While the decrease in the corporate tax rate is permanent barring new legislation, the reduction in the top individual tax rate and the QBI deduction expire after 2025 unless an act of Congress extends the provisions. Economic advisers in the Trump administration have previously floated the idea of “Tax Cuts 2.0.” The rumored plan includes reducing the individual tax rate to 15% for middle-income taxpayers, lowering the number of individual tax brackets, and making permanent some or all of the tax cuts from TCJA. Demonstrated progress on firming a proposal has been limited, with the most recent update from February suggesting the campaign would release a plan around September. However, clearly much has changed since February given significant spending to stimulate the economy in the wake of COVID-19. If there were to be a second term for the Trump administration, tax policy would likely remain largely the same.

What would a Biden presidency mean for MLP taxation?

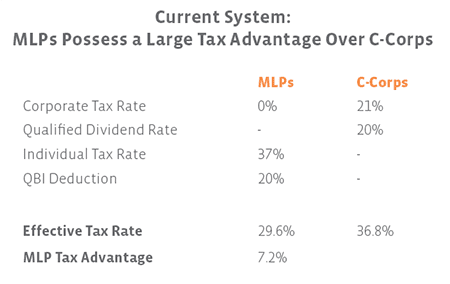

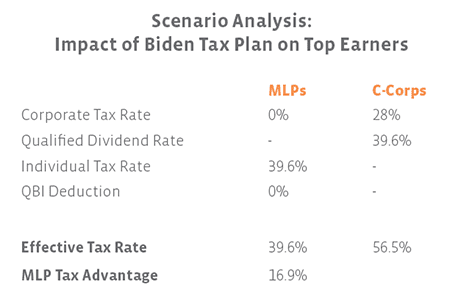

While MLPs currently possess a significant tax advantage over C-Corps for individual investors, tax policies can obviously change under different presidential administrations and Congresses depending on the balance of power. Given that it is an election year, it seems appropriate to also evaluate the potential tax agenda of presumptive Democratic presidential nominee Joe Biden. First reported by media outlets in December, the Biden tax plan is expected to include an increase in the corporate tax rate from 21% to 28%, which would still be lower than the 35% rate prior to the TCJA. Corporate taxation is also expected to include a 15% minimum tax to ensure larger companies pay some portion of taxes. For individuals making more than $400,000, the 20% QBI deduction would be repealed for pass-through investments, and the highest income tax rate would revert to 39.6% from 37%. The plan would also reportedly tax long-term capital gains and qualified dividends at ordinary income rates for those making more than $1 million in income. The tables below include these assumptions and show their impact on the effective rates for MLPs and C-Corps, excluding the Medicare tax.

Notably, for top earners, the tax advantage of investing in MLPs would increase from 7.2% to 16.9%, enhancing the attractiveness of the MLP structure relative to the C-Corp structure. The larger MLP advantage stems from the higher corporate and qualified dividend rates, which would offset a repeal of the QBI deduction and an increase in the tax rate for the highest income tax bracket. While this example is kept simple for illustrative purposes, it is one reason why MLPs may not be rushing to convert to C-Corps before the election (read more). Structure questions have also likely taken a backseat to other concerns given macro headwinds this year, although management teams have fielded a few questions about potential conversions recently. On its 1Q20 earnings call on April 29, Enterprise Products Partners (EPD) co-CEO and CFO Randy Fowler said he expected taxes to increase for everyone in the future as a result of significant government stimulus spending, and the partnership is mostly watching to see what happens. Magellan Midstream Partners (MMP) also discussed taxes among its criteria for evaluating a conversion to a C-Corp structure on its 4Q19 earnings call on January 30. CEO Mike Mears said the company takes a long-term present value of MMP’s tax-efficient MLP structure and analyzes it against the present value of a C-Corp structure. Because C-Corps have to eventually pay taxes following a conversion, MMP believes there is more value in remaining an MLP but also evaluates its structure on an ongoing basis.

Bottom Line

MLPs continue to retain a tax advantage over their C-Corp counterparts, which could potentially widen under a Biden presidency if tax rates are raised. While taxation is not the only factor in an analysis of potential C-Corp conversions, MLPs will continue to weigh their tax advantage against other considerations.

{kind=link}

{kind=link}