MLPs are on track to have their third worst year in history and unlike all the other bad years, there’s not a broader macro crisis going on at the same time. Unlike in 2008, there is no financial crisis closing access to capital markets. Unlike 2015, crude oil prices aren’t collapsing precipitously and taking the entire energy-related economy with it. In fact, we’re now, as one colleague likes to say, at “all-time, all-time, all-time” highs in nearly every sector.

So here we are in 2017. The broader market and economy have had a remarkable string of successes, capital markets are open and active, and even WTI crude oil has started to recover from summer lows in the $40s, staying rangebound around $50-$55. I am neither a Pollyanna nor a Pangloss—there has been some bad news coming out of various companies, but there has been no material change in fundamentals to explain the double-digit losses investors are experiencing this year. US energy demand remains stable, pipelines are flowing, and long-term contracts are in place. Given that, let’s examine some UNfundamentals of current MLP trading.

Shifting MLP Valuation Model

Using the verb “shifting” is a bit of a misnomer. Alerian has advocated valuing MLPs on a P/DCF (Price / Distributable Cash Flow) basis for over a decade now. But, that method takes a lot of work since data services like Bloomberg, Thompson Reuters, or Yahoo! Finance tend to give only incomplete estimates, not like in other sectors where these services can provide accurate and complete metrics like P/E or EV/EBITDA. Yield has commonly been substituted as a quick estimate, but that requires both that distributABLE cash flow = distributED cash flow and that the market is rational for unit prices.

Those days are gone. MLP management teams, reasonably frustrated that investors have stopped rewarding them for growing distributions, have started to (1) slow their distribution growth (Enterprise Products Partners (EPD) announced it will now grow distributions by $0.01 per year instead of $0.02), (2) halt it altogether (EnLink Midstream Partners (ENLK) has maintained distributions at $0.39/quarter for the past two years), or (3) even cut distributions (Genesis Energy (GEL) is a recent example). Instead of returning nearly all cash to unitholders and getting no reward in unit performance, they will use it to self-fund growth projects.

Volatility is to be expected as investors digest this tectonic shift in the way MLPs return value to unitholders. Would a rational investor care whether an investment grew via distribution growth or unit price growth? All taxes being equal, certainly not. But again, welcome to our irrational world.

