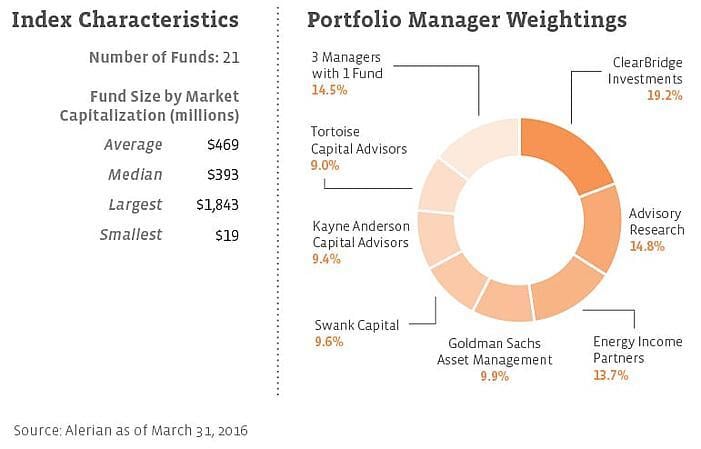

The Alerian Closed End Fund Index’s construction is relatively straight-forward. Today, there are 21 MLP C Corp CEFs on the market, with AUMs ranging from $19 million to nearly $2 billion. All of these funds are included and equal-weighted within the AMCI. Historical data was generated by backtesting the index back to 2004, when the first MLP C Corp CEFs were launched.

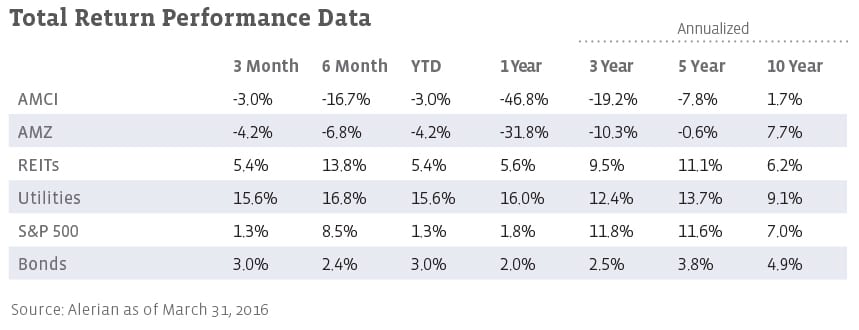

Examining the total return performance of the AMCI in the chart above, you’ll notice that it lags significantly behind the AMZ. This is expected and really showcases the effect of the C Corp tax drag. Even though CEFs use leverage to offset some of this drag, that leverage is only helpful on the way up. On the way down, leverage exacerbates losses. Although in the past three months, the AMCI has outperformed the AMZ, over periods of a year or longer, it has significantly underperformed.

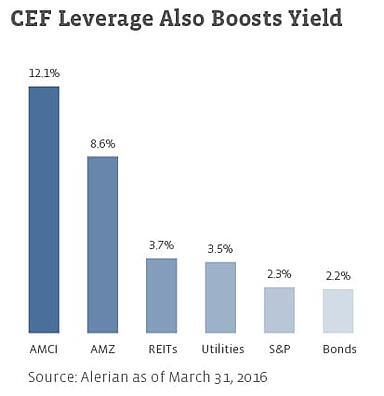

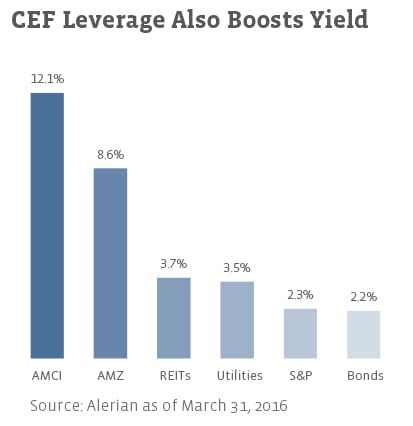

When looking at the yield of the AMCI, you’ll see that it’s also significantly higher than the AMZ. While some CEFs may focus their investments on higher-yielding MLPs, it’s not necessarily a universal trend, with leverage playing a larger role in boosting yields.

One important note is that since this index is equal-weighted, small funds have an outsized influence on index performance while larger funds may be under-represented when compared to an AUM- weighted index. Unfortunately, the smallest funds are also the worst-performing in the index.

When looking at the price return of the AMCI as of 3/31/16, the following data points stand out.

• 12 of 21 funds have outperformed the AMCI on a trailing one-year basis

• 11 of 13 funds have outperformed the AMCI on a trailing three-year basis

• 7 of 8 funds have outperformed the AMCI on a trailing five-year basis

• 4 of 4 funds have outperformed the AMCI on a trailing 10-year basis

How is it possible that the majority of index constituents outperformed the index for the 3-, 5-, and 10-year history? Unfortunately, two funds dragged the entire index down by hundreds of basis points. Although it’s unfortunate that these funds had such a negative impact on index performance, it also showcases that there can be large disparity between the best- and worst-performing active managers.

In the end, Alerian exists to equip investors to make informed decisions about their MLP investments. There are multitudes of MLP-related funds in the marketplace today and the most important thing is to know what you own. If you’ve already made the decision to go with an active manager and are comfortable with the pros and cons of C Corp CEFs, we hope that the AMCI better equips you to make an informed decision with your investments.

2016.05.19 2:30PM CST – Edited to correct phrasing in paragraph 4 and footnote 4.

{kind=link}

{kind=link}

{kind=link}