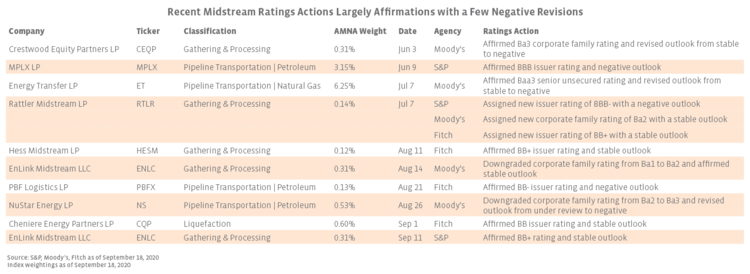

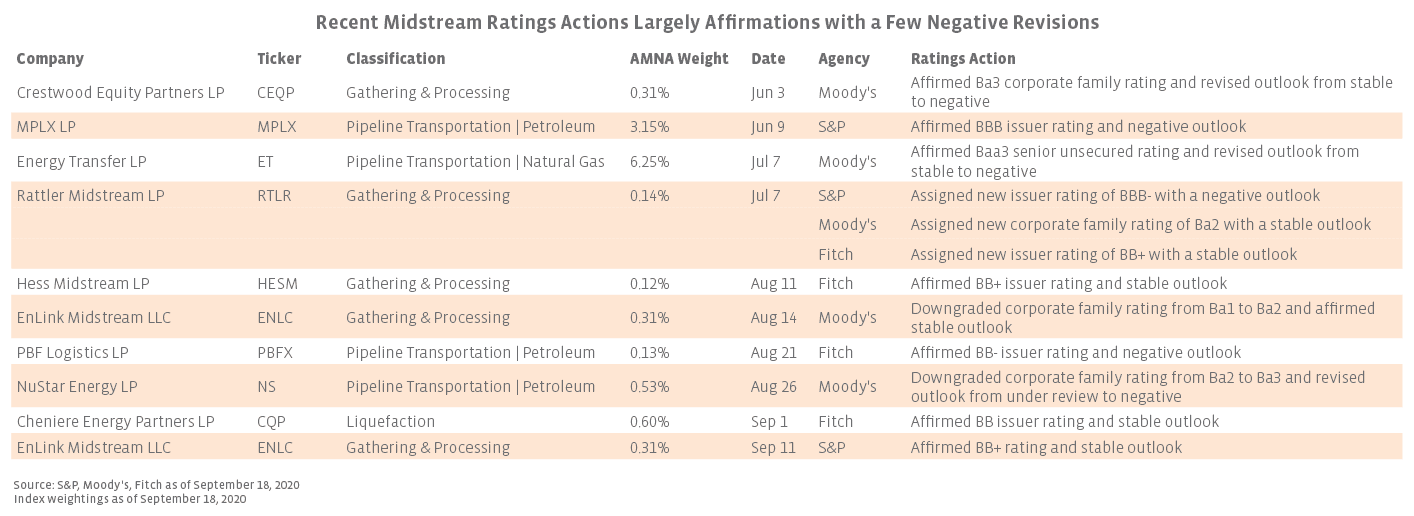

Since early June, the midstream space has seen several updates from the ratings agencies covering companies of different sizes and classifications. While cases where the rating outlook was revised to negative have been common in recent months, the issuer rating itself has often been reaffirmed. With the economic challenges brought by the COVID-19 pandemic providing a kind of stress test for midstream broadly, the lack of widespread ratings downgrades is encouraging. Large partnerships MPLX (MPLX) and Energy Transfer (ET) had their investment grade ratings affirmed by S&P and Moody’s, respectively. In keeping MPLX’s BBB issuer rating the same in June, S&P cited the geographic diversity and size of MPLX’s operations as well as the partnership’s high percentage of fee-based revenue. Despite maintaining its Baa3 rating, Moody’s revised ET’s outlook (through subsidiary Energy Transfer Operating) from stable to negative in early July because of the potential impact on earnings and greater difficulty reducing leverage that would be caused by a potential shutdown of the Dakota Access Pipeline, though the pipeline is currently expected to operate through the end of this year based on the timeline for legal proceedings. In general, large midstream companies with diverse operations across different basins as well as strong counterparties are unlikely to see significant ratings changes.

