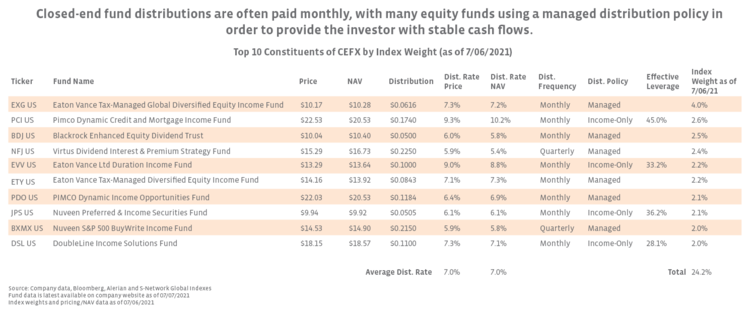

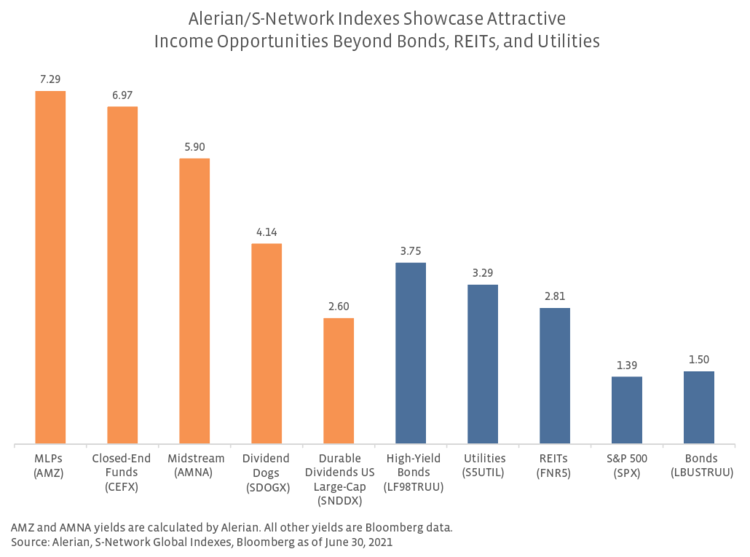

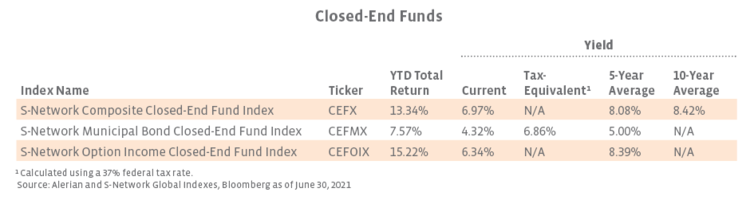

As interest rates remain near historical lows, investors have been hunting for yield. Compared to other income-oriented sectors like bonds and REITs, closed-end funds (CEFs) have considerably higher yields. Currently, the S-Network Composite Closed-End Fund Index (CEFX) has a yield of 6.97% and the S-Network Municipal Bond Closed-End Fund Index (CEFMX) has a yield of 4.32% (6.86% tax-equivalent). High yields in this sector can be attributed to several factors. To begin with, closed-end funds are exempt from corporate taxes on the condition that they pass through net investment income (interest and dividends) to shareholders. Most CEFs pay these distributions monthly—although some also pay quarterly—compared to traditional fixed income instruments, which pay coupons semiannually. CEFs also pay net realized capital gain distributions typically at the end of the year. Some equity and alternative strategy funds, however, expect to earn a large portion of their return through capital gains, rather than dividends or interest. In this case, they can use a managed distribution policy, which attempts to forecast capital appreciation for the year and incorporate that into the regular monthly/quarterly distribution payment. This can benefit investors by providing more stable cash flows, but it also comes with the risk that the fund may overestimate the unrealized capital gain and return principal instead.

Another factor that contributes to higher yields is the difference between CEF and open-end mutual fund structures. Open-end funds must have enough liquidity to continuously issue shares, while closed-end funds typically only issue new shares during the IPO. After the IPO, CEF shares can only be bought and sold on an exchange, so the fund does not need to hold cash for redemptions and can fully invest that cash in its strategy with more focus on a long term, income-oriented view. The fixed asset base also allows the fund to better utilize leverage—arguably the biggest differentiator of income for a CEF.

