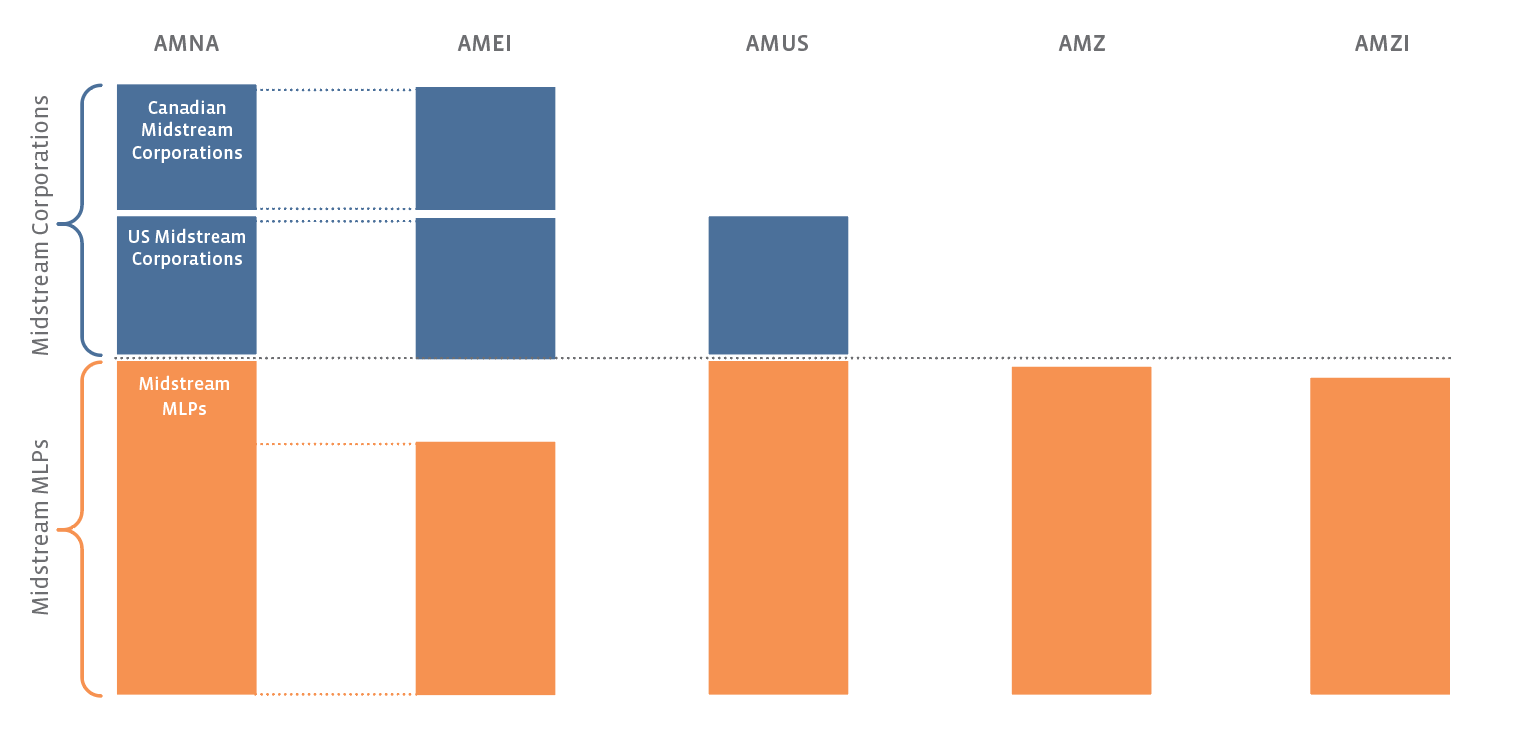

For illustrative purposes only, not drawn to scale

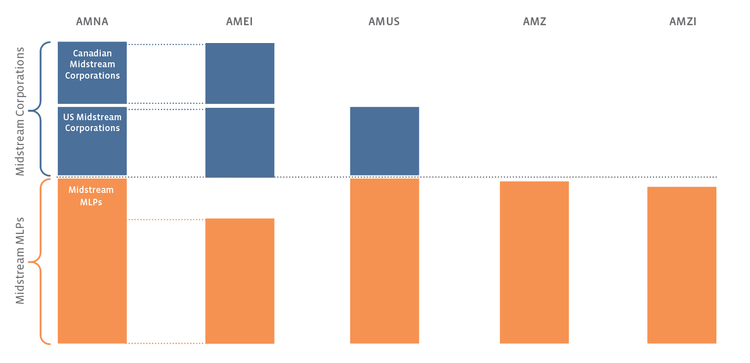

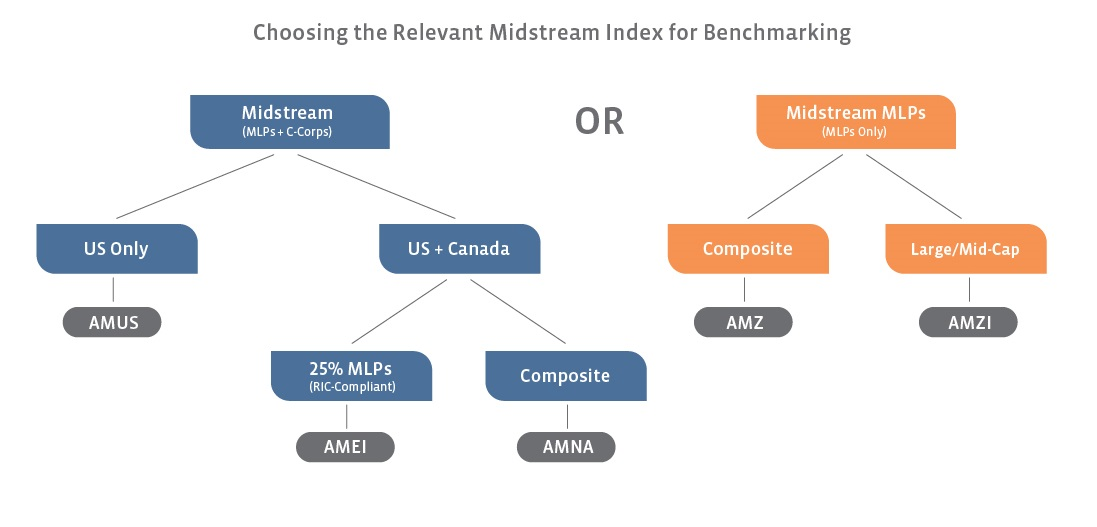

Alerian Midstream Energy Index (AMNA) – AMNA is a broad composite of the entire North American energy infrastructure universe. The only requirements for inclusion are that constituents must have principal executive offices in the US or Canada and must earn a majority of their cash flows from midstream activities. Index constituents can be MLPs or C-Corps.

Alerian Midstream Energy Select Index (AMEI) – AMEI is a more liquid and investable subset of AMNA. In addition to AMNA’s criteria, AMEI constituents must also have a minimum median daily trading volume of $2.5 million for the six months prior to the index’s data analysis date. Additionally, MLPs are capped at 25% of the index, making the index a fitting benchmark for RIC-compliant products.

Alerian US Midstream Energy Index (AMUS) – Simply put, AMUS is AMNA without the Canadian exposure. Only midstream MLPs and US C-Corps are included in the index. AMUS captures roughly 71% of the AMNA Index.

