What’s wrong with midstream (aside from negative energy sentiment)?

1) Production growth concerns.

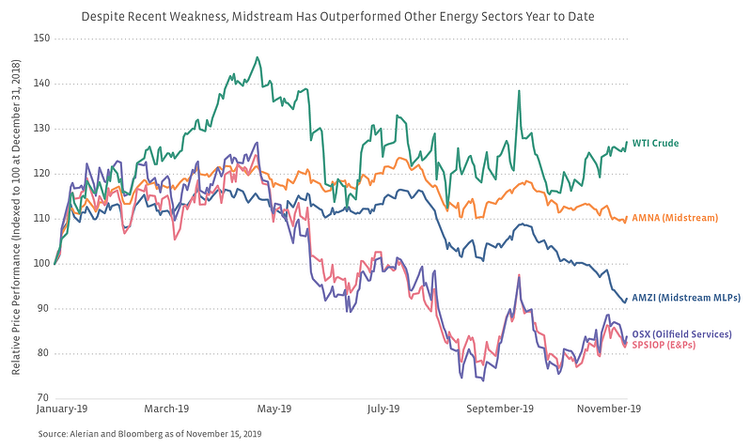

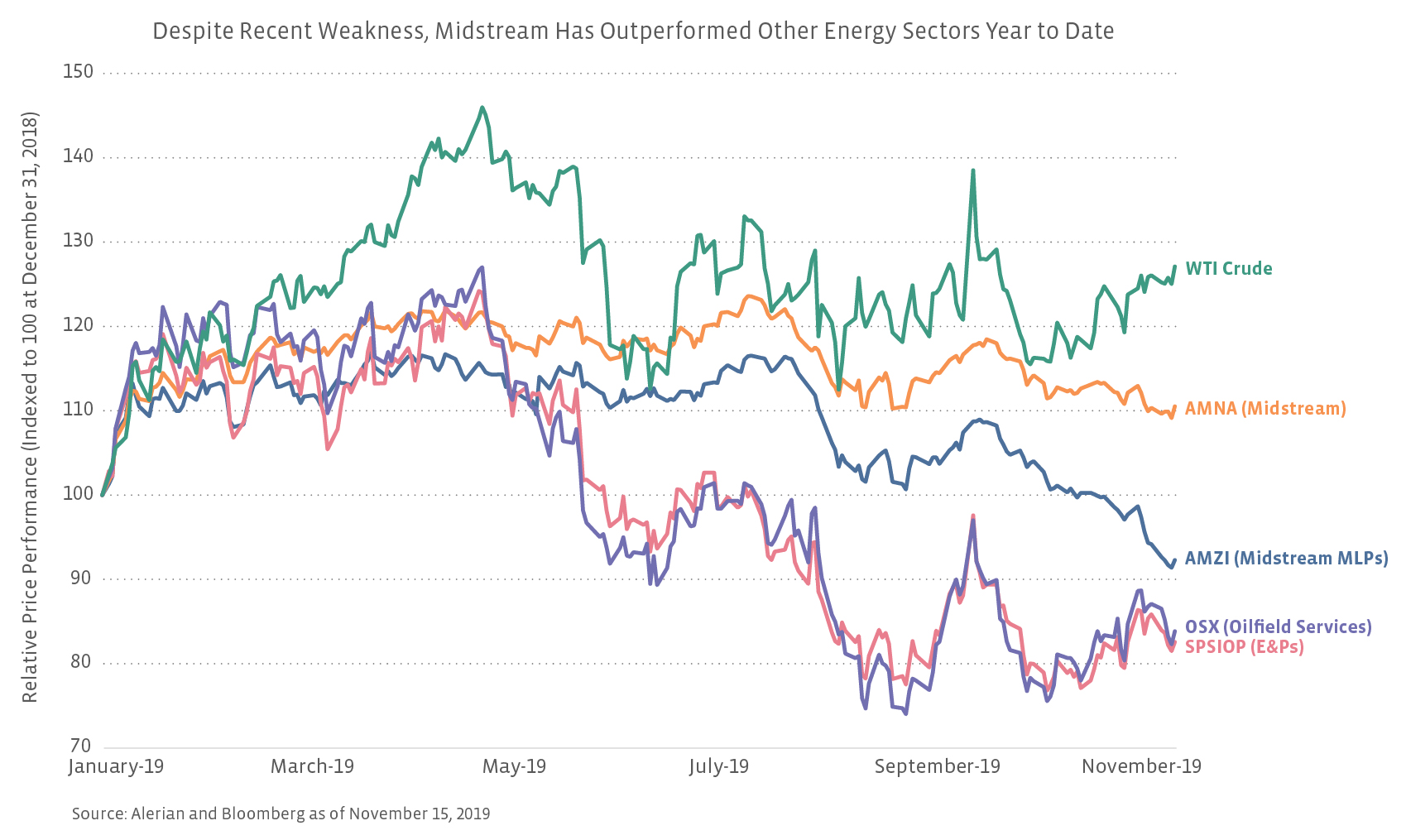

After years of significant growth, US oil and natural gas production growth is starting to slow due to commodity price weakness and forced capital discipline from E&P companies. Several producers lowered production guidance with their 2Q19 and 3Q19 earnings releases, which can have implications for midstream volumes. In particular, slowing growth has weighed on gathering and processing companies, which are closest to the wellhead (connecting wells with larger pipelines and processing natural gas into a usable form). Gathering and processing companies represent 25.7% of the AMNA Index. For additional commentary around production growth and midstream implications, please see our related notes on oil production and natural gas production.

2) Counterparty risks in focus.

Commodity price weakness has weighed on E&Ps, raising concerns about midstream customers’ ability to hold up contracts as activity decreases. In the past, we have seen E&Ps and midstream providers renegotiate contracts when the E&P is under stress. Rates may be adjusted with terms extended, or the midstream provider may receive a lump-sum cash payment. For example, in August 2016, Williams Partners (former ticker WPZ) renegotiated contracts with CHK in the Barnett and Mid-Continent, which resulted in $820 million in cash payments and adjusted gathering rates in the Barnett through 2029 linked to Henry Hub prices. The renegotiated contracts were expected to maintain the net present value of cash flows from the assets. As an alternative example, when Sabine Oil & Gas went bankrupt, a judge ruled that gathering contracts between Sabine and a subsidiary of Cheniere Energy (LNG) could be rejected, a decision that was upheld in the appeals process. If E&P customers go bankrupt, it could have negative implications for their midstream providers, which highlights the importance of a diversified revenue stream and diversified midstream exposure.

