The table above provides examples from 2Q but is not exhaustive for midstream capex increases. For example, Phillips 66 Partners (PSXP) raised its total capital budget by $150 million on its 1Q18 earnings call, reflecting in part the Gray Oak Pipeline project from the Permian. Midstream corporation. Williams (WMB) raised its growth capital guidance for 2018 and 2019 in its 2Q release to reflect the acquisition of Discovery DJ Services and other projects. Of course, not all midstream spending increases are a function of additional growth opportunities. For example, EQT Midstream Partners (EQM) recently increased the project cost for the Mountain Valley Pipeline from $3.5 – $3.7 billion to $4.6 billion due to work stoppages, weather events, and some overruns on construction costs.

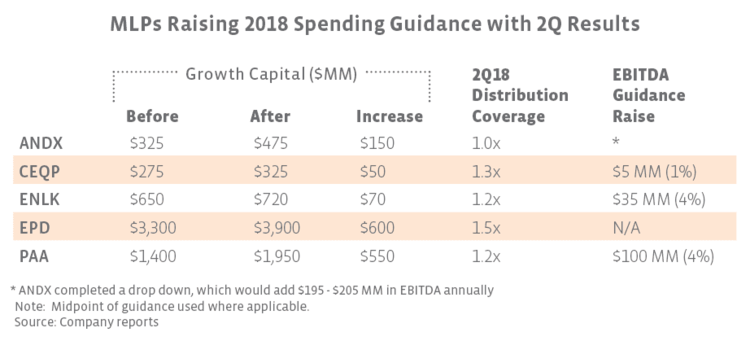

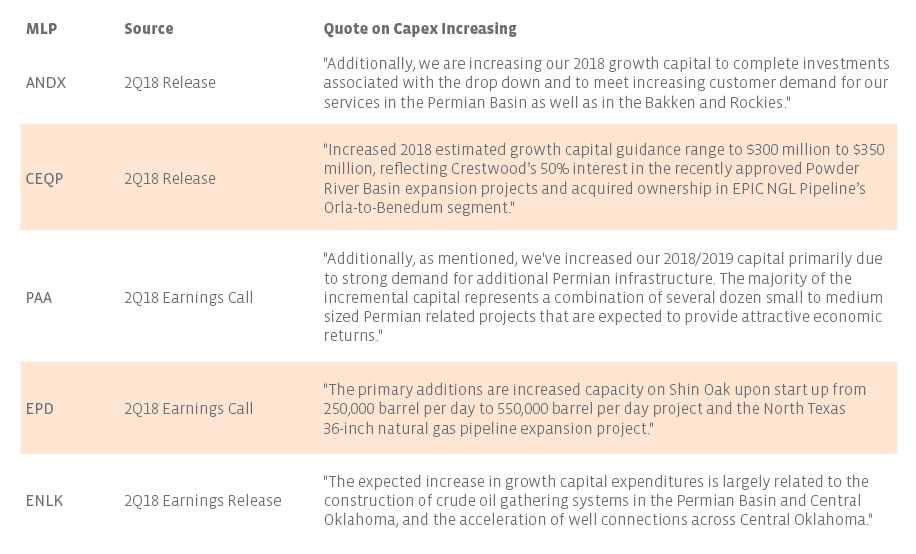

Interestingly, for the five MLPs, the increase was at least partially attributed to activity in the Permian. In some cases, the Permian was the sole driver of increased spending. Acquisitions were also a factor in some of the increases. See commentary in the table below. As we seem to continually repeat, the growth in oil and natural gas production in the US creates growth opportunities for the midstream space, and these increases are clear evidence of that. Improvements in drilling technologies and increased efficiencies from E&Ps and oilfield service companies also benefit the midstream space.