Alerian MLP Index (AMZ) – The AMZ, the first real-time MLP Index, is a composite of midstream MLPs. Each AMZ constituent must have a market capitalization of at least $75 million. Currently, there are 32 constituents that meet these criteria.

Alerian MLP Infrastructure Index (AMZI) – AMZI is a more liquid and investable subset of AMZ. Rather than require a minimum market capitalization, AMZI constituents must have a minimum median trading volume of at least $5 million for the six months prior to the index’s data analysis date. Additionally, AMZI constituents must have declared a distribution for the trailing two quarters. AMZI captures 95% of the AMZ Index by market cap.

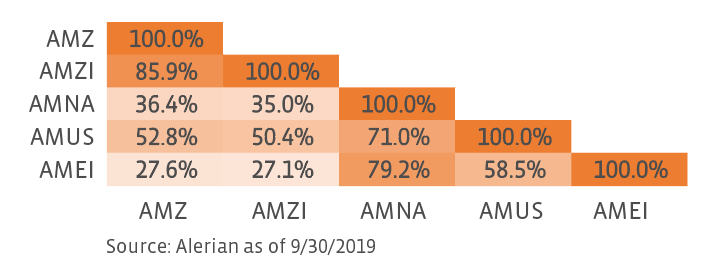

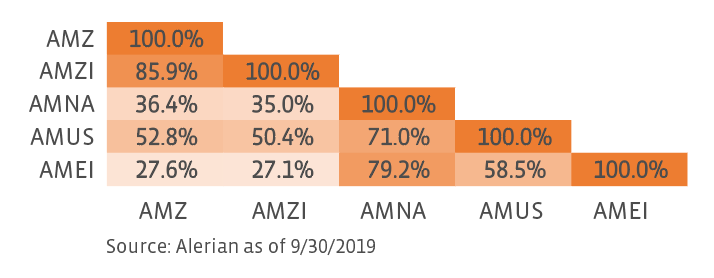

The graphic below shows the overlap between Alerian’s midstream indexes. Unsurprisingly, there is significant overlap between the AMZ and AMZI as MLP-focused indexes. AMEI has high overlap with AMNA as the investable subset of the broad composite index.