There have been two issuer ratings downgrades since June primarily due to the company’s operations or financial situation. In August, Moody’s reduced EnLink Midstream’s (ENLC) corporate family rating from Ba1 to Ba2, owing to concerns about its cash flow profile and leverage in 2021 given potentially lower volumes in some of its main operating areas such as the STACK play in Oklahoma. However, in September, S&P affirmed its BB+ issuer rating on ENLC and stable outlook due to its forecast for relatively steady distribution coverage and improving leverage. Moody’s also downgraded NuStar Energy’s (NS) corporate family rating from Ba2 to Ba3 on concerns about elevated leverage and weak free cash flow generation, which is expected to delay deleveraging. The agency is also closely monitoring oil prices as a result of the uneven pace of the economic recovery, with an extended period of low commodity prices carrying over to heightened concerns about counterparty risk for midstream companies.

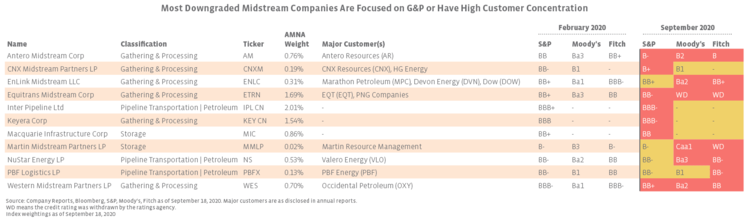

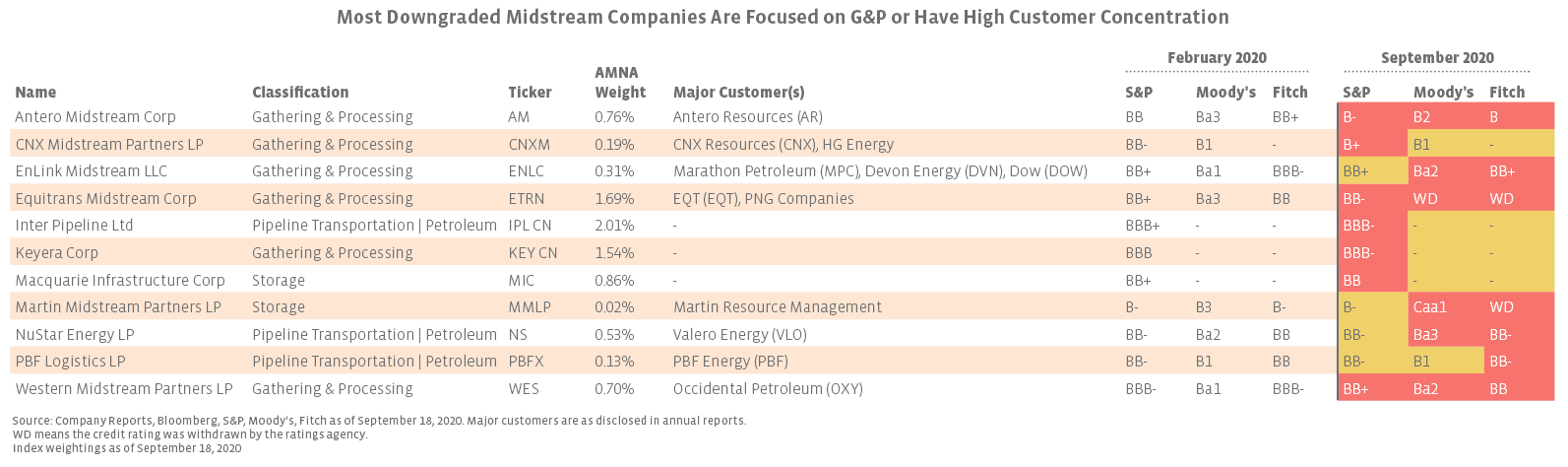

Examining AMNA credit ratings before COVID-19 and now.