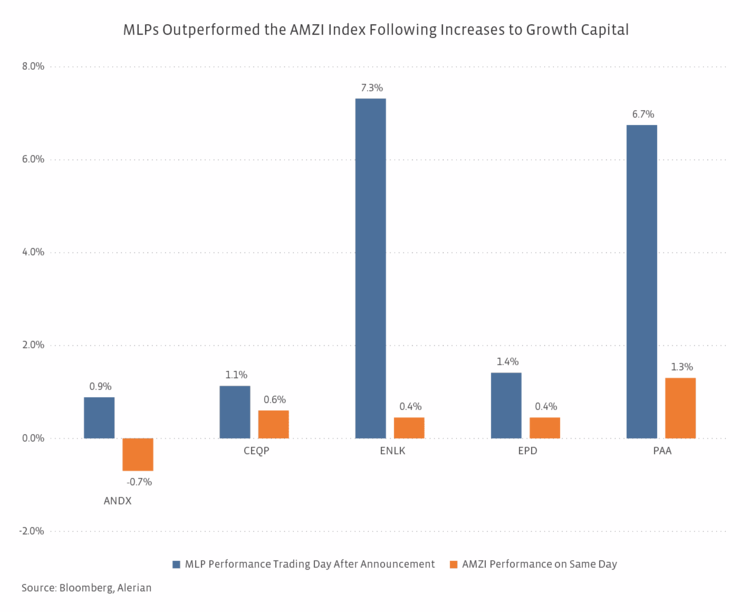

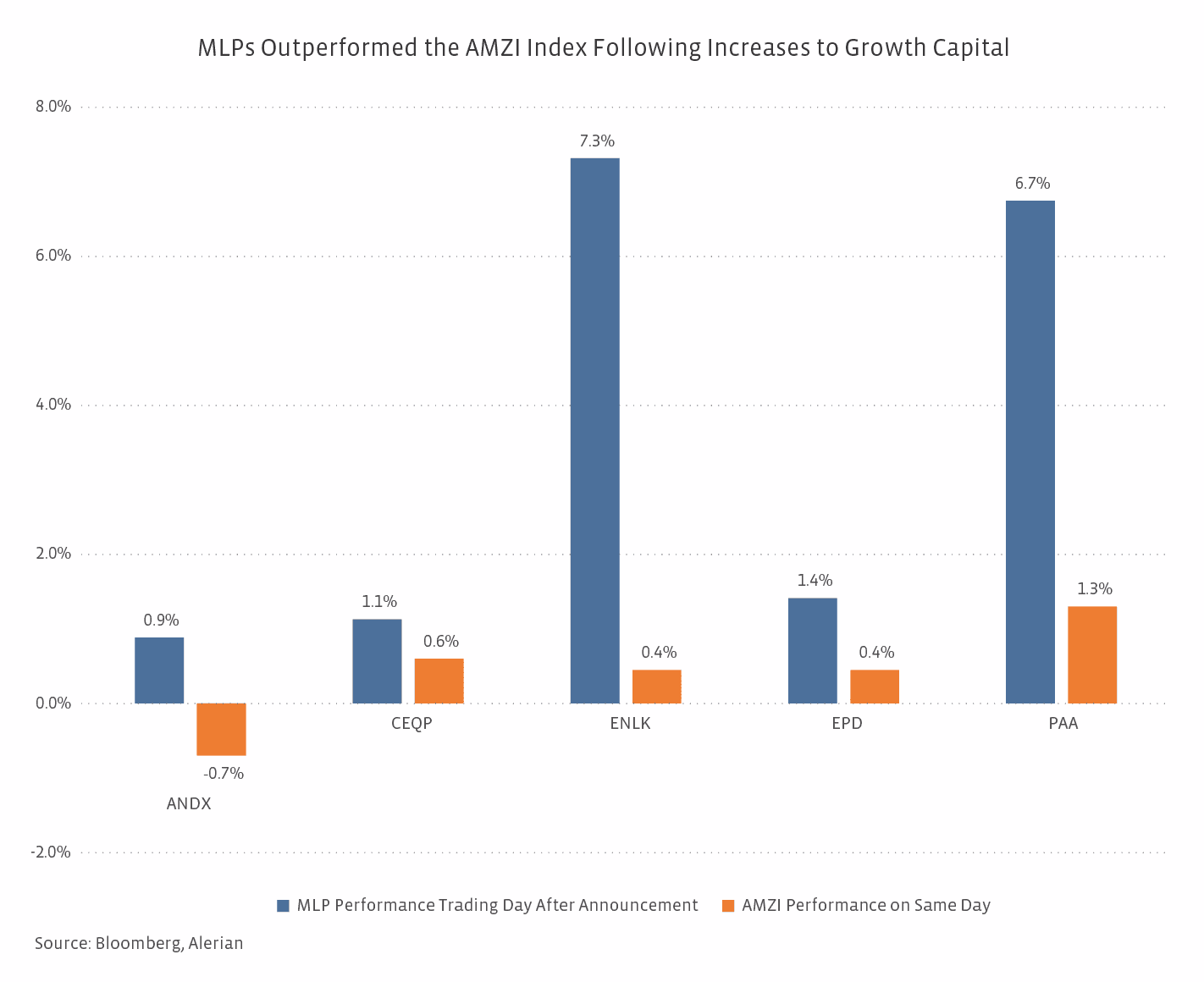

Across the board, the MLPs announcing increased growth spending with their 2Q results outperformed the Alerian MLP Infrastructure Index (AMZI) on the trading day immediately following their announcement as shown below. C-Corp WMB gained 3.0% on the trading day following its earnings release, outperforming the 1.6% gain in the Alerian Midstream Energy Index (AMNA). It would be misleading to say that the outperformance was solely due to increased growth spending, as earnings results and conference calls encompass a multitude of data points. As noted above, three MLPs also increased EBITDA guidance. That said, one can at least argue that midstream companies were not penalized for increasing their growth capital plans – unlike E&Ps.

