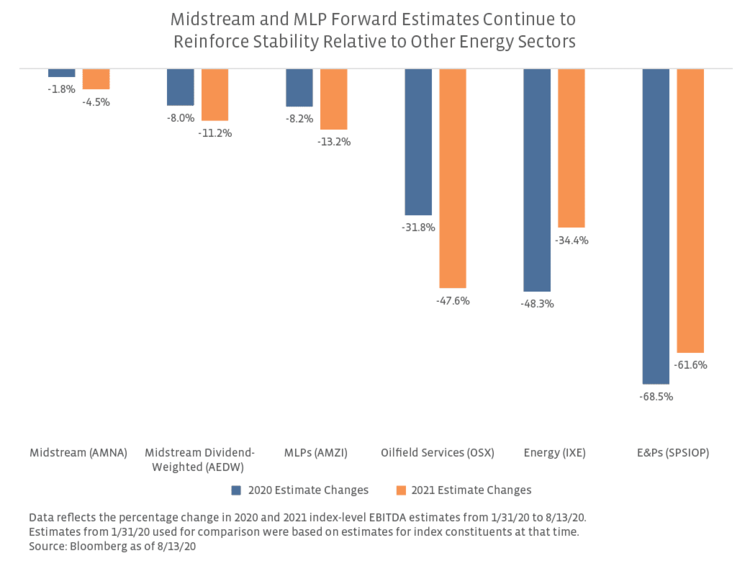

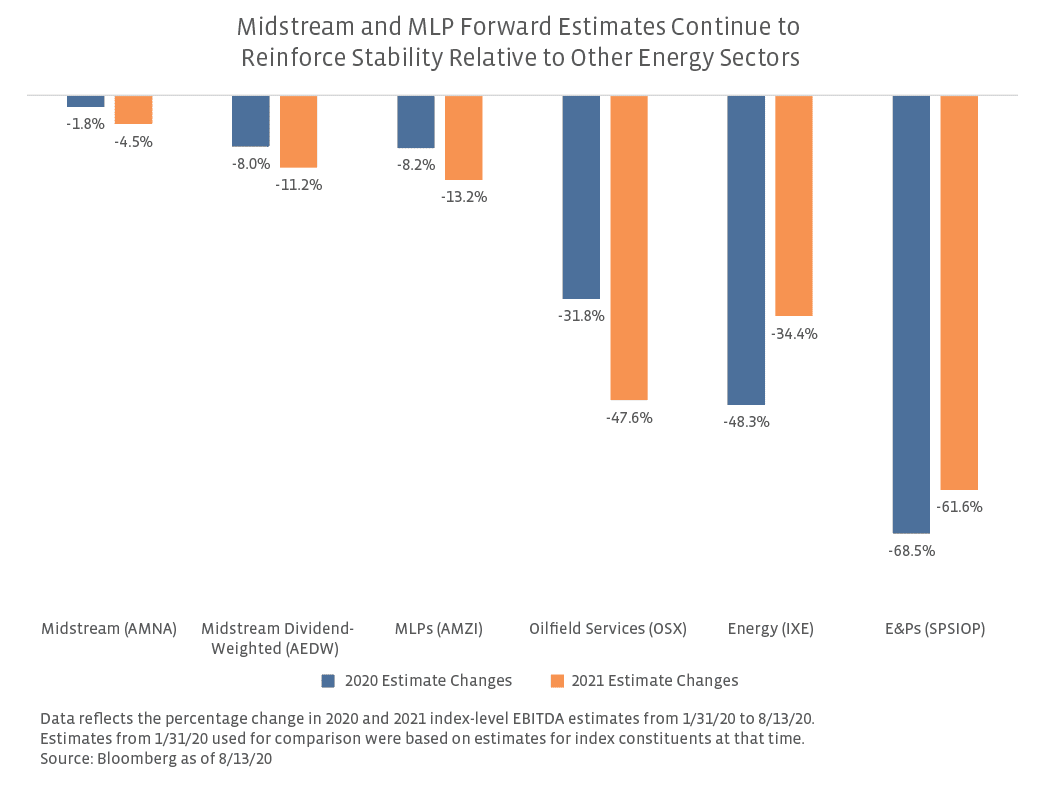

Midstream EBITDA estimates have been resilient in contrast to other sectors of energy because of midstream’s fee-based business models and contract protections such as minimum volume commitments, which have helped to shield the space (read more). Despite forward EBITDA estimates barely budging for midstream since oil’s collapse, especially compared to other energy sectors, the space has not been spared from weakness in equity price performance as discussed below – a point of frustration for long-term midstream investors.

