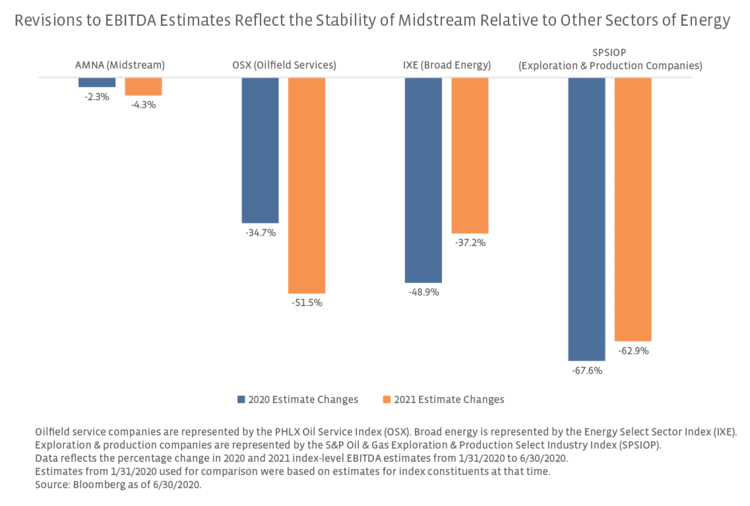

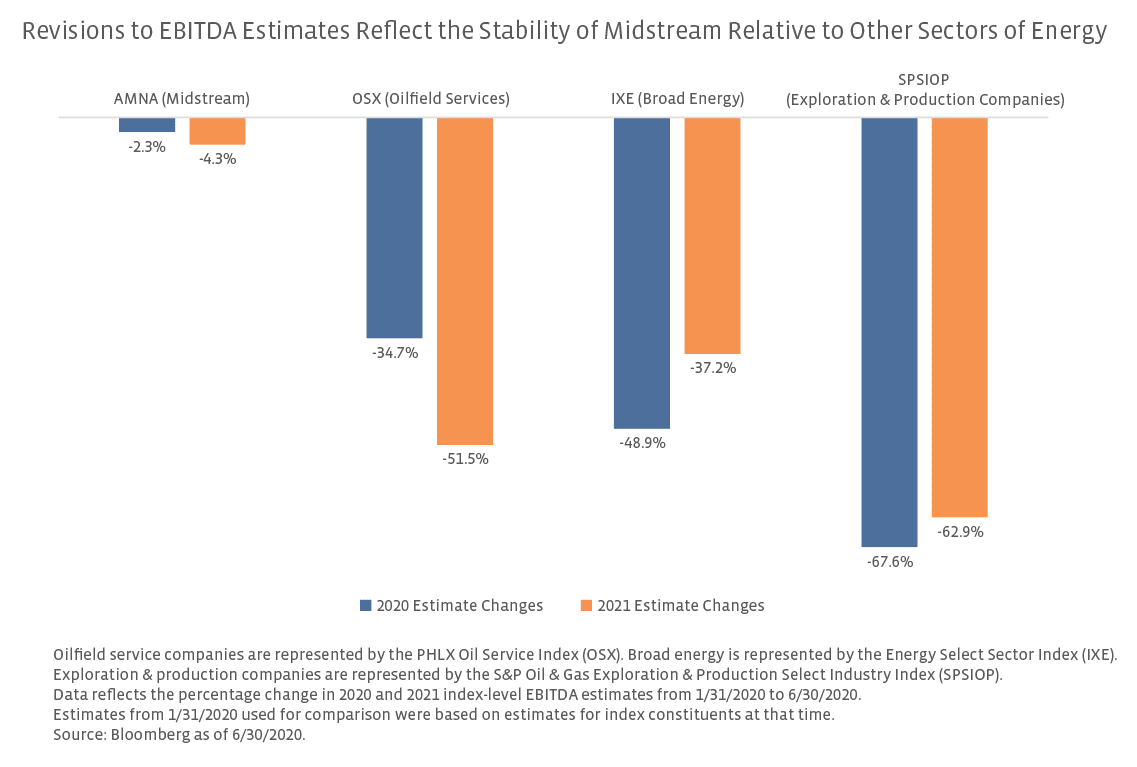

Despite macro headwinds today related to COVID-19, North American midstream companies are well positioned to withstand market volatility. Companies have responded by prioritizing financial flexibility, which has led to widespread reductions in growth capital spending plans and dividend cuts for smaller names. Specifically for AMNA, 20 of 48 constituents as of April cut their payouts for 1Q20, but this represented only 10.3% of the index by weighting as of April 17. While dividend cuts are frustrating for investors, they leave the space better positioned to weather current challenges. Furthermore, the fee-based nature of midstream insulates the sector’s cash flows from commodity price volatility, particularly relative to other sectors of energy as shown in the chart below.

