Summary

- Multiple factors likely mitigate the potential negative impact of rising rates on midstream, including debt reduction in recent years.

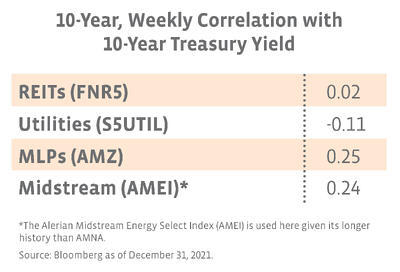

- Midstream and MLP indexes have had a modest positive correlation with the 10-Year Treasury yield over the last decade.

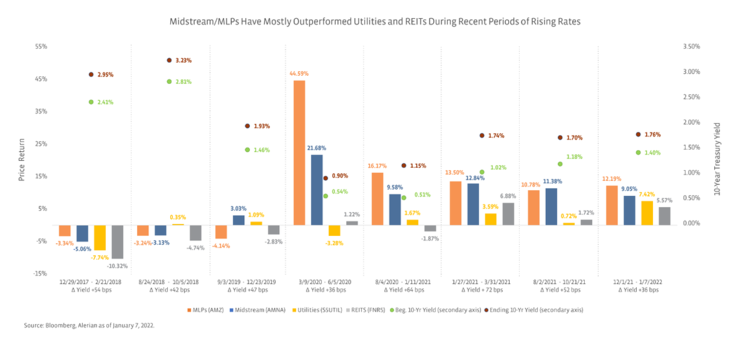

- In recent periods of rising interest rates, MLPs and midstream generally outperformed utilities and REITs, though admittedly the macro recovery in energy likely helped in 2H20 and 2021.

Inflation has been top of mind for investors for months. Last week’s Consumer Price Index reading for December, which showed a 7% year-over-year increase and marked the largest jump since the early 1980’s, has only added to the concern. Recent comments from Federal Reserve officials indicate that addressing inflation is a key priority, and interest rate hikes could be implemented as soon as March to temper inflation. Over the years, investors have often asked how midstream performs in rising interest rate environments, particularly relative to other equity income investments. Today’s note addresses that question and explains why rising rates are not expected to weigh on midstream performance.

Why are rising rates a potential concern?

For midstream, rising interest rates can be a headwind in two ways: 1) increased competition for investor dollars among yield vehicles as fixed income investments become more attractive and 2) borrowing costs rise. Importantly, several factors likely mitigate these headwinds for midstream. First, midstream yields are so much higher than the typical bond yield that bonds and midstream may not be competing directly. For context, at year-end 2021, the Alerian Midstream Energy Index (AMNA) and Alerian MLP Index (AMZ) were yielding 6.3% and 7.9% respectively, compared to the Bloomberg Barclays US Aggregate Bond Index (LBUSTRUU) yielding 1.8% (read more).

While higher rates mean higher borrowing costs for existing variable debt and new debt issuances, this may also be less of an issue for midstream/MLPs, particularly relative to the past. Leverage has trended lower over time as many companies have focused on debt reduction in recent years. Additionally, midstream capital spending has come down meaningfully since peaking in 2018 or 2019 when companies were investing heavily to facilitate production growth. Production volumes are still recovering and below pre-pandemic levels, which has contributed to lower growth capital spending. Reduced capital spending and less debt in the capital structure should help mitigate the impact of rising rates on midstream borrowing costs.

How have midstream and MLP indexes held up in periods of rising rates?

To better understand the relationship between midstream/MLP performance and rising rates, it can be helpful to look at correlation data and historical performance in periods of rising rates. As shown in the table, midstream and MLP indexes have a modest positive correlation with the 10-Year Treasury Yield when looking at weekly correlations for the last decade. Over the same period, REITs have a correlation near 0, and utilities have a slightly negative correlation, implying that interest rates and utility equities tend to trend in opposing directions. Utilities tend to be particularly sensitive to interest rate moves given the capital-intensive nature of their businesses and significant use of debt.

While the correlation data would suggest that midstream and MLPs should fare better than REITs and utilities in a rising rate environment, it is helpful to look at historical examples. The chart below shows periods when the 10-Year Treasury yield was rising since the end of 2017 and how MLPs, broader midstream, utilities, and REITs performed. Overall, MLPs and midstream outperformed utilities and REITs in periods where Treasury yields were increasing. Admittedly, examples of rising rates are limited, and the upward moves in some cases are modest. The macro recovery in energy since the first half of 2020 has also skewed MLP and midstream performance higher in recent periods as rebounding oil and natural gas prices have boosted sentiment for midstream.

So far in 2022, midstream and MLPs have outperformed as the yield on the 10-Year Treasury has increased by 19 basis points, but this has also been coupled with 9.2% gains in oil prices. Year-to-date through January 13, AMZ and AMNA are up 9.1% and 8.7%, respectively, while utilities and REITs are down 2.4% and 5.2%, respectively. Setting aside oil prices, looking forward, to the extent that rising rates encourage a rotation into value, that could also be beneficial for energy stocks, including midstream.

Bottom Line:

While it is difficult to isolate the impact of a rising interest rate environment on midstream equity performance, correlation data and recent historical performance should help allay investor concerns that rising rates may have a negative impact on midstream performance, particularly relative to utilities and REITs.

AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMZ is the underlying index for the JP Morgan Alerian MLP Index ETN (AMJ), the ETRACS Alerian MLP Index ETN Series B (AMUB), and the ETRACS Quarterly Pay 1.5X Leveraged Alerian MLP Index ETN (MLPR).