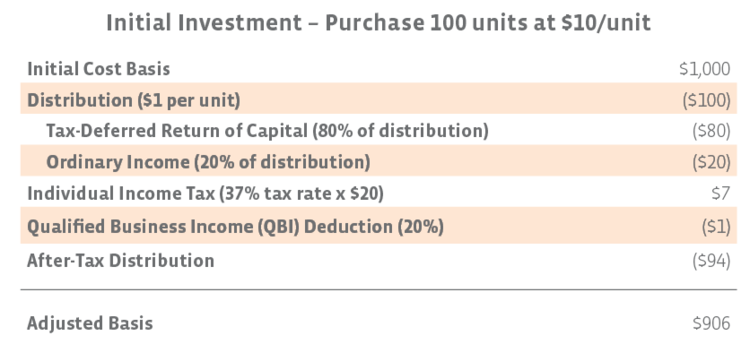

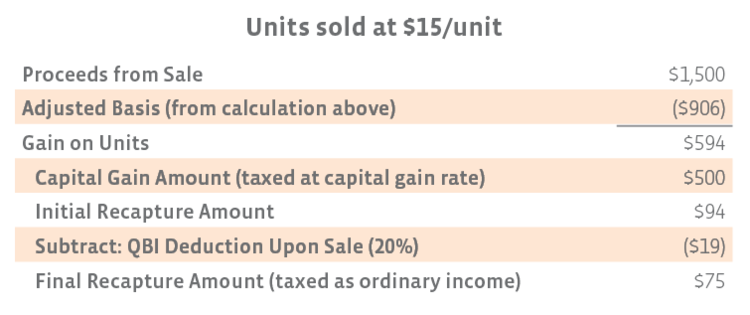

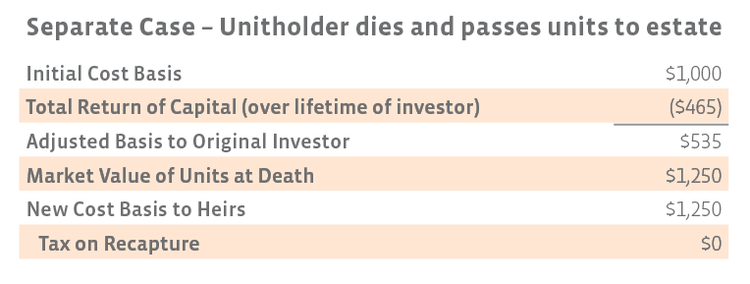

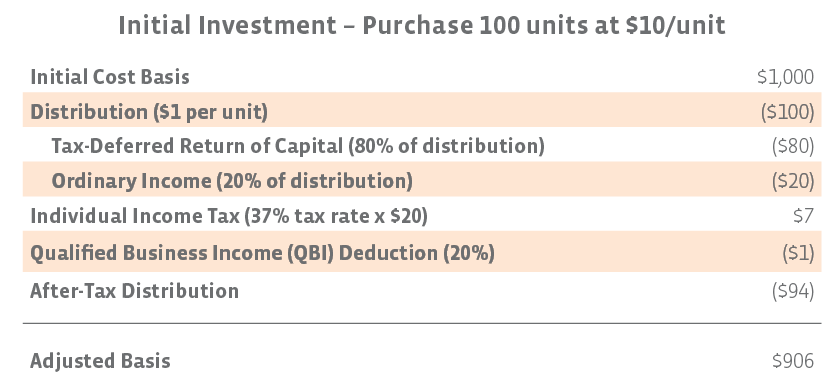

Investing directly in MLPs may be less desirable for some investors.

While MLPs provide tax benefits for US investors, foreign investors can face high tax rates if they invest in MLPs. As a result of US tax law, MLPs are required to withhold taxes from the distributions of foreign unitholders at the highest individual tax rate (37%). Foreign investors can potentially avoid this withholding by buying swaps on MLPs. In a total return swap, a bank or other counterparty purchases the underlying asset (MLPs) and pays the distribution and capital gains to the investor in exchange for a negotiated borrowing rate.

Another potential issue for investors is Unrelated Business Income Tax (UBIT), which can arise when a tax-advantaged account directly invests in MLPs. UBIT is generated when Unrelated Business Taxable Income (UBTI) exceeds $1,000 in a given year, as the tax is designed to prevent unrelated business activity within a tax-exempt vehicle such as an IRA or 401(k). The good news for ETF investors is that you do not need to worry about UBTI if you are invested in an MLP ETF in a tax-advantaged account like an IRA (Read More).

Tax considerations for MLP investment products.

When considering MLP investment products, it’s important to keep in mind their tax implications and how they differ from individual MLPs. First of all, MLP access products generally issue a single form 1099, which means you do not receive a Schedule K-1. Instead, K-1 forms are processed by the product issuer, and they distribute a 1099 form to investors.

