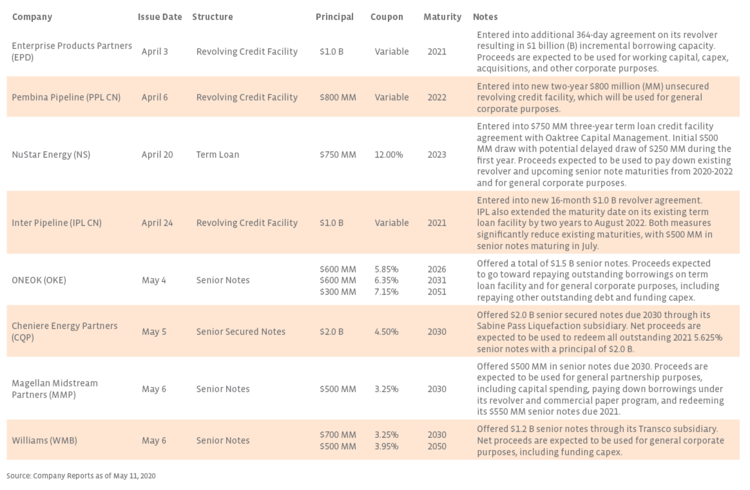

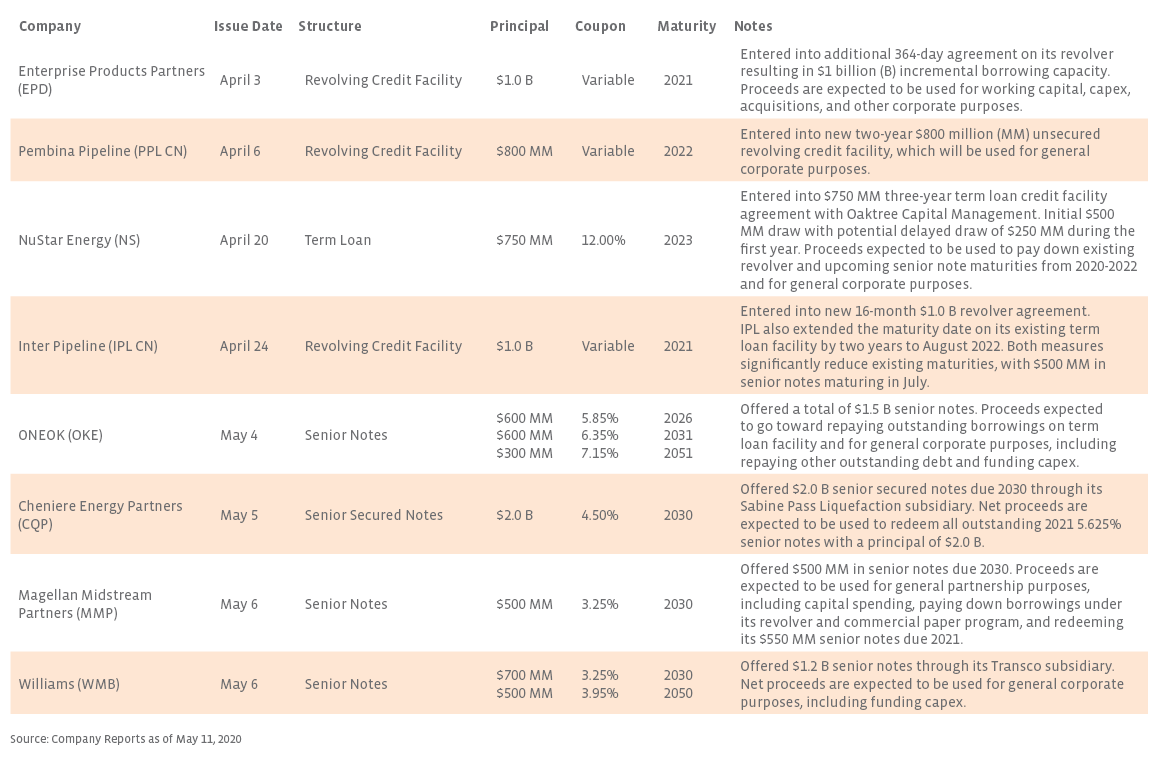

Notably, among the companies listed in the table, NuStar Energy (NS) is the only issuer that is not investment grade. (While Cheniere Energy Partners (CQP) itself is high yield, its Sabine Pass Liquefaction subsidiary that offered the new issue last week holds an investment grade rating from Moody’s.) On April 20 – the same day WTI oil prices went negative for the first time – NS agreed to a $750 million three-year term loan facility with alternative investment firm Oaktree Capital Management. The term loan provided $500 million on the April 21 initial funding date with an additional $250 million delayed draw option available for up to one year following the offering, if needed. In addition to paying down its revolver, NS plans to use the proceeds to repay debt maturing in 2020-2022. NS noted in its quarterly report filed on Friday that it expected to use senior note issuances in addition to borrowings under its revolver or term loan to fund the $750 million in senior note maturities due 2020 and 2021. While the term loan notably reduces short-term liquidity risk, the terms of the agreement are costly given the loan bears a 12.0% annual interest rate, which is expensive relative to prior issuances. For instance, in May 2019, NS priced $500 million in senior notes due 2026 with a coupon of 6.0%.

Over the last week, there have been four notable senior note offerings by two MLPs and two midstream C-Corps, indicating that debt markets are open for some midstream issuers, especially those with good credit. ONEOK (OKE) completed a $1.5 billion offering of senior notes in three tranches at coupons ranging from 5.85% to 7.15%. Notably, the ten-year notes issued last week had a higher coupon of 6.35% compared to a coupon of 4.35% for ten-year bonds issued in March 2019. New issues from CQP and MMP are also expected to contribute to reducing near-term maturities. CQP announced a $2.0 billion offering of senior notes due 2030 expected to help pay down $2.0 billion in 2021 maturities. Similarly, Magellan Midstream Partners (MMP) offered $500 million of ten-year senior notes last week with proceeds, among other uses, going toward a redemption of $550 million of senior notes due 2021. Enterprise Products Partners (EPD) and Canadian companies Inter Pipeline (IPL CN) and Pembina Pipeline (PPL CN) announced new revolving credit facility agreements or extensions to existing agreements. IPL said its measures had significantly reduced near-term debt maturities, with $500 million maturing in July this year.

Recent debt issuances and credit facility agreements indicate that midstream companies with good credit are still able to access debt capital markets at reasonable rates despite the challenges of the last few months. For companies with fewer options as a result of higher levels of debt maturing over the short term, lower credit facility availability, or high yield ratings, debt markets may be accessible but at an increased cost. In response to the challenging macro environment, midstream companies will likely take steps as needed to address short-term maturities and bolster liquidity, complementing other initiatives to improve financial flexibility such as operating cost and capital spending reductions.

Company Releases:

Enterprise Products Partners (EPD)

Pembina Pipeline (PPL CN)

NuStar Energy (NS)

Inter Pipeline (IPL CN)

ONEOK (OKE)

Cheniere Energy Partners (CQP)

Magellan Midstream Partners (MMP)

Williams (WMB)

{kind=link}