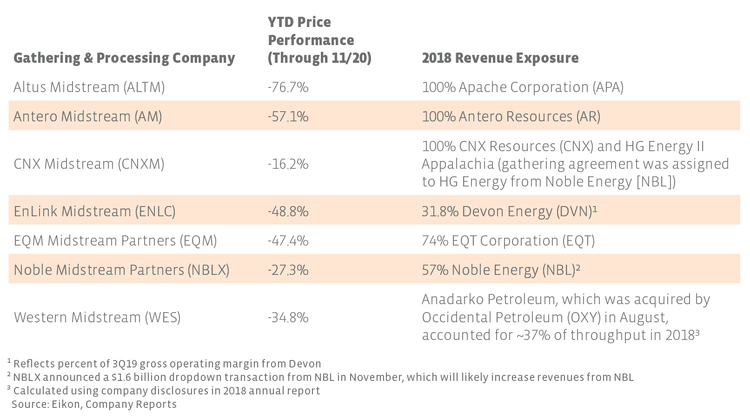

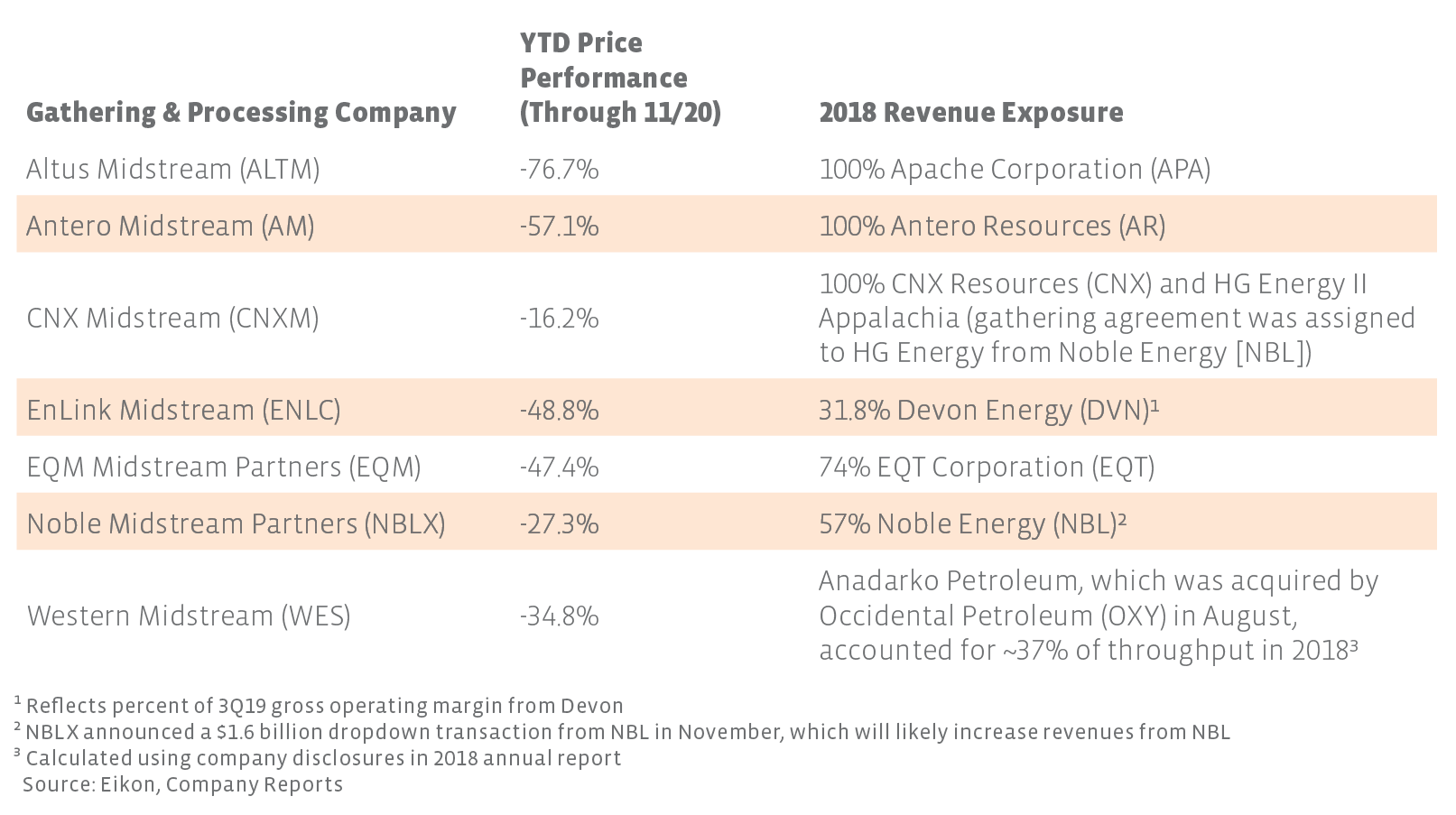

Midstream companies with exposure to one main producer are particularly at risk, and the nature of contracts matter. Midstream corporation Altus Midstream (ALTM) has acreage dedications covering all of Apache Corporation’s (APA) Alpine High acreage, but no minimum volume commitments. Reduced activity by APA has pressured ALTM. The table below includes examples of gathering and processing companies with a single major customer and price performance this year.