How have Alerian’s indexes evolved with changes in the midstream landscape?

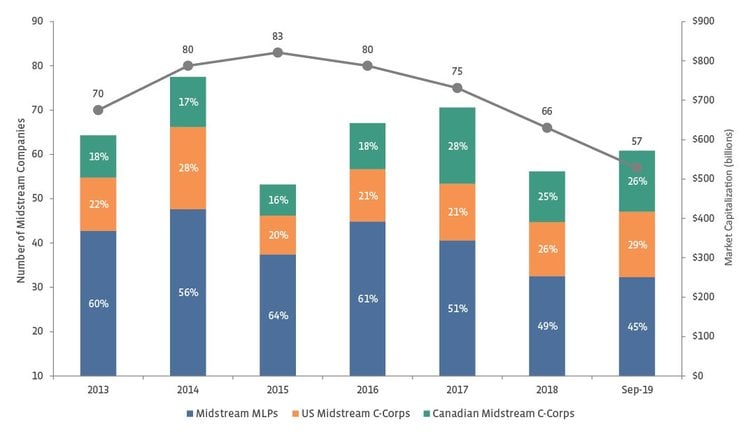

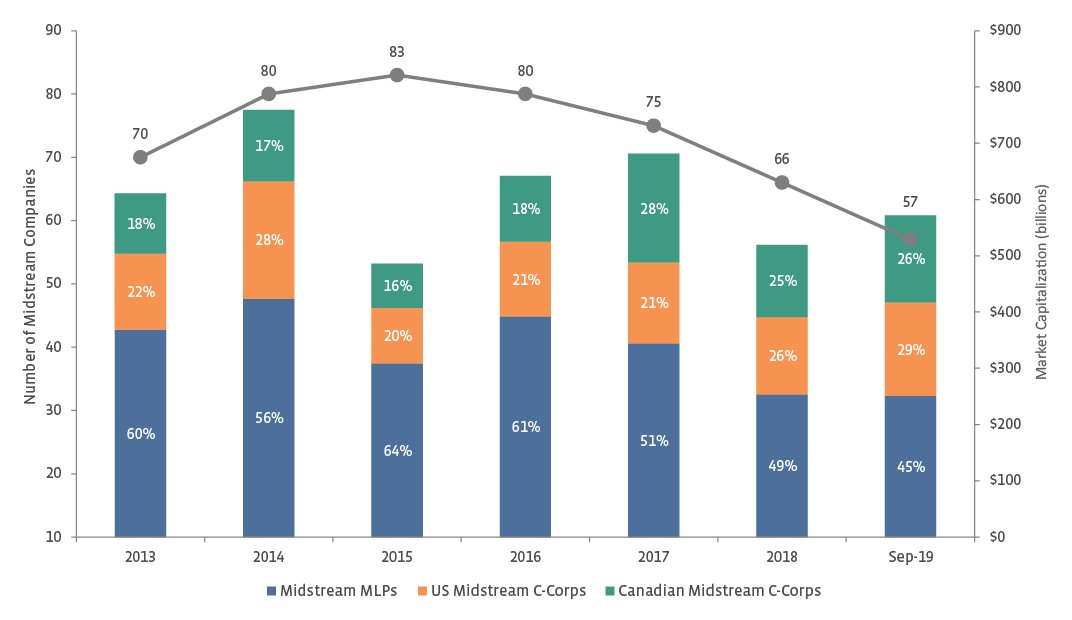

This summer, we discussed MLP consolidations and the impact that they could have on investors, but it is worthwhile to analyze how consolidations may influence one’s choice of midstream benchmarks. As a result of consolidations and growth in Canadian midstream names, MLPs do not capture the entirety of the North American energy infrastructure landscape. In 2016, midstream MLPs made up over 60% of the North American midstream market capitalization. At of the end of September, MLPs made up 45% of the North American midstream market capitalization.

