However, Plains management (like everyone) also predicted more M&A activity. Earlier this year, they put a $1 billion revolver in place to take advantage of any potential opportunities. Asset prices have just remained high as sellers insist on valuations reflective of recovered commodity prices (while buyers, of course, base valuations on current prices).

However, there has been more merger activity, particularly between related entities. So the natural question is: what about PAA and PAGP?

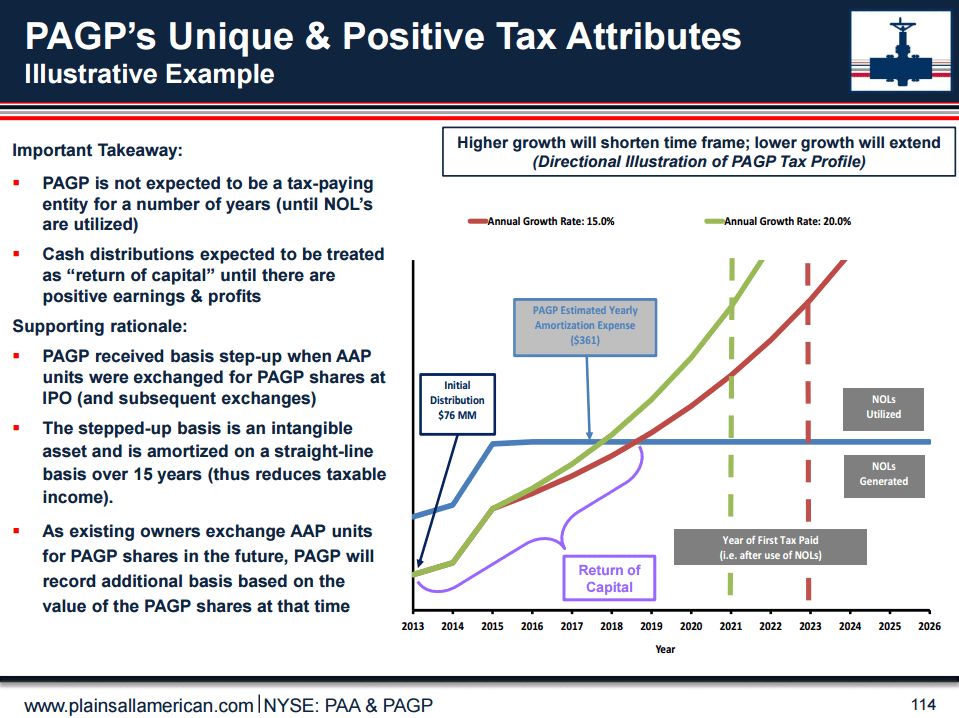

I was not able to attend the New York analyst day in person, so I can’t report on management’s facial expressions when they were asked this inevitable question. A lot of investors are listening for any signal that there is another LP/GP consolidation. Right now, Plains doesn’t seem to be the most likely candidate. There’s just not a strong enough incentive given the 7% expected distribution growth at PAA and 21% distribution growth at PAGP. Plus, PAGP won’t be paying taxes for the next few years. More to the point, PAA has a BBB+ credit rating from S&P, a distinction it shares with only three other MLPs: Enbridge Energy Partners (EEP), Enterprise Products Partners (EPD), and Magellan Midstream Partners (MMP). Plus, should a large acquisition opportunity present itself, PAGP provides optionality for financing at the GP level.

Now to address the 600-pound gorilla in the room: a few weeks before the investor day, Plains had a pipeline rupture, spilling oil into the Pacific Ocean, where it ended up on the Santa Barbara coast. Now, if you are a famous bassist trying to take his family to the beach, you’re probably pretty mad. But if you’re an investor worried about the impact to the bottom line, the financial impact will be mitigated by Plains’ business interruption insurance and reserves for remediation. It’s neither the largest spill, nor the smallest, and despite Plains’ goal of zero incidents, it has hundreds of facilities and thousands of miles of pipelines. Previous spills have resulted in a settlement with the EIA and DOJ of $3.25 million and new operating procedures.

In general, we tend to find what we’re looking for, and hear what we want to hear. Are you looking for a company with a proven track record of growth and $9.5 billion worth of projects yet to build? Are you looking to be horrified at yet another oil spill? Do you want to believe in consolidation despite other more likely candidates? The choice is yours.

{kind=link}

{kind=link}