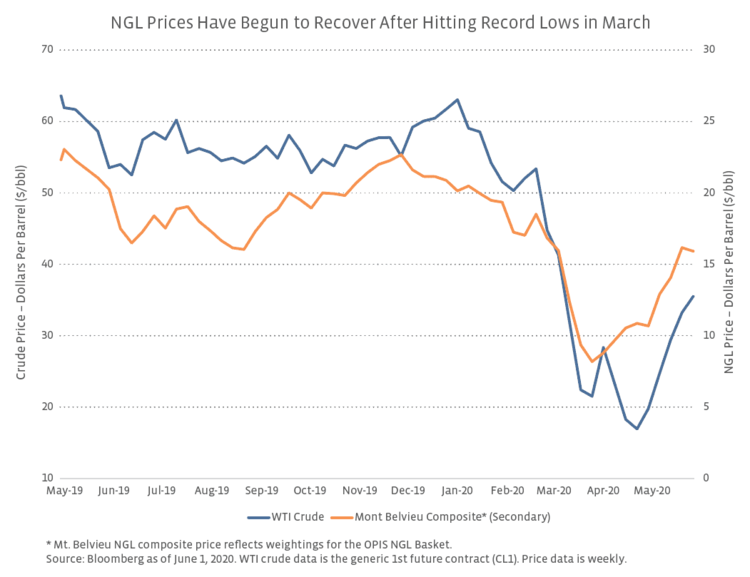

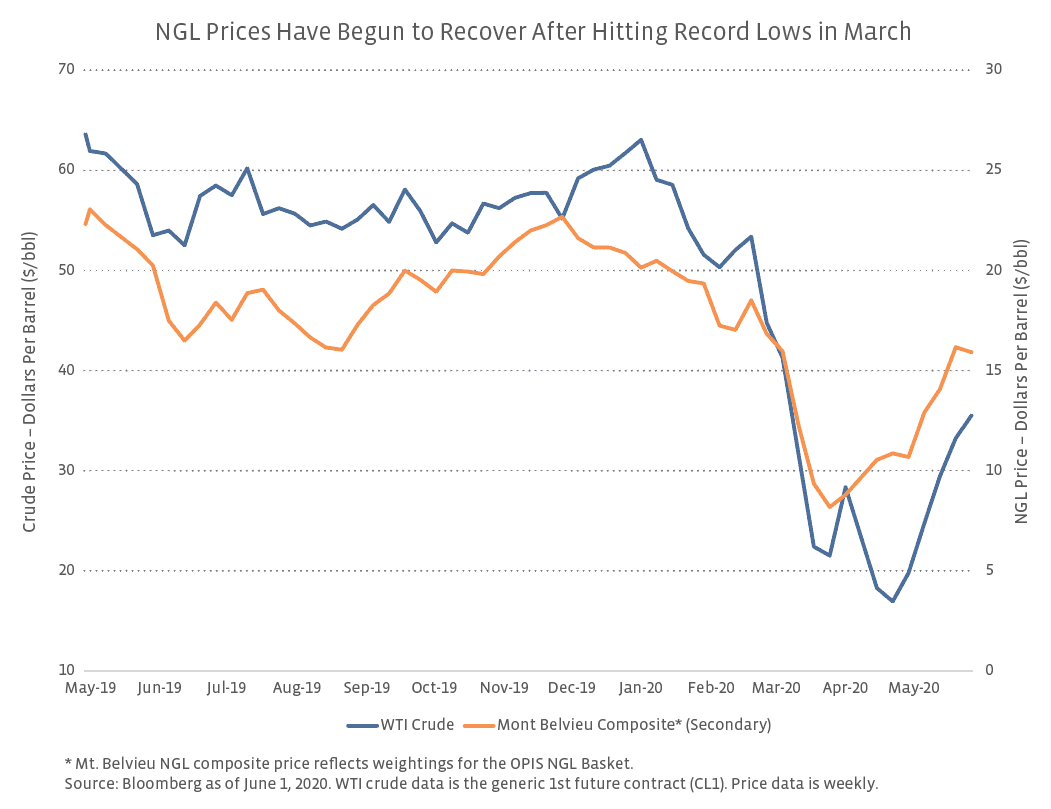

NGL prices at Mont Belvieu have started to recover after hitting record lows in March.