Comparing ratings over a wider timeframe is also helpful in understanding the midstream credit market and the ratings agency assessments. While there have been some downgrades of midstream ratings since early February, downgrades have not been common overall. Using ratings data from Bloomberg, the ratings of about 90% of the AMNA Index by weighting (excluding names that are not rated) remained the same during the period from February 1 to September 17. In general, the midstream names that were downgraded have a concentrated customer base and are more likely to be primarily involved in gathering and processing (G&P). The table below summarizes midstream downgrades with ratings for the three major ratings agencies as of February 1 prior to COVID-19 impacts in North America and currently as of September 18. The table also includes major customers, which are those that represented greater than 10% of revenues in 2019.

Looking at the ratings generally, companies remained in their investment grade or high yield camps despite downgrades with the exception of Western Midstream (WES). WES moved from investment grade to high yield over the time period, which aligns with the change in ratings for its major customer and 51.5% owner Occidental Petroleum (OXY). Notably, G&P was the most common classification for the companies that have been downgraded, which likely reflects the greater commodity price sensitivity of these companies given more dependence on upstream activity, producer counterparties, and the need for new wells to support growth. Furthermore, processing contracts can sometimes be based on commodity prices instead of flat fees. The downgrades also include a number of companies with concentrated counterparty exposure. Antero Midstream (AM), CNX Midstream (CNXM), Equitrans Midstream, and WES all have significant exposure to a single producer customer, and PBF Logistics (PBFX) is leveraged to refiner parent PBF Energy (PBF). Of the major customers in the table, Antero Resources (AR), CNX Resources (CNX), EQT (EQT), PBF, and OXY are rated high yield. In late August, S&P reiterated that it is focused on counterparty risk and revenue concentration with major customers. Many of the downgrades for the midstream companies above reflect corresponding downgrades and uncertain outlooks for their primary customer. Without a diverse customer base, there is less ability to mitigate counterparty risk. However, exposure to a single customer can also cut the other way by providing visibility to cash flows if the counterparty is well-positioned to withstand volatility.

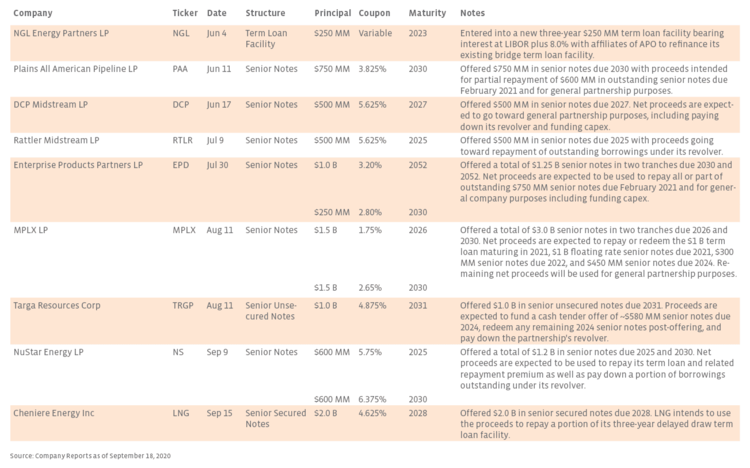

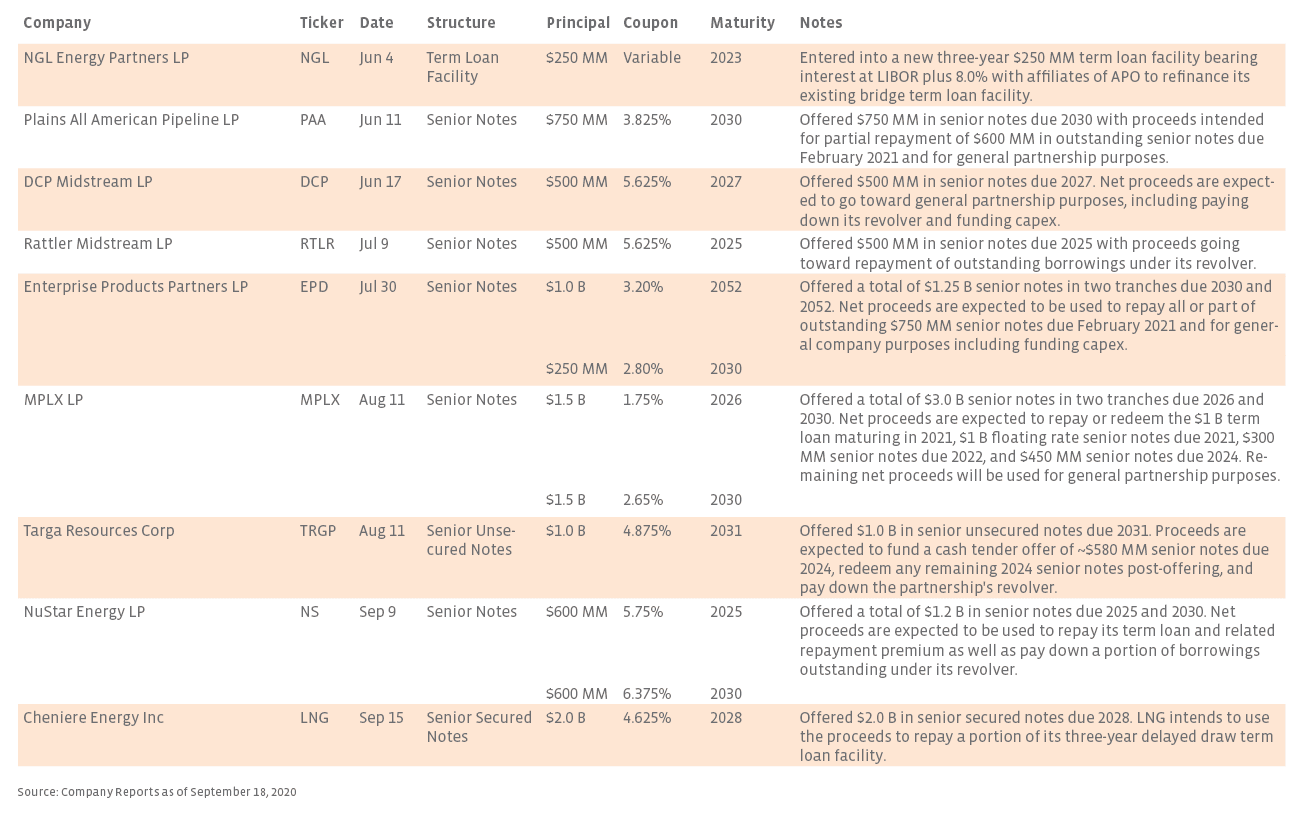

Midstream companies continue to access debt markets and reduce near-term maturities.

In recent months, debt markets have remained open for midstream companies, with several high yield issuers among the offerings. The table below summarizes midstream debt offerings since June. Overall, terms have generally been reasonable for recent debt issuances and largely in line with similar offerings from the past. After agreeing to a costly $750 million term loan at 12% with Oaktree in April, high yield issuer NS completed an offering of $1.2 billion of senior notes in September at rates of 5.75% and 6.375% for maturities in 2025 and 2030, respectively, that are expected to be used to pay back the term loan (including a repayment premium) and reduce outstanding borrowings under its revolver. The offering should help remove an overhang created by the term loan and extend the partnership’s maturities.

Several companies have used issuances to help pay down debt outstanding under credit facilities or impending senior note maturities. Large MLPs Plains All American (PAA) and Enterprise Products Partners (EPD) both tapped the debt markets in June for $750 million and $1.25 billion, respectively. PAA said it would use the proceeds to partially repay senior notes due February 2021, while EPD expected to repay all or part of $750 million in senior notes due February 2021. Similarly, in August, MPLX offered a total of $3.0 billion in senior notes to be used to repay or redeem its $1 billion term loan maturing in 2021, $300 million in senior notes due 2022, and $450 million in senior notes due 2024. Debt issuances at relatively favorable terms improve near-term liquidity and provide further financial flexibility for these companies as the economy recovers. Midstream companies that need to further reduce near-term maturities should be able to access debt markets.

Bottom Line

Despite the challenges of the last several months, midstream companies with a diverse set of assets and creditworthy counterparties have demonstrated that they are well-positioned to withstand a volatile market environment from a credit perspective. Midstream management teams can continue to take steps to improve their short-term financial positioning and increase flexibility by tapping debt markets at favorable terms to reduce near-term debt maturities.

{kind=link}

{kind=link}

{kind=link}