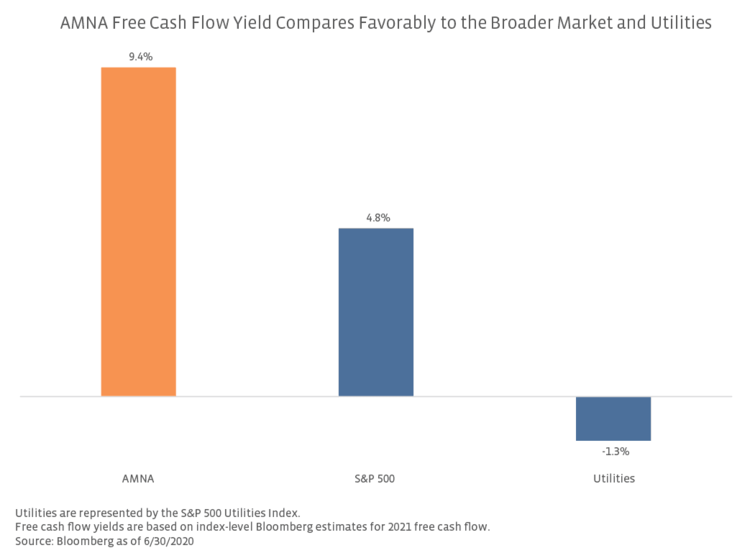

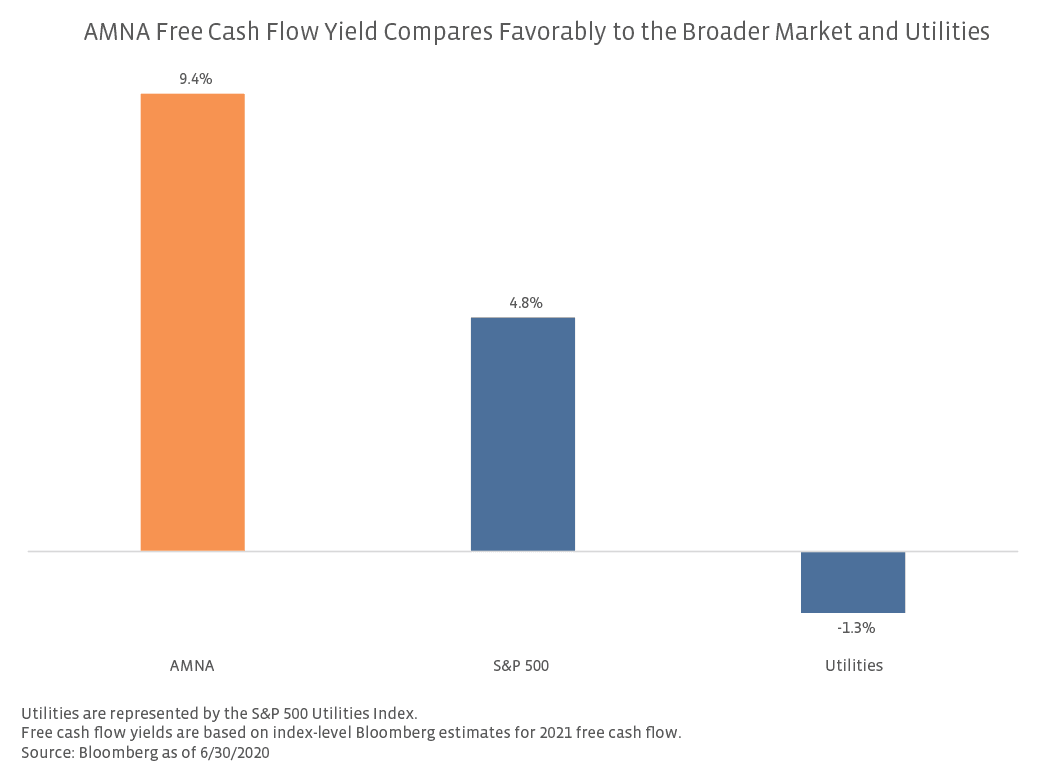

Entering 2020, the midstream space was nearing a free cash flow inflection point as growth capital spending was moderating from peak levels in recent years. Several companies had free cash flow generation after dividends in their sights for 2020 or 2021 (read more). Despite current macro challenges, midstream has the potential to generate meaningful free cash flow in the coming years, as shown in the chart below. In the near term, excess cash flow will likely be used to reduce leverage and shore up financial positioning. However, as demand recovers and energy markets stabilize, midstream could be well positioned to direct excess cash flow to shareholder-friendly returns, including buybacks and dividend increases.

Conclusion

Changes in the midstream landscape have necessitated a more comprehensive benchmark with MLPs and corporations. The Alerian Midstream Energy Index (AMNA) fulfills stakeholders’ needs for a representative sector benchmark for the North American midstream universe.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}