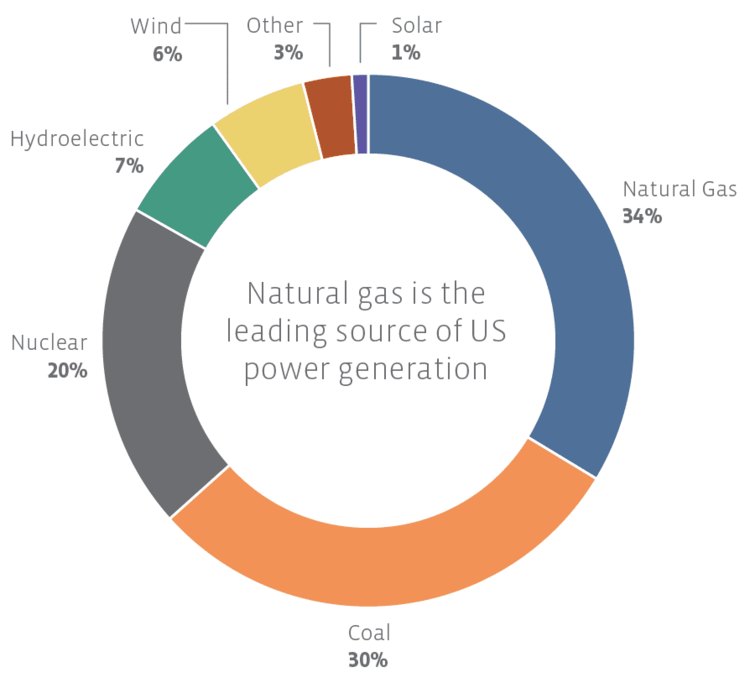

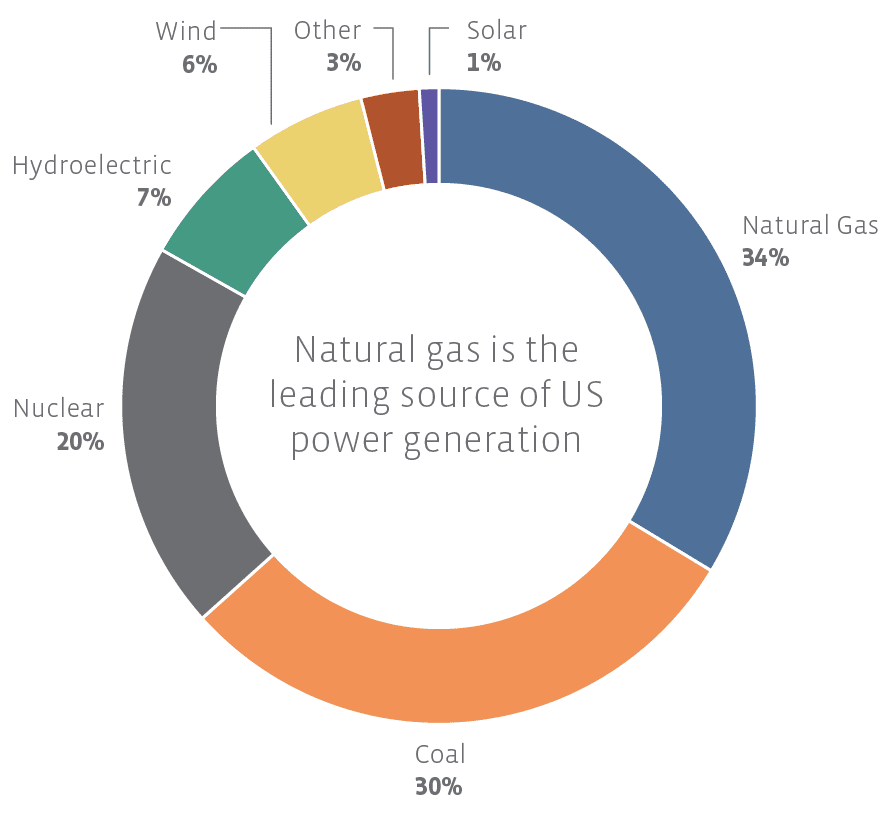

Forgotten Natural Gas

Does anyone remember that roughly 50% of the pipelines in the US move natural gas? Of the remaining 50% that do move petroleum and petroleum products, does anyone care about the ones moving refined products like gasoline and jet fuel that see steady demand? Or the fact that refined product exports are at an all-time high?

Crude correlations are in the news and in our inbox practically every day. It’s not that the price of crude doesn’t matter—it does. In fact, it matters very much to those MLPs providing takeaway capacity for oil wells in production areas like the Permian Basin and the Bakken. Those MLPs are not all MLPs.

To be sure, we’ve had warm winters for a couple years now, so there’s been less demand for natural gas for heating. But what about the steady increase in exports of natural gas to Mexico that we’ve seen over the last few years? What about the possibility of significant LNG exports that began with the startup of Cheniere Energy Partners’ (CQP) Sabine Pass LNG terminal in 2016 and is set to grow as additional LNG export facilities come online?

Source: EIA

Another way this gets forgotten is investors’ practically panicked concern that electric vehicles are going to wipe out all value in MLP investments—by tomorrow. We wrote an entire article on electric vehicles, but let me explain even more why Tesla production numbers shouldn’t be inversely correlated with MLP prices. Worldwide, there are one billion vehicles on the road, and only two million electric vehicles, or 0.02% of the total fleet. If the Paris targets are hit, then in 2035, there will be 100 million EVs against 1.8 billion total vehicles, or 5.5% of the global fleet. The internal combustion engine is not that easily forgotten. Plus, electricity doesn’t magically appear out of the air. More US electricity is generated by natural gas fired power plants than by any other source. So, those investors wanting a second- or third-derivative way to play the electric vehicle theme should be investing more money in natural gas MLPs, not less.

Money Flows Bely Sentiment

As the old quip goes, when the market’s moving down, there are more sellers than buyers. However, looking at asset flows, at least into products, shows demand is still there. For 2017, an average of $350-$400 million has flowed into MLP ETFs and mutual funds every month. Drilling down further to the largest MLP ETF: the Alerian MLP ETF (AMLP), there have been fund flows of roughly $1.4 billion in the first nine months of the year.

Some of this move is likely a shift of money from closed-end funds into more transparent products or products without leverage. Some investors may be taking tax losses in individual names early this year and moving funds into broader, more diversified products. Others may be making their first MLP allocations ever.

Beyond retail investors, private equity money has been active in MLPs and will likely provide a floor for valuations. For example, this summer, Blackstone bought a 32.4% stake in the unfinished Rover Pipeline from Energy Transfer Partners (ETP) for $1.57 billion. Private equity has a longer-term holding period, so given that flexibility, their management teams have decided that this space and its assets are attractive at these levels.

The Base Case Is Worth Something

When MLPs trade down near these levels, it’s time to ask the hard question: Is the price decline merely an overreaction by panicked sellers (or those with other motivations such as tax loss harvesting), or is this the warning shot of something far darker—that MLPs will be unable to operate profitably in the future?

MLPs are equities operating in a niche space with a steep understanding curve, which can cause volatility. The global economy is more connected than it has ever been so every asset class is more correlated than it has ever been. When and if a broader market correction comes or if commodity prices again fall, market sentiment is going to carry MLPs down with it, though maybe not as far given how far they have already fallen. The risks of investing in MLPs remain.

If you believe that (1) US energy demand will remain relatively constant in the next few years, and (2) renewable energy will not overtake natural gas and petroleum usage in the US, and (3) that the long-term contracts MLPs have signed will remain in place and continue to generate cash flow for transportation, storage, and processing of hydrocarbons, well, it logically follows that the value proposition of being invested in MLPs is relatively unchanged from one or three or five years ago. If you’re invested in MLPs now, you’re here because you have faith in the thesis, you recognize the risks and volatility, and you like that 4%-8% yield you’re paid while you wait for the midstream world to make sense again.

{kind=link}