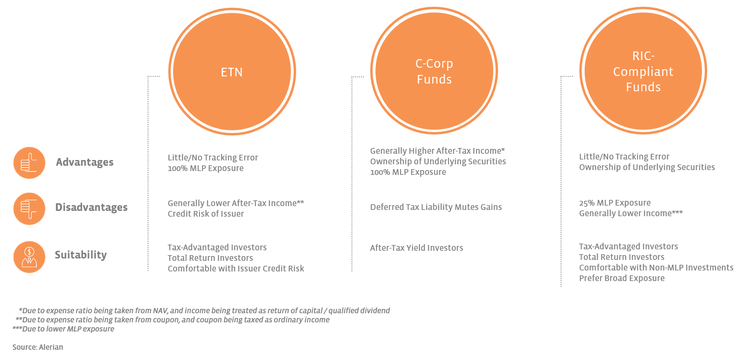

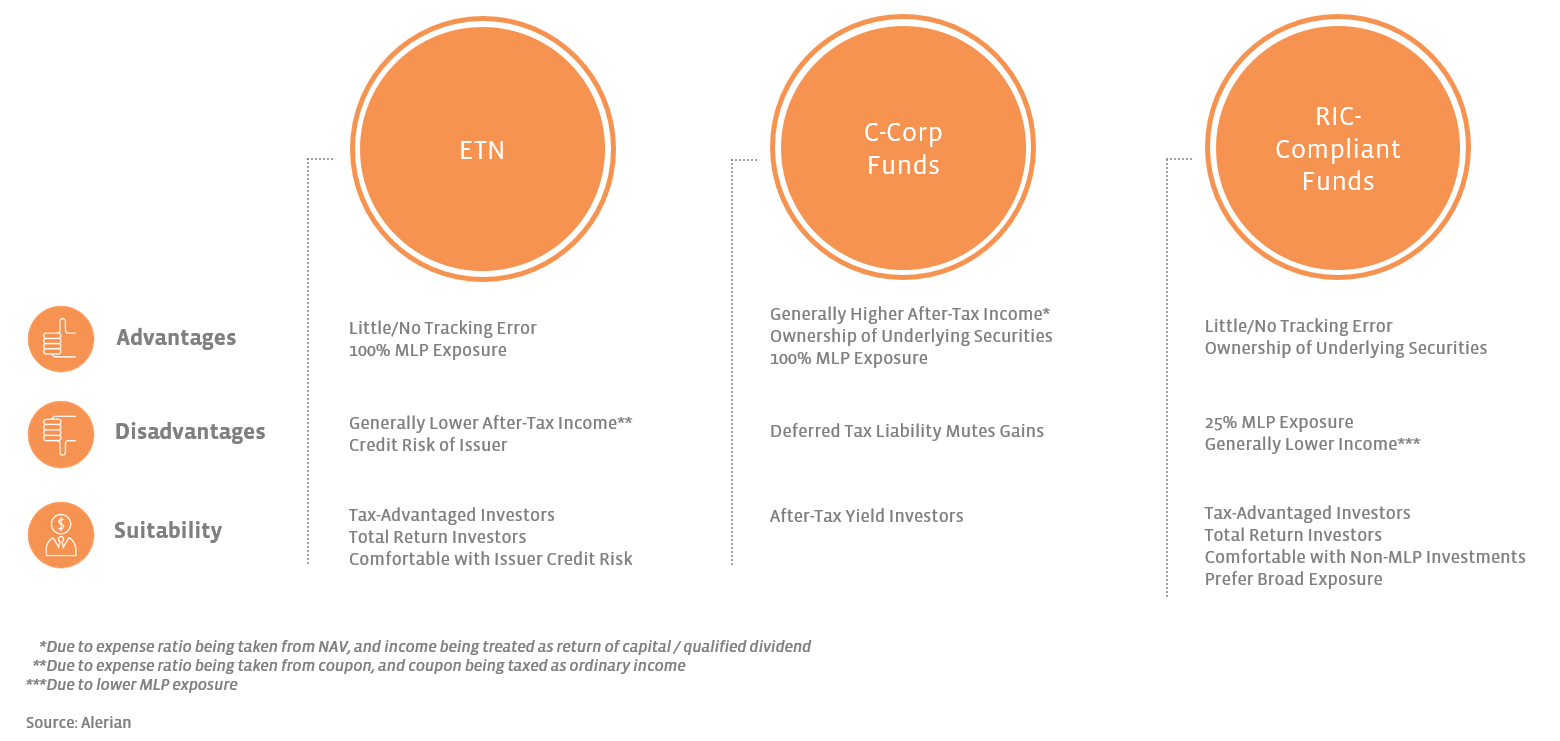

Products also have different tax characteristics depending on structure (see graphic below). C-Corp funds — funds that own more than 25% MLPs — are taxed as corporations (currently 21%). Because the fund’s earnings are taxed, the product issuer withholds a certain amount at the fund level to pay taxes and accrues a deferred tax liability or asset. The result is that the fund will not perfectly track the underlying securities when it is in a net deferred tax liability status. For example, if the underlying securities appreciate by 10%, the fund will only appreciate by 7.9%. The fund’s distribution, however, retains the tax characteristics of the underlying securities. As a result, a significant portion of fund distributions will typically be treated as a tax-deferred return of capital, with the remainder taxed at qualified dividend rates (which share similar tax treatment as long-term capital gain rates).

RIC-compliant funds (those that hold less than 25% MLPs) do not pay taxes at the entity level as pass-through entities. As a result, there is no tax drag on performance, making them attractive for tax-advantaged investors interested in total return. In contrast to C-Corp funds, more of the distribution from RIC-compliant funds is taxed as qualified dividends rather than tax-deferred return of capital. As a result, when combined with lower exposure to MLPs, RIC-compliant funds generate lower after-tax income compared to C-Corp funds. Exchange-traded notes (ETNs) are different than funds in that they are debt obligations issued by a bank who agrees to provide the return of an underlying index minus fees. ETN coupons are taxed at the ordinary income rate. ETNs, like RIC-compliant ETFs, do not have a tax drag on capital appreciation. For more information on MLP access products, please refer to our piece from January.

Bottom Line

While the tax benefits of MLPs can be complex, the investment story for MLPs is simple in contrast. Growing production of US oil and natural gas will increasingly be exported overseas to meet rising global demand, requiring additional energy infrastructure such as pipelines, storage terminals, and natural gas processing plants. MLPs benefit as fee-based businesses, generating cash flows through long-term contracts with customers for the volumes handled by those assets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}