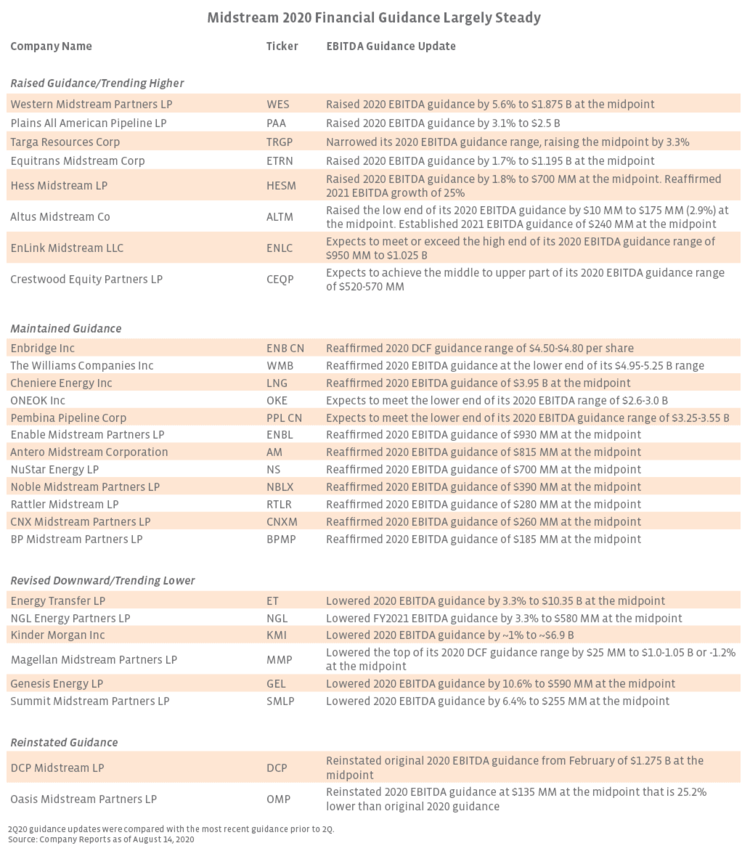

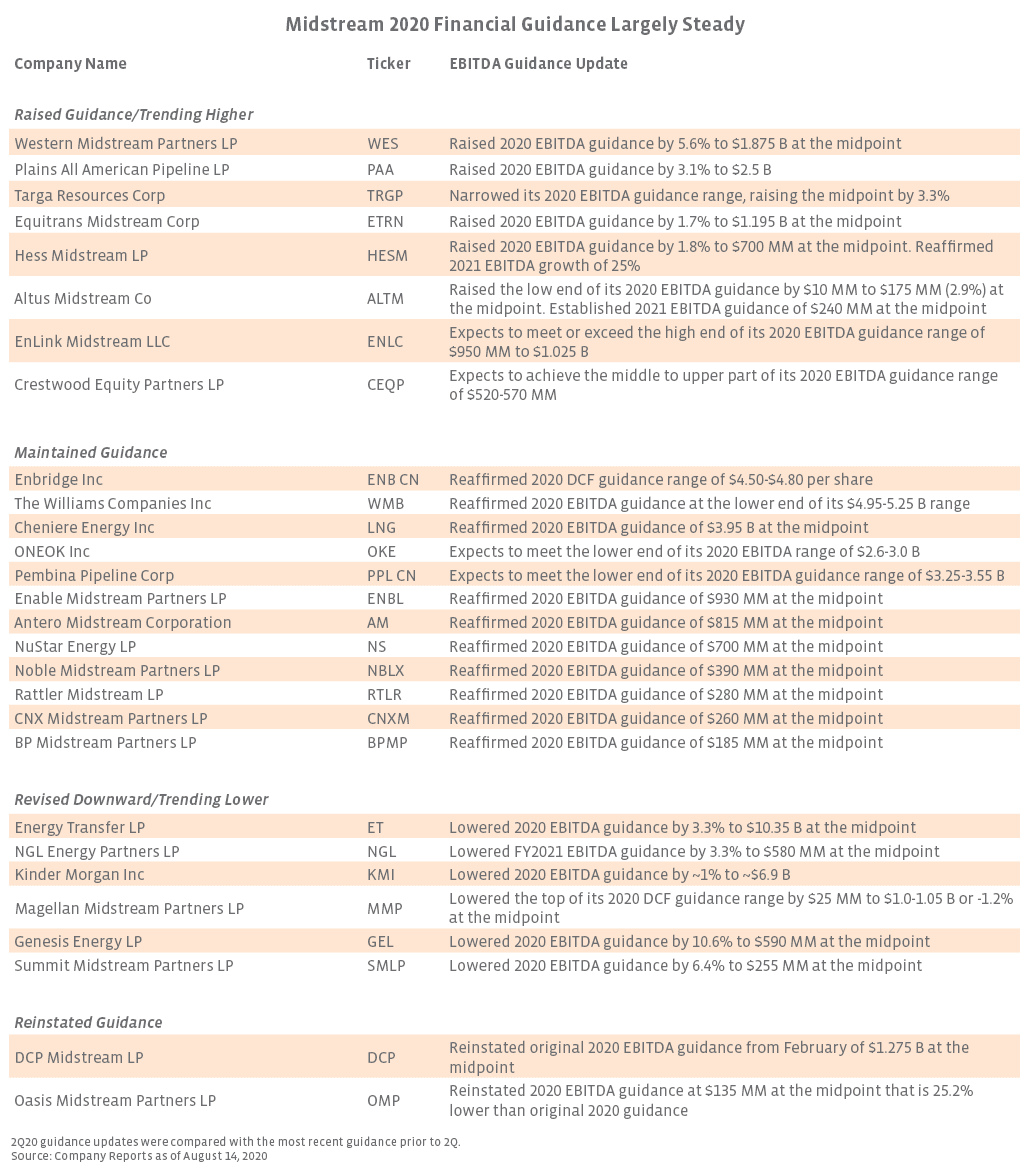

2020 outlooks largely maintained or raised with a few notable exceptions.

Despite a challenging macro environment in 2Q, full-year 2020 guidance for midstream was largely resilient with only a few companies trimming their projections. The table below shows select 2020 EBITDA guidance updates announced with 2Q results and compares them with the outlook in place prior to earnings season. For example, if a company lowered its 2020 outlook in March, the table below would compare to the March guidance instead of the outlook from the start of this year. To be clear, some companies, including Williams (WMB), Enbridge (ENB), and Cheniere (LNG) have maintained guidance issued prior to the onset of the COVID-19 pandemic. Overall, guidance was largely maintained or increased relative to expectations before earnings season. Of the 28 companies listed below, 20 raised or maintained guidance, including those expecting to come in at the low-end of the provided range. A handful of companies also narrowed guidance ranges or provided qualitative expectations for where guidance is trending.