E&Ps: Increasing capital budgets generally frustrates.

E&Ps have long been notorious for spending beyond their cash flows in the name of production growth. Dividends have typically been limited, particularly among smaller E&Ps, though some larger E&Ps have been more generous. In the wake of the oil downturn, E&Ps have begun to embrace capital discipline, free cash flow generation, and returning cash to shareholders as investors have demanded more discipline and a greater focus on returns. (For more context, see this Wood Mackenzie article.)

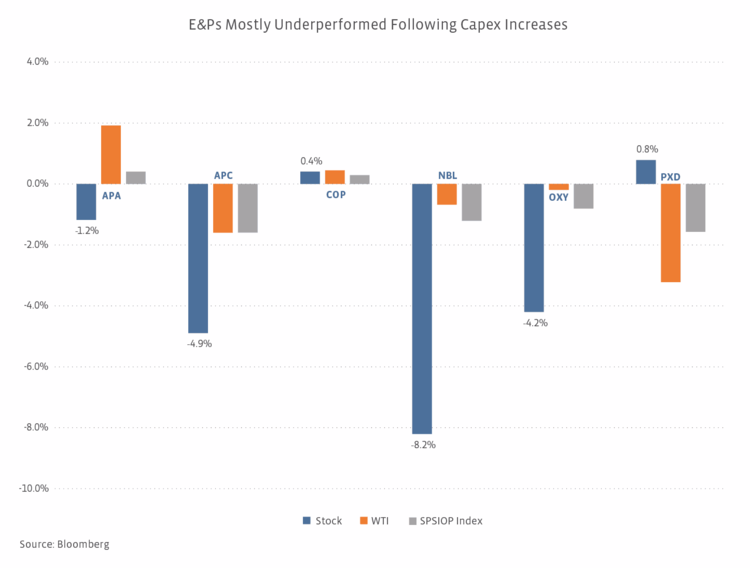

Multiple E&Ps raised capital spending guidance with their 2Q results, typically citing higher service costs due to higher oil prices or plans to increase activity. Occidental (OXY) raised its capital budget by a significant $1.1 billion (28%), with the increase largely driven by Permian opportunities characterized as high-return, short-cycle projects. Apache Corp (APA) raised its 2018 capital guidance from $3.0 to $3.4 billion, with most of the increase allocated to the Permian. Noble Energy (NBL) raised its 2018 capital spending to $3.0 billion from a prior range of $2.7 – $2.9 billion due to higher spending on onshore projects related to a change in scope and industry cost inflation. Other E&Ps announcing increased spending plans for 2018 include Anadarko Petroleum (APC), ConocoPhillips (COP), and Pioneer Natural Resources (PXD), among others.