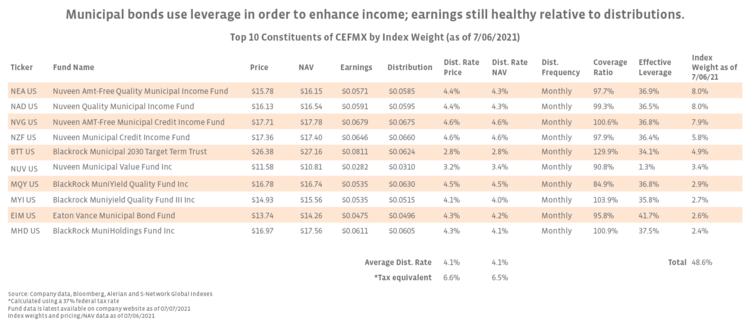

Fixed income CEFs can use leverage—borrowing at lower, short-term rates and reinvesting in higher rates—to enhance earnings and income. According to Bloomberg data, over 2/3 of CEFs use some form of leverage, which includes debt and preferred stock. Lower interest rate environments, like our current environment, are particularly beneficial for funds that use leverage. As short-term interest rates decrease, the cost of leverage (i.e., the cost to borrow) decreases and the fund’s earnings increase as the spread between borrowing cost and investment rate widens. Higher earnings help support the fund’s distribution, which can be measured by the distribution coverage ratio. A fund with earnings greater than its distributions will have a coverage ratio >100%, whereas a fund with earnings below its distribution will have a coverage ratio <100%. A fund with a low distribution coverage ratio may have more risk of cutting its distributions, although another factor to consider is the fund’s undistributed net investment income (UNII), which is the total balance of available funds outside of current earnings that the fund can use for future distributions. It is also worth noting that while leverage can potentially enhance a fund’s yield, it can have the opposite effect if interest rates rise and can result in greater losses than an unleveraged fund.

For a typical investor, certain concepts like managed distribution policies and leverage for equity and fixed income funds, respectively, hold risks that may require some additional consideration. Even with firm knowledge of CEFs, it is still difficult to predict when a distribution cut will occur and how to take advantage of premiums/discounts. Risk averse investors may prefer to invest in CEFs through professionally managed index-linked products which provide access to a variety of CEF managers and styles, while still providing above average yield relative to most other sectors.

Current Yields vs. History

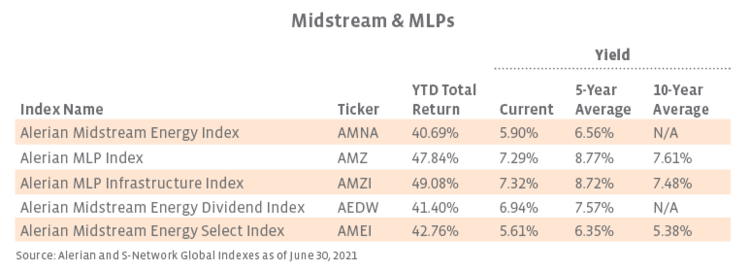

Midstream/MLP indexes continue to offer healthy yields. While below historical averages, yields remain in the 5% to 7% range.

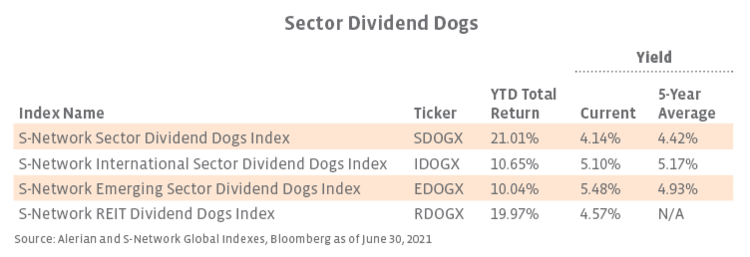

Among the Sector Dividend Dogs, yields are close to historical averages. EDOGX is the only index in the suite to offer a current yield above the 5-year average.

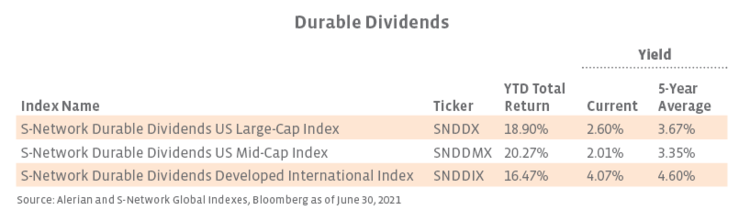

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes.

Though current yields are slightly below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio.

Related research:

A Smarter Approach to Closed-End Funds

Midstream Income Opportunities: Dividends Resilient Throughout Recent Quarters

Biden’s Tax Proposal and Tax-Efficient Income Opportunities