In conjunction with falling oil prices battered by demand headwinds related to the coronavirus, NGL prices slumped to record lows in late March. Year-to-date through March 27, the NGL basket price at Mont Belvieu had fallen more than 60% per Bloomberg as shown in the chart below compared to a 64.8% fall in West Texas Intermediate (WTI) crude prices over the same period. Already weak NGL prices declined in March in conjunction with crude prices as concerns over potential demand erosion were added to ongoing worries about elevated inventory levels for many purity products (read more). The EIA estimates that some of this demand slowdown is likely to endure with US consumption expected to decline by 7.4% this year but rise by 5.3% in 2021 as an economic recovery begins to take hold. However, despite this challenged outlook, the Mont Belvieu basket price has almost doubled off the low through May 29, while WTI oil gained 57.0%. Company commentary supports the idea that NGL demand may be more resilient than previously expected. Range Resources (RRC) reported on its 1Q20 earnings call on May 1 that global demand for its propane and butane has remained robust in the second quarter, with the market showing signs of tightening as continued reductions in supply are expected from global refineries and OPEC producers into 2021. Antero Resources (AR) noted that NGL demand has been resilient because it is driven primarily by the more inelastic demand from the petrochemicals, residential, and commercial sectors as opposed to transportation fuels, which have been hit harder by the coronavirus. Examining NGL prices as a percentage of WTI crude also helps to frame the magnitude of the recent NGL price recovery and the temporary disconnect from the price of WTI. In 4Q19, NGL prices at Mont Belvieu averaged 36.1% of WTI and remained within a relatively tight range of 32% to 41% for much of the period. On April 24, however, the NGL basket price as a percentage of crude surged to more than 60% as NGL prices began to move slowly upward against a continued decline for crude. Over the last month, prices between the two commodities have moved higher together. As of May 29, NGL prices were 44.8% of WTI, which is above the range from 4Q19 and reflects the relative resilience of NGLs.

A potential silver lining for the NGL market, which is evident in the turnaround in prices, is that consumption has remained somewhat resilient for certain petrochemical end products such as consumer plastics. Dow (DOW) recently said Chinese industrial activity has returned to 80-90% of pre-pandemic levels and expects a gradual economic recovery in the second half of 2020 in Europe and North America as economies reopen, which is meaningful for prices broadly. Ethane prices have also risen despite mixed news recently related to ethylene cracker projects, which process ethane into ethylene and help drive ethane demand. Dow started up a 500,000 metric ton per year ethylene cracker expansion at its Freeport, Texas, plant in April, bringing total capacity up to 2.0 million metric tons per year. Formosa Plastics restarted its 680,000 metric ton per year ethylene cracker at Point Comfort, Texas, in late March following planned maintenance but delayed the expected startup of its low-density polyethylene (LDPE) plant to late July or early August. Similarly, the expected startup for Sasol’s (SSL) 420,000 metric ton per year LDPE plant in Lake Charles, Louisiana, was moved back to the second half of this year. While the EIA expects ethane consumption to fall in 2020, ethane demand is expected to increase in 2021 as petrochemical plants like these ramp and manufacturing improves.

How are midstream companies responding to NGL headwinds?

Several midstream management teams offered updates on projects and insight into what they are seeing in the NGL market in conjunction with earnings at the end of April and early May. As a result of production shut-ins, TRGP expected lower volumes on the Grand Prix NGL pipeline out of the Permian and through its fractionation trains in Mont Belvieu. However, the company said a substantial portion of its Train 7 and Train 8 fractionation projects are underwritten by minimum volume commitments, with the commitments increasing as volumes ramp up. Train 7 was placed into service in 1Q20, while Train 8 is expected to be completed in late 3Q20. TRGP also expected to utilize any available capacity in its 50-million-barrel NGL storage footprint to take advantage of higher future prices. As a large MLP with diverse operations, Enterprise Products Partners (EPD) detailed the varied impacts of macro headwinds on its assets during its 1Q20 earnings call on April 29. Similar to TRGP, EPD expected to capitalize on the steep contango for many hydrocarbons this spring and location-based differentials to offset potential volume declines. EPD also said that its fractionators were full and expected to remain that way, while NGL pipelines had not seen a decline. NGL exports were another hot topic on earnings calls. EPD management emphasized that its LPG exports have been sold out and could reach another a record high in May. The partnership also noted that over 90% of its LPG export capacity is covered by take-or-pay contracts. In the case of a vessel not showing up, the counterparty would make a payment that would reimburse EPD’s variable costs. While minimal details were provided, TRGP management also noted that its exports are highly contracted on its earnings call. Contract protections can provide comfort to investors who might be concerned about lower NGL export volumes, though company commentary has pointed to steady exports.