The number of companies raising or maintaining guidance helps reinforce the stability and reliability of midstream cash flows despite a tumultuous macro environment. Twelve companies reaffirmed their 2020 EBITDA guidance in 2Q20, including large C-Corps WMB and LNG and MLPs Enable Midstream (ENBL) and NuStar Energy (NS). Two companies – DCP Midstream LP (DCP) and Oasis Midstream Partners LP (OMP) – reinstated guidance after previously pulling guidance for the year. The large companies that announced lower guidance generally had small revisions, such as Kinder Morgan (KMI), which lowered its EBITDA guidance by 1%, and Magellan Midstream Partners (MMP), which trimmed the top end of its distributable cash flow guidance by $25 million (down 1.2% at the midpoint). Notably, Energy Transfer (ET) reduced its EBITDA guidance by 3.3% to $10.35 billion at the midpoint and cited the uncertain pace of the recovery in production volumes and commodity prices. Setting aside OMP’s reinstated guidance below prior expectations, the largest negative guidance revisions came from a few smaller midstream names, including Genesis Energy (GEL) and Summit Midstream Partners (SMLP). Of note, GEL has been negatively impacted by challenged economics and cancellations within its soda ash business, a non-midstream activity prone to commodity price volatility.

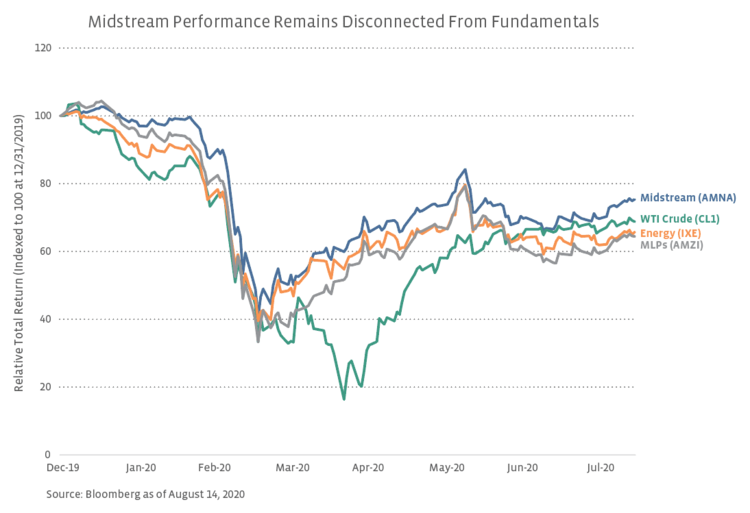

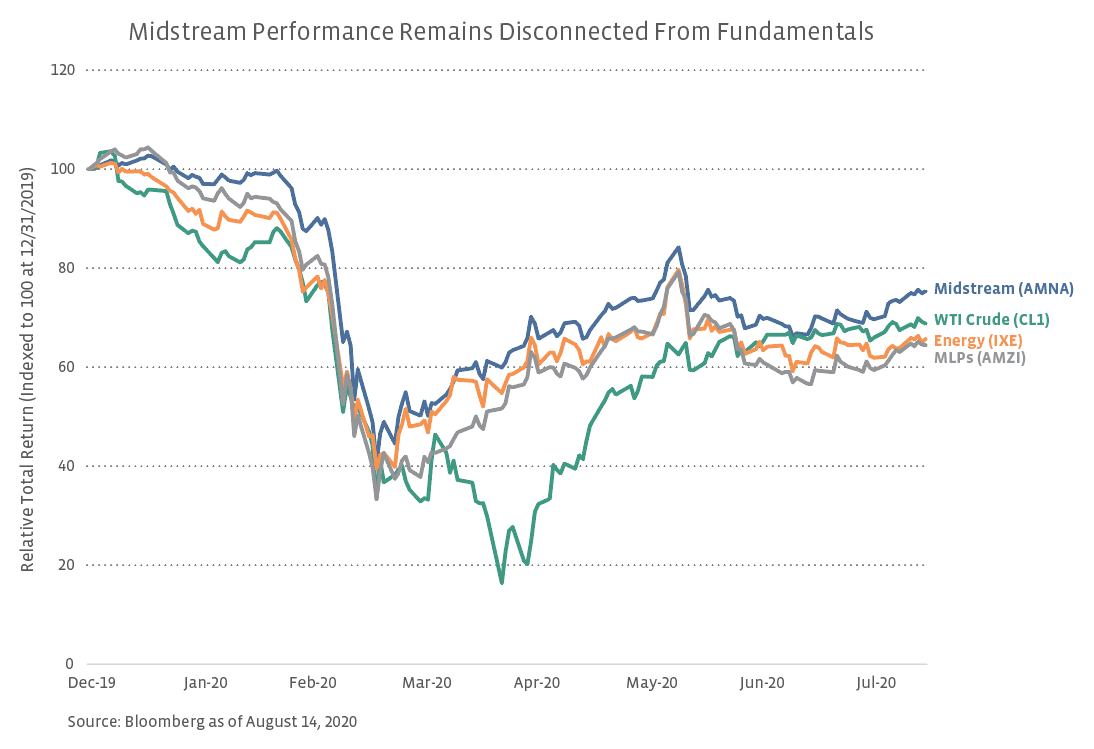

EBITDA estimate revisions and company guidance updates suggest a disconnect with performance.

The stability in the outlook for midstream EBITDA in 2020 and 2021 contrasts starkly with the volatility and weakness in midstream equities this year. Midstream, as represented by the AMNA Index, is down 24.6% year-to-date through August 14, while MLPs (AMZI Index) are down 35.5% on a total-return basis (see chart below). Even though EBITDA estimates for midstream have been much more resilient, the equity performance for midstream has been more in line with broader energy as represented by the IXE, which is down 34.3% on a total-return basis. This disconnect between performance and fundamentals suggests potential room for improvement if midstream companies can remain financially disciplined and execute consistently. Notably, midstream and MLPs have performed in line or better than other sectors of energy and the broader market since earnings began, which could indicate some improvement in sentiment or potentially some rotation into the space to capitalize on dividend announcements. From July 22 through August 14, the AMEI gained 5.8% on a total-return basis, while the AMZI was up 3.5%. For comparison, broader energy (IXE) fell 1.0%, WTI crude rose 0.1%, and the S&P 500 increased 3.5% over the same period.

Bottom Line

Though EBITDA guidance adjustments were not universally positive for the second quarter, the defensiveness of the midstream business model is apparent in the significant number of companies maintaining or raising guidance. The stability of 2020 and 2021 EBITDA estimates in light of considerable stress is a clear differentiator for midstream relative to other energy sectors, yet midstream performance has been relatively in line with broader energy. Though midstream outperformed during earnings season, a continuation of that trend will require sustained execution and discipline as well as fresh investor interest in the space.

Company Releases

Western Midstream Partners LP (WES)

Plains All American Pipeline LP (PAA)

Targa Resources Corp (TRGP)

Equitrans Midstream Corp (ETRN)

Hess Midstream LP (HESM)

Altus Midstream Co (ALTM)

DCP Midstream LP (DCP)

EnLink Midstream LLC (ENLC)

Crestwood Equity Partners LP (CEQP)

The Williams Companies Inc (WMB)

Cheniere Energy Inc (LNG)

Enable Midstream Partners LP (ENBL)

Antero Midstream Corporation (AM)

NuStar Energy LP (NS)

Noble Midstream Partners LP (NBLX)

Rattler Midstream LP (RTLR)

CNX Midstream Partners LP (CNXM)

BP Midstream Partners LP (BPMP)

Energy Transfer LP (ET)

Genesis Energy LP (GEL)

NGL Energy Partners LP (NGL)

Kinder Morgan Inc (KMI)

Magellan Midstream Partners LP (MMP)

Summit Midstream Partners LP (SMLP)

Oasis Midstream Partners LP (OMP)

ONEOK Inc (OKE)

Pembina Pipeline Corp (PPL CN)

Enbridge Inc (ENB CN)

{kind=link}

{kind=link}

{kind=link}