Summary

- While the delta variant has stalled the global reopening, expectations for rising inflation remain intact.

- Contract service agreements with inflation protection allow midstream names to pass through the effects of inflation, which could potentially lead to higher incremental EBITDA as cost reductions and asset optimization remain a focus.

- Midstream offers exposure to real assets, which tend to outperform during inflationary periods, while also providing attractive yields in a market where inflation is sending real asset yields into negative territory.

Inflation on the horizon.

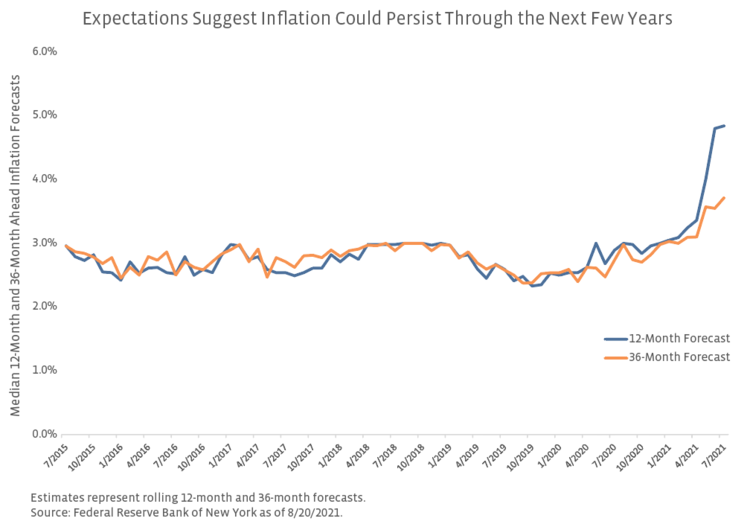

Uncertainty over the effects of monetary stimulus and the supply and demand impacts from COVID-19 and its delta variant have led to a growing divide between those that believe inflation is transitory and those that believe it is going to persist much longer. While speculation continues to dominate the long-term inflation narrative as investors look ahead to the Fed’s Jackson Hole Symposium for more clarity, current expectations for rising inflation remain intact. According to the July 2021 Survey of Consumer Expectations released by the Federal Reserve Bank of New York, one-year-ahead inflation expectations were unchanged at 4.8%, while inflation expectations three years out increased to 3.7%. While the mentioned estimates do not capture how inflation develops through the second half of the year, expectations that pricing pressures will not moderate in 2021 and will likely spill over into 2022, are also increasing. According to Bloomberg’s latest U.S. Economic Forecasts Survey Report released this month, year-over-year CPI forecast for 2021 increased to 4.2% vs prior estimates of 3.7%, while the forecast for 2022 increased to 2.9% vs 2.7% previously.

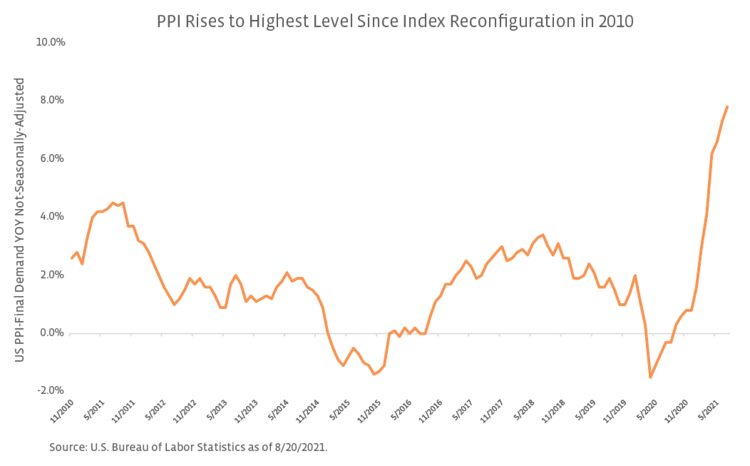

The latest Consumer Price Index (CPI) reading released by the US Labor Department, which measures the prices Americans pay for everyday goods and services, reflected a 0.5% increase in July and a 5.4% year-over-year jump as shelter, food, energy, and new vehicles all contributed to the highest yearly increase since 2008. While the 0.5% CPI reading came in line with expectations and may have suggested inflation is beginning to moderate after rising 0.9% in June, inflation on the producer side suggested otherwise. The Producer Price Index (PPI), which serves as a leading indicator for the CPI as production costs are passed through to consumers, rose by 1.0% in July and 7.8% on a yearly basis, surpassing expectations that called for a 0.6% increase in July. Notably, the index reached its highest level since its reconfiguration in 2010

Midstream inflation pass-through benefits help support margins and complement cost reductions.

With rising expectations for inflation, midstream is well positioned to weather an inflationary environment thanks to key contract provisions and the ability to pass on higher costs to customers. For example, the fees charged by interstate liquids pipelines are often subject to the Federal Energy Regulatory Commission’s (FERC) Oil Pipeline Index, which is based on the Producer Price Index for Finished Goods plus an adjustment (read more). Currently, the index is based on PPI plus 0.78% through June 2026. Companies typically sign contracts with inflation protection included. For example, MPLX’s (MPLX) 10-K states that most pipeline agreements with Marathon Petroleum (MPC) are indexed for inflation, and pipeline fees from third parties are subject to inflation adjustments. Midstream companies, including MPLX and Energy Transfer (ET), often include language in their annual reports noting that they expect to continue to pass along higher costs to customers through higher fees as permitted by regulations, existing contracts, and the competitive environment, consistent with the past. Enbridge (ENB), which has both liquids and natural gas pipelines—and moves about 20% of US gas consumed—mentioned during their 2Q21 conference call that they were well protected from inflation, adding that roughly 80% of their revenues have either built-in inflators contractually or periodic regulatory protections through rate proceedings. At the very least, natural gas pipelines can also file a rate case if costs are not being adequately covered (read more).