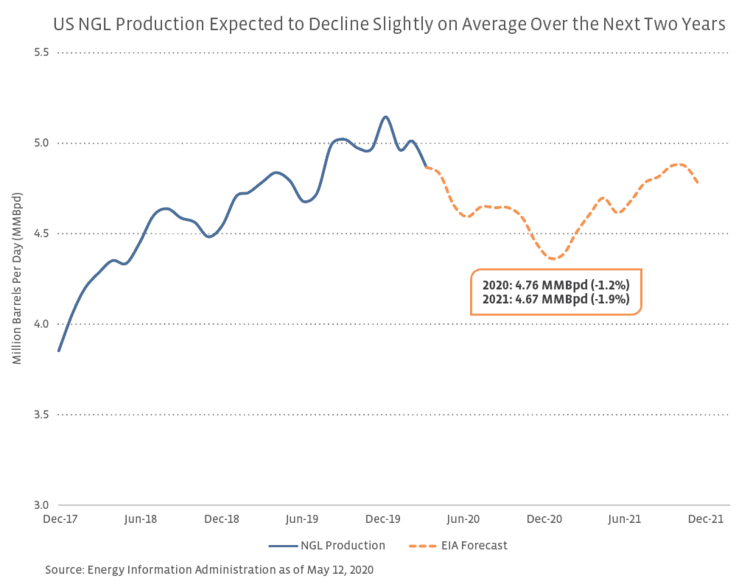

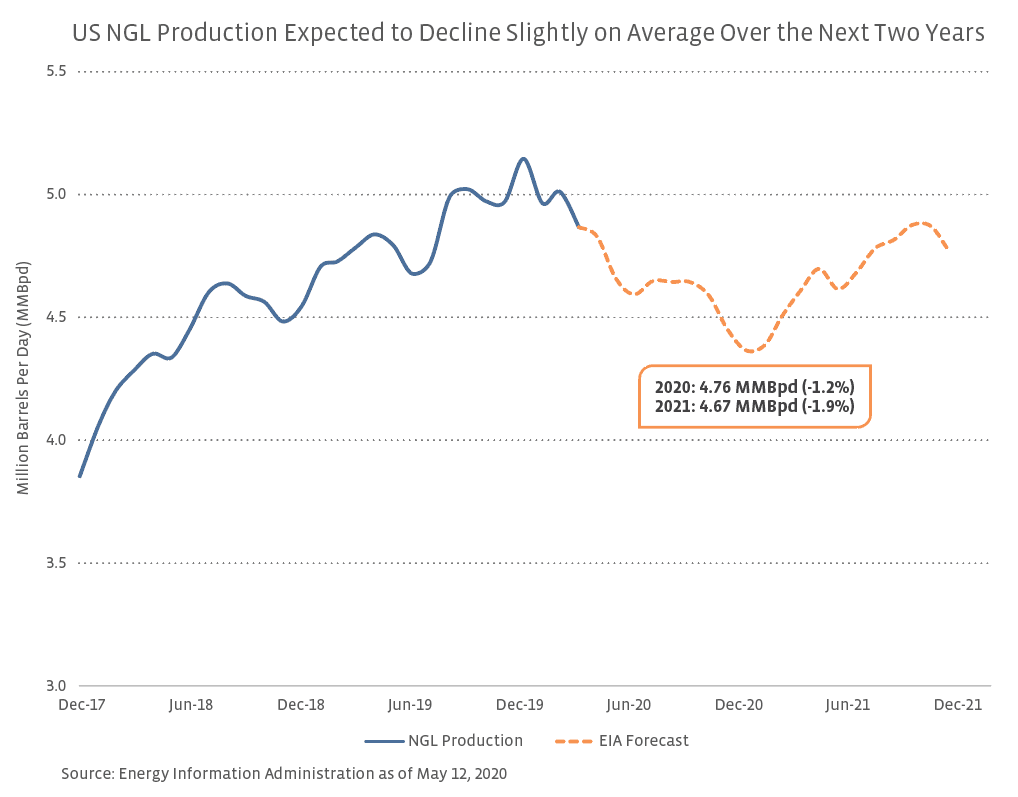

As companies have reduced capital spending in response to production declines (read more) and to increase financial flexibility (read more), NGL projects have been among those that have been deferred or canceled. MPLX (MPLX) said it would no longer pursue the original scope of the Permian to Gulf Coast BANGL NGL pipeline and would defer the fractionation and export capacity associated with the project. Management noted that it remains interested in exploring options for NGL transportation capacity from the Permian even as volume commitments are expected to slow as a result of current production headwinds. Similarly, ONEOK (OKE) suspended its West Texas LPG pipeline expansion, which would have supported up to 100 thousand barrels per day (MBpd) of additional NGL pipeline capacity out of the Permian and was previously slated for completion in 2Q21. The company also said in March that it would reduce the scope of a planned 160-MBpd expansion on the Elk Creek NGL pipeline. The pipeline was completed in December 2019 and extends from the Williston Basin to the Mid-Continent. After placing its Frac VII plant at Mont Belvieu in service in February, Energy Transfer (ET) delayed construction of Frac VIII and now expects it to be in service in 1Q22. ET maintained its expectation to complete two NGL projects in 2020 – the 400-MBpd Lone Star Express NGL pipeline expansion out of the Permian and the 235-MBpd LPG export expansion at Nederland in 4Q20.

Bottom Line

While headwinds remain, NGL prices have begun to improve as production curtailments and stability in demand help tighten the supply-demand balance. Midstream companies face a potential decrease in volumes through NGL pipelines and fractionation facilities as production declines, but the impact may be muted by contract protections such as minimum volume commitments and take-or-pay features. Despite ongoing macro challenges, NGLs may prove to be a relative bright spot for midstream in the coming months.

{kind=link}

{kind=link}