With Chesapeake’s going concern language, midstream exposure to CHK is in focus. In 2018, Chesapeake accounted for 8% of The Williams Companies’ (WMB) revenue; however, WMB sold its 50% interest in the Jackalope Gas Gathering System, which services CHK’s Powder River Basin (PRB) acreage along with other producers, to Crestwood Equity Partners (CEQP) in 2019, bringing CEQP’s ownership to 100%. At the time of the transaction, CEQP guided to $100 million in annual cash flow from Jackalope in 2019, growing to $150 million by 2021. In its latest presentation, CEQP noted that the PRB is CHK’s top oil-producing area and provides the best net-backs to CHK. In its 2018 10-K (prior to the consolidation of Jackalope), no customer accounted for more than 10% of CEQP’s revenues.

3) Tax-loss selling.

In recent years, tax-loss selling has weighed on the midstream space into the end of the year. Given broader market strength, investors tend to have gains elsewhere and may sell their midstream position to harvest losses.

What’s still right with midstream?

The long-term midstream thesis remains intact. While production growth is slowing, it is still increasing. The US Energy Information Administration (EIA) forecasts that US oil production will increase 8.1% (1 million barrels per day) and gas production will increase 3.0% (2.8 billion cubic feet per day) in 2020. Additionally, the US is expected to become a net energy exporter next year according to the EIA, and the world’s leading exporter of LNG by 2024 according to the International Energy Agency. In short, the world needs US energy, and midstream will play a vital role in connecting US energy with demand domestically and overseas.

Positioning has improved. Midstream’s broad emphasis on reducing leverage, shifting to self-funding equity, increasing financial flexibility and removing IDRs to lower the cost of capital have resulted in a stronger space. Average leverage for AMZI constituents was 4.09x in 2016 compared to 3.85x in 2018. Average distribution coverage in 4Q16 was 1.2x compared to 1.4x in 3Q19. In 2016, 38% of the AMZI by weight had eliminated incentive distribution rights (IDRs), whereas today more than 85% of the index by weight has eliminated costly IDRs.

Insiders have been buying showing confidence in the companies and broader thesis. Willie Chiang, CEO of Plains All American (PAA/PAGP), bought 60,000 units of PAGP valued at over $1 million last week, as did Chairman Greg Armstrong. Energy Transfer (ET) management has also been busy buying this month, with purchases by CEO Kelcy Warren, CFO Thomas Long, and Marshall McCrea. Per Eikon, KMI’s Executive Chairman Rich Kinder has purchased ~$100 million in KMI this year (recent filings – 10/29, 10/31, 11/11), which has performed well as noted above.

What’s bad for the micro is good for the macro. While it may not provide much consolation to energy investors, the challenging commodity price environment and subsequent discipline from producers is good for the macro commodity picture. As is often said in this industry, the cure for low prices is low prices. Moderating production growth sets the stage for oil and gas price improvement, though it may take time. Furthermore, slower production growth should lead to more moderate growth capital spending by midstream, laying the groundwork for free cash flow generation (read more).

Execution by E&Ps could lead the way to more investor interest. Aside from the integrated majors, E&Ps are probably the most common holdings among generalist investors. If E&Ps can weather today’s volatility well and demonstrate capital discipline, it may help them to rebuild rapport with investors, which could improve energy sentiment more broadly.

In the short-term, there tends to be a January effect. In conjunction with tax-loss selling at year end, there tends to be a rebound at the start of the new year. The AMZI has seen positive price performance in January for seven of the last ten years, and on average, the price gain in January for the past ten years has been 1.9%. For the last three years, the average price return has been 7.1% in January.

Bottom line

Although it remains defensive, the general malaise in energy has infected midstream. Production concerns, counterparty risks, and tax-loss selling have combined to weigh on the space, with some names disproportionately impacted due to their customer base. Despite these headwinds, the long-term thesis for midstream remains intact, with midstream expected to play a vital role in supplying US energy to the world. Improved financial flexibility should help midstream weather the current environment.

{kind=link}

{kind=link}