Source: Alerian as of 9/30/2019

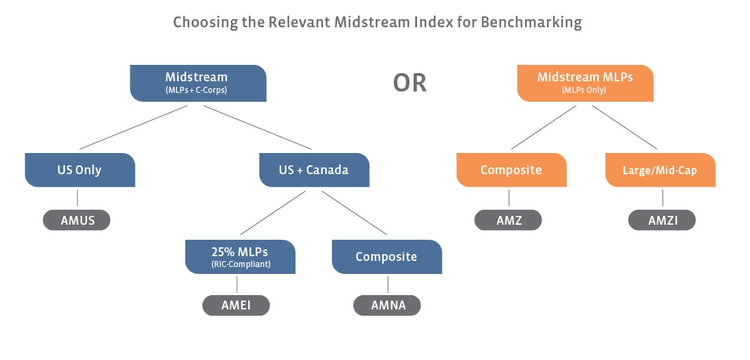

As a result of the smaller MLP universe and higher market cap of US and Canadian corporations, AMNA and AMUS were both launched in June 2018. Due to their tax-agnostic construction and inclusive criteria, AMNA and AMUS are the best representations of the North American and US midstream sectors overall, respectively. Additionally, both indexes can be used as benchmarks for products that aim to provide broad energy infrastructure exposure, particularly separately managed accounts (SMAs) that include MLPs and C-Corps.

While the AMZ and AMZI may not fully capture the broader midstream universe, they provide accurate representations of the midstream MLP space for investors solely focused on MLPs. AMEI, due to its 25% MLP limitation, can function as a benchmark for RIC-compliant MLP products. The decision tree below outlines the appropriate midstream index for benchmarking based on the desired representation.

How do Alerian’s indexes fit into access products?

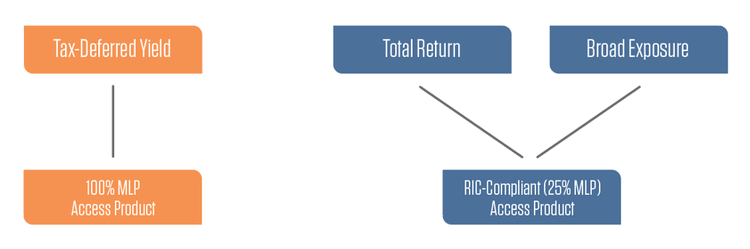

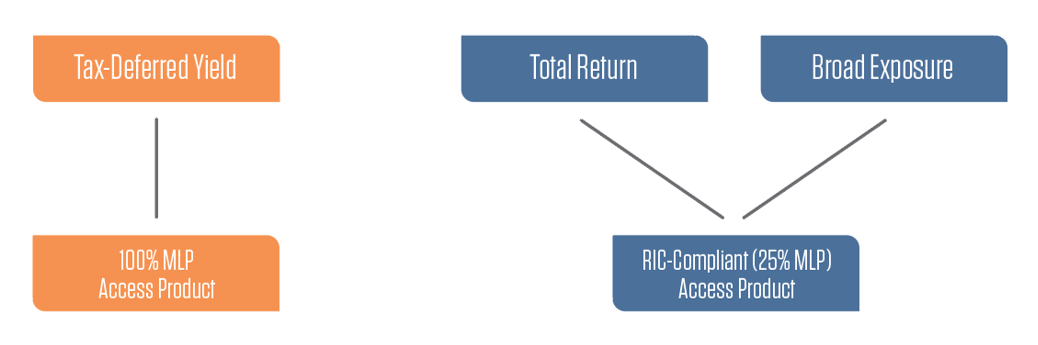

In addition to acting as benchmarks, Alerian’s indexes can also function as the underlying index for midstream or MLP access products. As for which index works best in the product structure, there is no universal answer; It depends entirely on the needs of the individual investor. A 100% MLP product is best suited for investors seeking higher after-tax income, while investors looking for broader midstream exposure with a total-return focus would generally prefer a RIC-compliant product. Additionally, an investor’s outlook for midstream performance can determine which access product is right for them. Ultimately, Alerian’s midstream indexes are well suited to fit a wide variety of investor needs. For a broader discussion of the different types of MLP and midstream access products, please see our note on the topic from January (read more) or the Energy Infrastructure Investing section of our Energy Infrastructure Primer. Please note that Alerian is not an investment advisor, and this post does not constitute investment advice (please see our disclaimers here).

Bottom Line

Alerian offers a broad suite of midstream indexes in order to provide both investors and asset managers with reliable representations of the energy infrastructure sector. As the midstream space has evolved, Alerian has added new indexes to meet the benchmarking needs of stakeholders, including last year’s launch of the AMNA and AMUS indexes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}