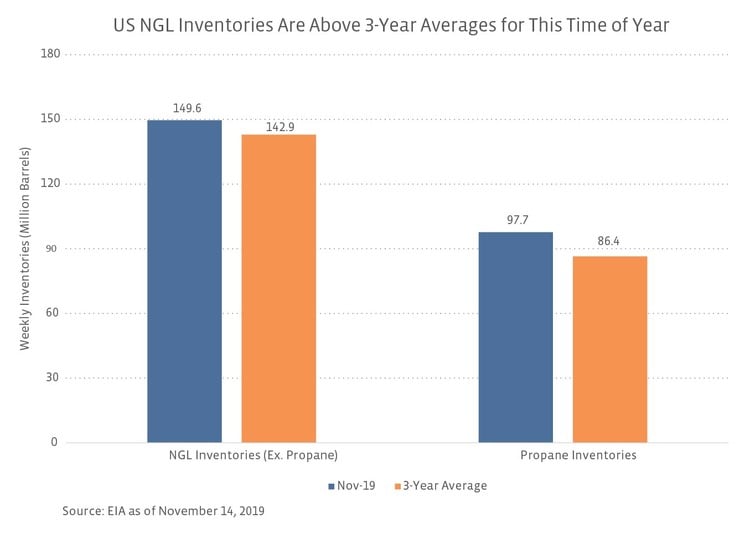

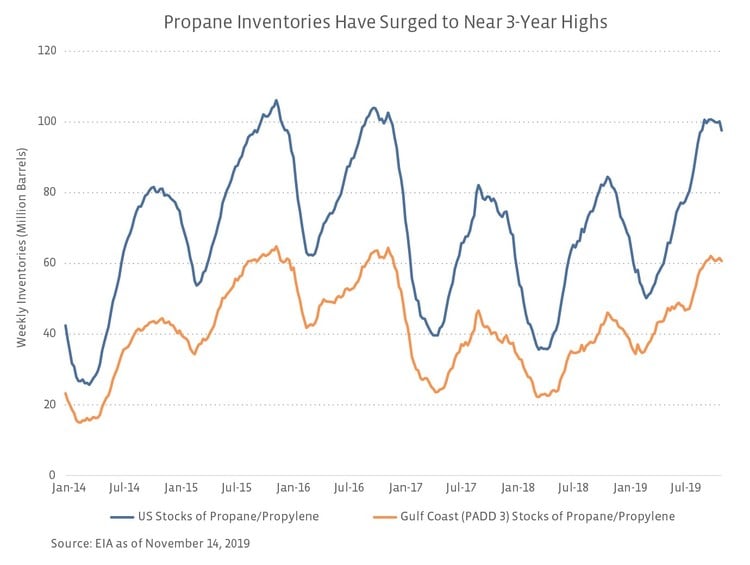

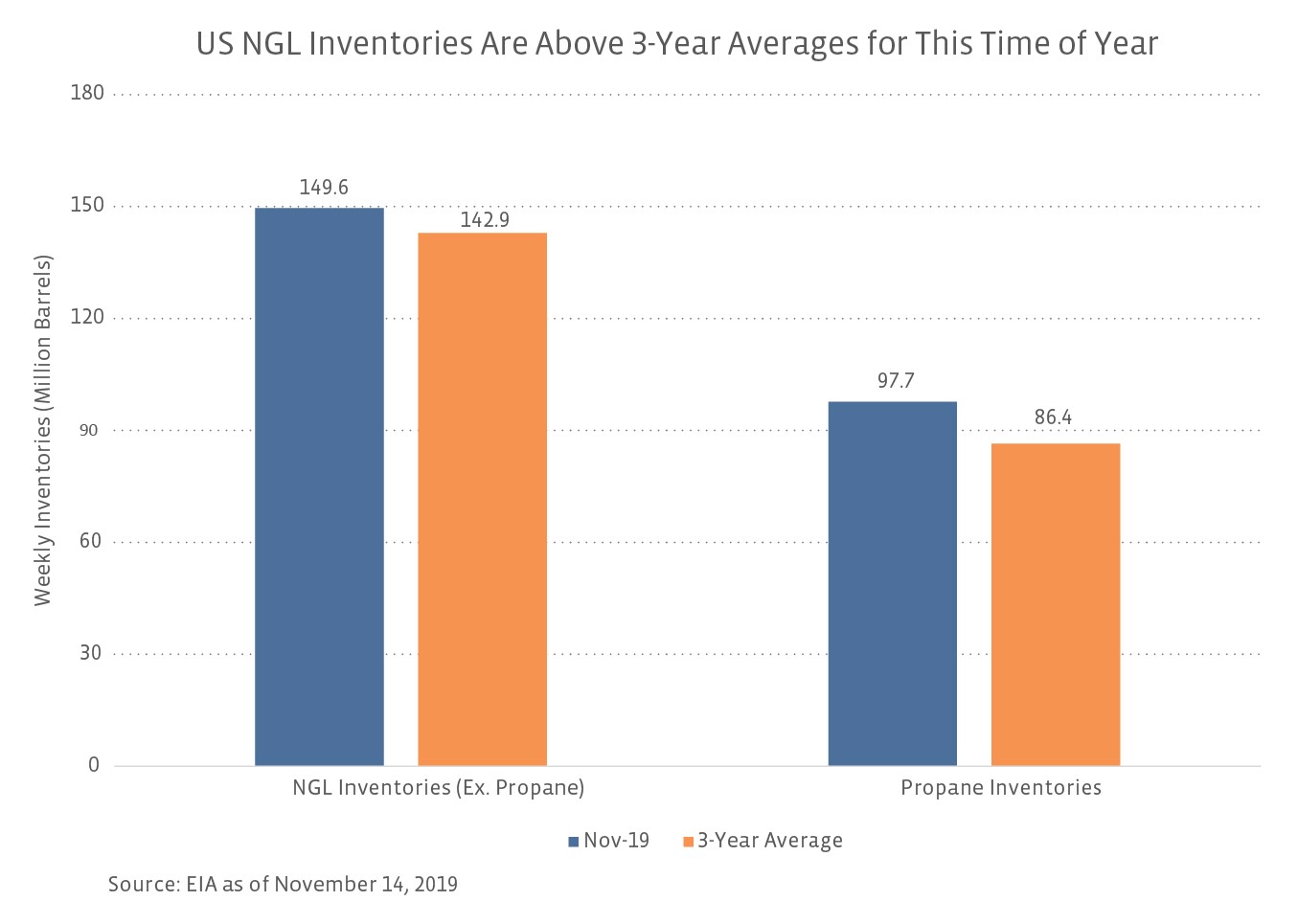

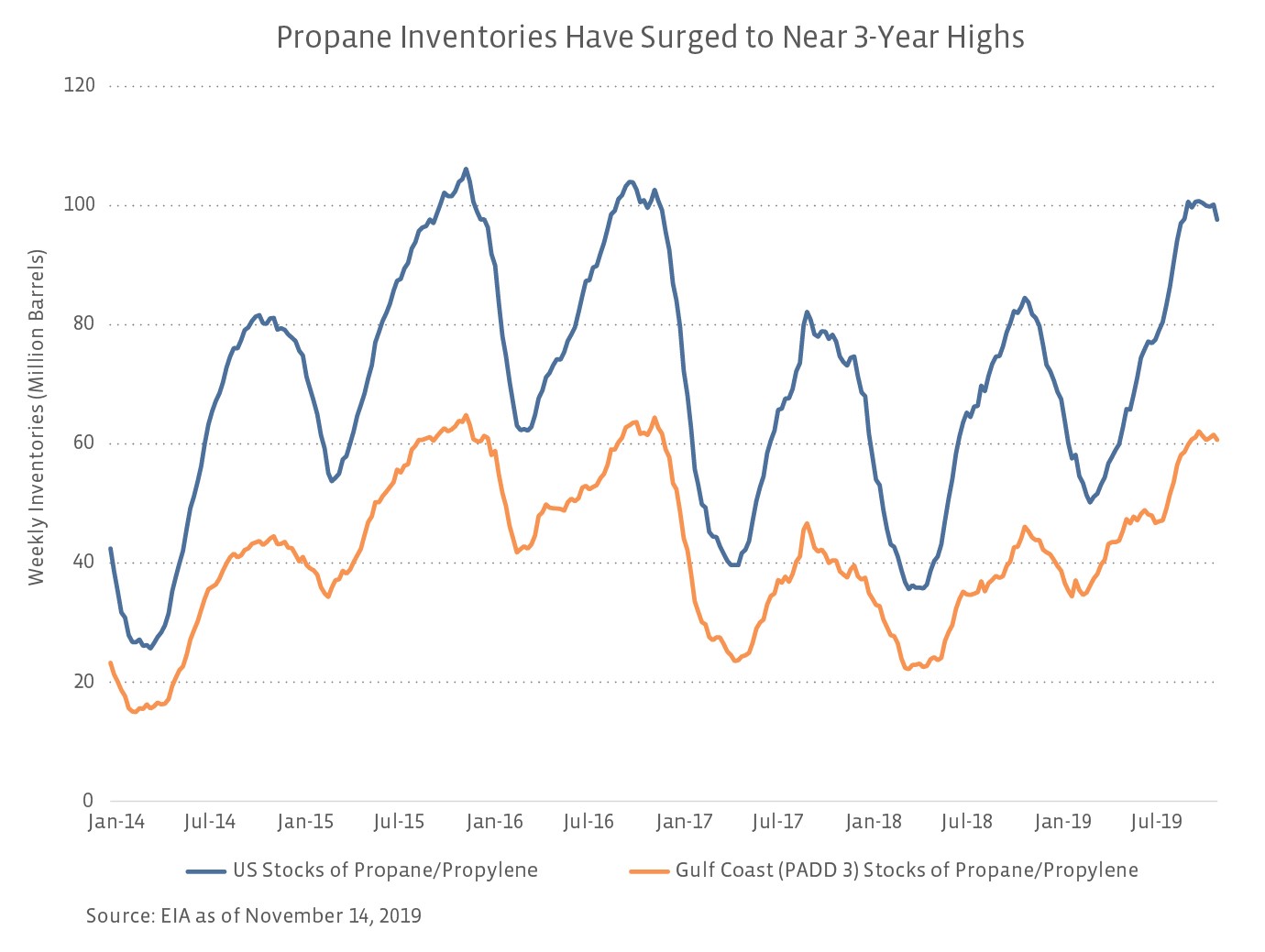

Mont Belvieu NGL prices have also been negatively impacted lately by high inventory levels at the hub for purity products and in the US in general, where inventories are above the three- and five-year averages. The price of propane at Mont Belvieu increased nearly 8% month-over-month as of November 8 but is down 31.9% over the same time last year. The short-term price increase is likely due to propane’s seasonal demand for uses as a space heating fuel and in crop drying. Elevated propane inventories on the Gulf Coast are likely to temper any further price jumps in the short term and have kept prices down compared to last year’s heating season. Propane inventories hovered near three-year highs for both the US and Gulf Coast (PADD 3) for the week ending November 8 (see chart below). High inventories reflect the continued growth in NGL production alongside crude in areas like the Permian, while additional pipelines, fractionation capacity, and export infrastructure have facilitated the movement of NGLs to the Gulf Coast. The chart below depicts current US NGL inventories as of November 14 and inventories for the same time period on a three-year average basis to account for seasonality.