Benefits to the topline from contracts with inflation protection could translate into higher incremental EBITDA through margin expansion if inflation rate adjustments outpace increased costs for midstream and as cost control remains a focus. Magellan Midstream Partners (MMP) mentioned on their 2Q21 conference call that historically around 40% of their shipments have been linked to the FERC index and that people and power represent the greatest costs for their pipeline systems and the PPI has outpaced cost increases for those two items. However, they have seen higher costs for maintenance items and capital purchases related to higher steel costs for example. An emphasis on controlling costs and optimizing assets was a continued theme of 2Q21 earnings calls. For example, Enlink Midstream (ENLC) discussed that their ongoing focus on cost reductions is helping offset some inflationary pressures they have seen this year. DCP Midstream (DCP) mentioned they will continue to aggressively manage costs and remain committed to maintaining savings realizations from 2020 while managing the impact of inflationary pressures. Plains All American (PAA) noted that they continue to find cost-saving opportunities and expect to sustain a portion of those savings into the future.

History shows sectors with hard asset exposure outperform during inflationary periods.

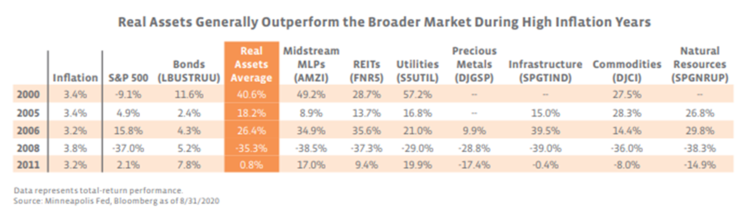

Unlike the last two decades where persistently low inflation had seen hard assets fall out of favor, the case for investing in real assets is becoming increasingly attractive amid rising pricing pressures today. Companies that own or operate real assets such as midstream energy infrastructure companies, can provide liquid real asset exposure (read more). From a performance standpoint, sectors with real assets have generally outperformed the broader equity market when inflation has averaged above 3.0% on a yearly basis since 2000. As shown below, MLPs represented by the Alerian MLP Infrastructure Index (AMZI), have outperformed the broader market during these inflationary years, with the exception of 2008 when the carnage to equity markets from the financial crisis was most severe. MLPs have also held their ground relative to other sectors that offer hard asset exposure, outperforming the real asset average return three of five times inflation averaged above 3% for the year. Inflationary periods can also see higher oil prices, which can be supportive for energy sentiment and the midstream space, even though midstream is not directly levered to the commodity price environment.

Midstream income better suited to withstand inflation-driven yield erosion.

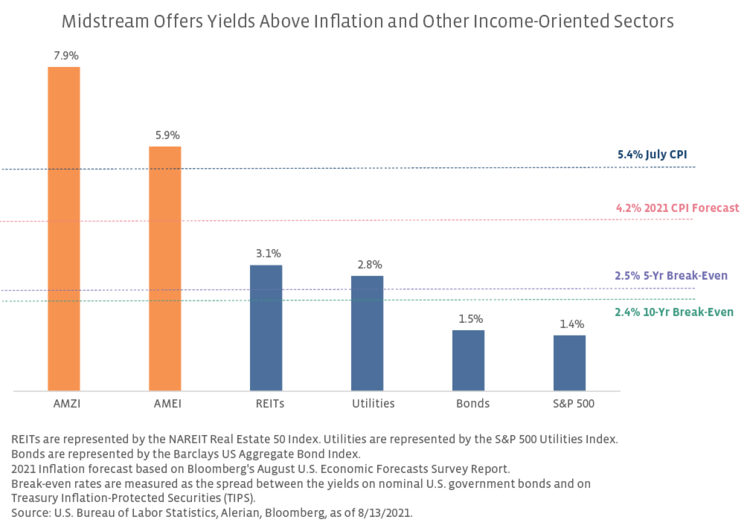

Typically, inflationary pressures tend to be accompanied by rising bond yields, helping offset the yield erosion provided by higher inflation. However, that relationship has broken down as inflationary pressures escalate while treasury bond yields steadily march lower, with the 10-year yield down 48 basis points as of August 20 from its high in March of 1.62%. As of August 13th, the AMZI and the Alerian Midstream Energy Select Index (AMEI) were yielding well above other income-oriented assets, providing higher yields that are better protected from inflation. As shown, midstream offers yields above both current inflation and expected forward inflation, including short-term economist forecasts and inflation break-even rates over a 5- and 10-year horizon. Largely steady distributions, strong 2Q21 results, and a constructive outlook across the midstream space adds confidence to the reliability of midstream income in a market with historically low yields and inflationary pressures.

Bottom Line:

While the Fed should provide some clarity around monetary policy and their inflation outlook during the much-anticipated Jackson Hole Symposium later this week, the effects of surging demand from the global economy reopening and ongoing supply chain bottlenecks suggest inflation could continue to be in focus. Midstream offers protection from the effects of higher inflation and could potentially benefit investors through what could become a period of sustained inflation.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR).