Summary

- A recent survey of over 600 financial advisors shows MLPs are known for their income, but their tax advantages are not well understood.

- Regarding the ongoing energy transition, survey results suggest that most advisors expect oil and gas infrastructure to continue operating for decades.

- Two-thirds of survey respondents agree that midstream investing is compatible with ESG investing.

Today’s note discusses key observations from a recent survey of advisors about the midstream/MLP space. The survey results provide a window into areas of misconception about the sector as well as views on topical issues such as the energy transition and ESG considerations. The Alerian-commissioned, third-party survey was conducted in late 2021 and includes the views of more than 600 financial advisors. Accompanying this note, Alerian has also published “Dispelling Myths about Midstream Investing,” which concisely addresses eight common misperceptions. Please see the resources section at the end of this note for additional information.

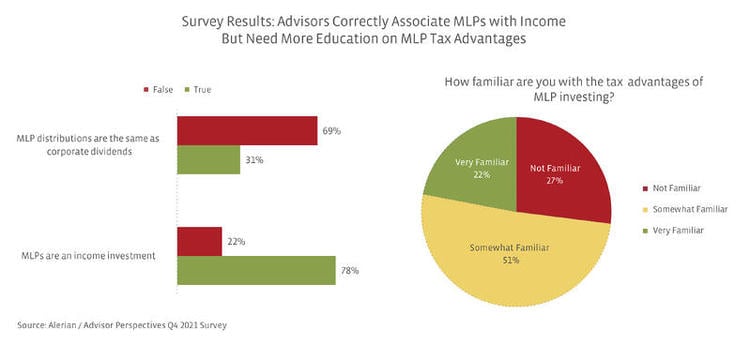

MLPs are known for their income, but tax advantages are not well understood.

Based on survey results, advisors largely recognize MLPs as income investments – a proper association given that the Alerian MLP Infrastructure Index (AMZI) has had an average yield of 7.6% over the last ten years. Most respondents also realize that MLP distributions are not the same as the dividends paid by corporations. However, the tax advantages of MLPs – including the potential for tax-deferred income – are not well understood. In fact, only 22% of respondents indicated they are very familiar with the tax advantages of MLPs. Indeed, several respondents noted that more education was necessary to make midstream/MLP investing more attractive. While the resources below provide more detail, in short, MLPs are pass-through entities and do not pay federal taxes, thus they do not have the double taxation associated with corporate dividends. MLPs have historically provided attractive income that is largely a tax-deferred return of capital.

It is possible to get MLP exposure without a K-1.

Admittedly, the tax advantages of MLPs are not without some complexity. Specifically, a direct investment in an individual MLP will result in a Schedule K-1 being issued for tax reporting. Multiple respondents cited K-1s as an obstacle to investing in MLPs. However, there are many exchange-traded products and funds that provide diversified exposure to MLPs and issue a Form 1099 instead of a K-1. If investors have written off MLP investing solely because they do not want a K-1, they are needlessly missing out on an attractive opportunity for potential tax-advantaged income and total return.

Advisors appreciate that the energy transition will take decades, but midstream should still prepare.

Investor questions about midstream and the potential impact of the energy transition often seem to underestimate how long energy transitions take, but survey results suggest that advisors largely expect oil and gas infrastructure to operate for decades. Notably, 75% of survey respondents did not believe that oil and natural gas pipelines would become obsolete in the next 25 years. When asked when global oil consumption would become relatively obsolete, 63% of respondents believed it would be more than 30 years. To be clear, investors are justified in raising questions around the impact of the ongoing energy transition for midstream. This is especially true for MLPs given that their tax-deferred income makes them attractive for retirement or estate planning, which can result in longer holding periods.

While Alerian agrees that energy infrastructure will be used for decades to come, midstream companies have a role to play in the energy transition and should not be caught flat-footed as the energy landscape evolves. Companies are actively evaluating ways to participate in this evolution, and some have even partnered with other energy firms to pursue opportunities around hydrogen, carbon capture, and renewable fuels (read more). The ability to safely move and store energy – whether it is oil, natural gas, renewable fuels, hydrogen or byproducts like captured carbon dioxide – will be needed for decades to come.

Midstream investing can be compatible with ESG investing.

The growing focus on ESG investing has not been lost on midstream/MLPs. In recent years, energy infrastructure companies have been focused on reducing emissions, improving governance and transparency around ESG metrics, and better highlighting the safety practices that are critical to the industry. Several midstream companies have announced net-zero emission targets by 2050, including Enbridge (ENB), Williams (WMB), Gibson Energy (GEI), DT Midstream (DTM), and others. Two-thirds of survey respondents agreed that midstream investing is compatible with ESG investing – a point that Alerian has often highlighted in past research (see resources below).

Bottom Line:

Based on survey responses, advisors largely understand that MLPs provide income, but additional education is needed around the tax advantages of that income and ways advisors can access the space without receiving a K-1. Responses indicate that the energy transition and the ESG credentials for midstream are not sticking points for investment decisions. For its part, Alerian is committed to educating advisors and other investors about the benefits of investing in midstream/MLPs. For more information about the realities of investing in the space, please see “Dispelling Myths About Midstream Investing.”

Resources:

MLP Taxation:

MLP Taxation: The Benefits and What You Need to Know

MLP Primer: Tax Efficiency and Accounting with MLP Investing

Energy Infrastructure Council: Basic MLP Tax Principles

MLP and Energy Infrastructure Investment Products:

MLP Exchange Traded Products Explained: ETNs and ETFs

Decisions, Decisions: Demystifying MLP Investment Options

ESG:

Can Midstream/MLPs Be a Green Investment?

Midstream/MLPs: The Unsung ESG Push

Midstream Partnering for a Cleaner Tomorrow

Midstream Pulling Multiple Levers to Reduce Emissions

The Alerian MLP Infrastructure Index (AMZI) is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (AMUB).