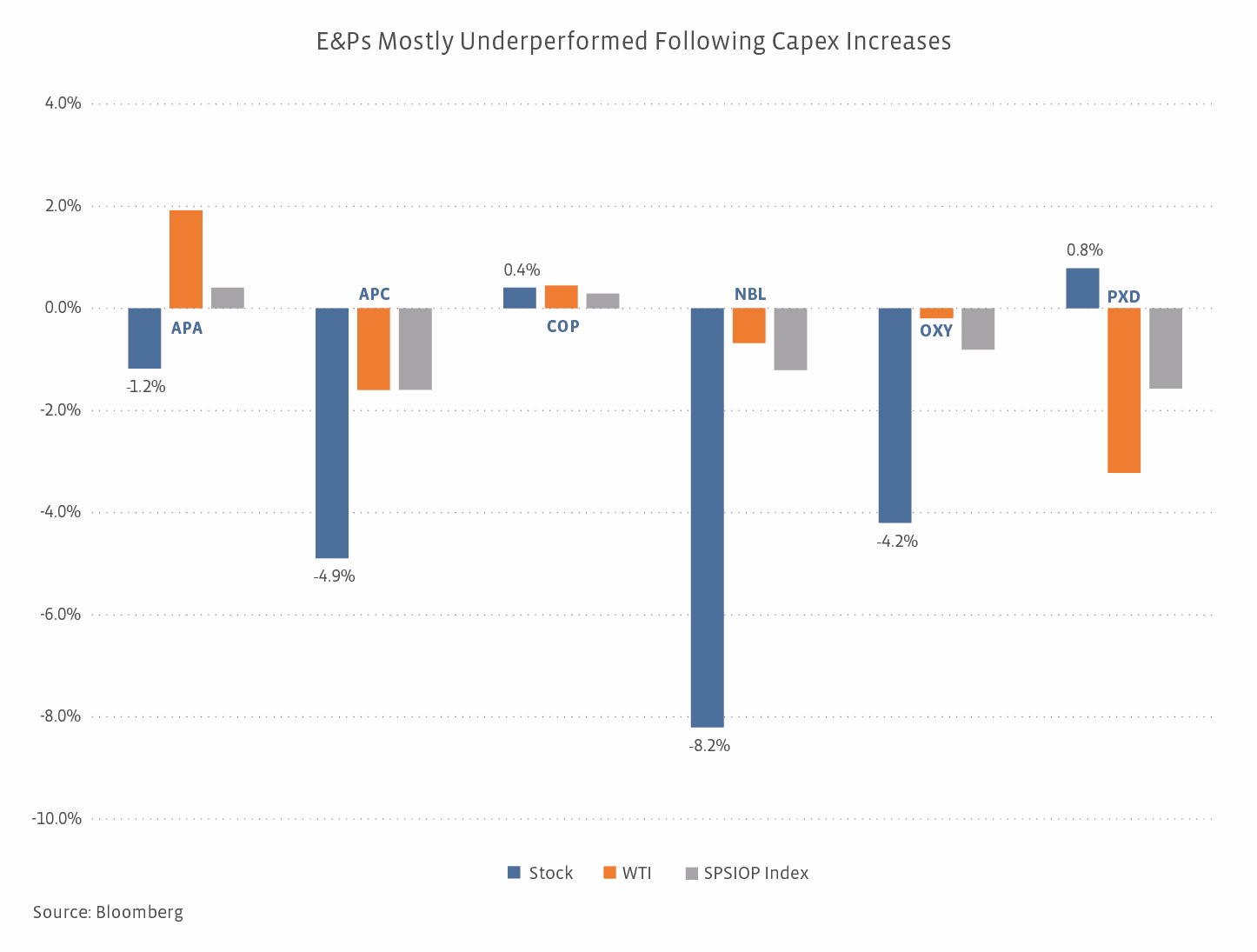

As shown, E&Ps announcing increased capital spending plans tended to underperform the relevant benchmark, the S&P Oil & Gas Exploration & Production Select Industry Index (SPSIOP), on the day of their announcement. COP and PXD are exceptions, with COP having also announced an increase to its production guidance. As with midstream, the spending increase was not the only news to accompany earnings and was not the only factor in how E&P stocks traded. For example, NBL’s performance was also likely impacted by comments that sales volumes for 2018 would come in at the low end of the guidance range provided. The first questions from analysts on NBL’s call and OXY’s call were related to capex, though.

Why the opposite market reactions to Midstream and E&P capex hikes?

Aside from being energy companies and shifting to focus more on capital discipline, MLPs and E&Ps don’t have a lot in common. Accordingly, they have different business models, risk profiles, policies on returning cash to shareholders, and investor bases. Midstream growth projects are generally built with customer commitments in place and clear visibility to fee-based cash flows and thus have a lower risk profile than investments in drilling activities. E&P project returns are subject to commodity price risk, and increased spending does not necessarily equate to increased production (NBL is an example) or cash flows, particularly with spending increases driven by cost inflation.

One would think that the higher oil price environment today would help soften any impact from a capex hike for E&Ps. Since 2Q18 results were announced in late July and early August, WTI oil prices have improved from the high-$60s per barrel to the mid-$70s/bbl. Surprisingly, only half of the E&Ps listed are trading at a higher level now than they were on the day of their earnings announcement (APA, COP, and OXY). Three of the five MLPs are trading higher as of the close on October 8th (ANDX, CEQP, ENLK), excluding EPD, which is trading only 20 cents lower. WMB is also trading lower.

Bottom Line

While several midstream companies and E&Ps raised capex guidance with their 2Q18 earnings, the market generally viewed increases from midstream names more positively. Of course, increased activity and production growth from E&Ps are what create opportunities for midstream – higher spending due to cost inflation does not. E&P investors’ frustration with a lack of capital discipline, particularly when it stems from increased activity, may ultimately be midstream investors’ gain.

{kind=link}

{kind=link}

{kind=link}

{kind=link}