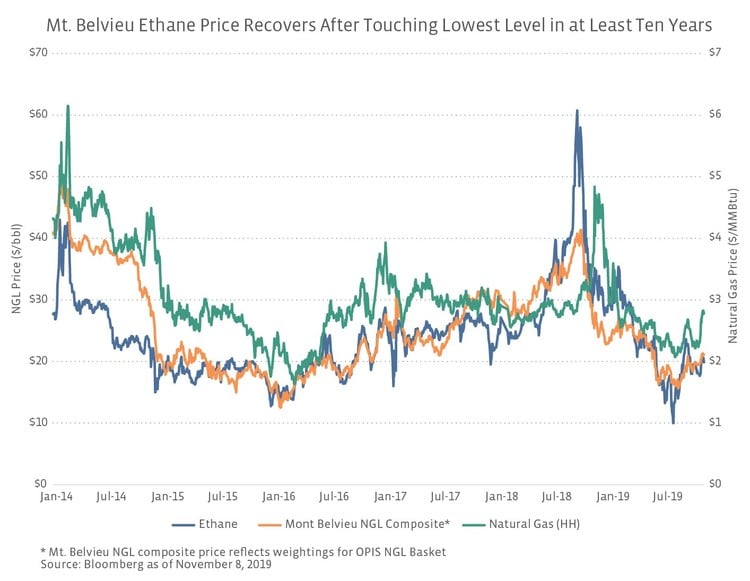

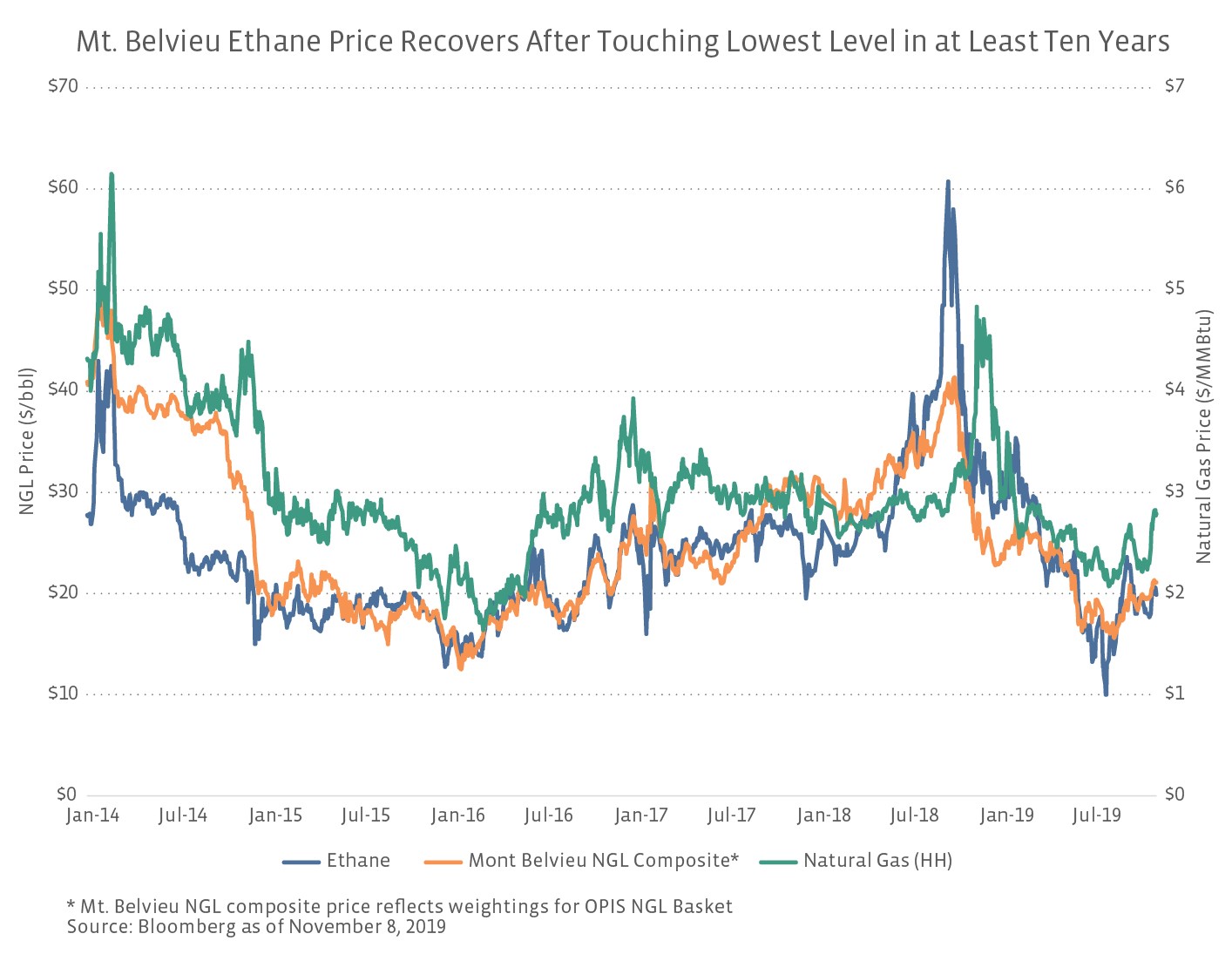

Mont Belvieu ethane price comes off three-year low as crackers start up.

Ethane has been in focus lately as the Mont Belvieu price hit a multi-year low in late July but has recovered somewhat with new cracker capacity beginning to come online along the Gulf Coast. Unlike other NGLs, ethane can be left in the natural gas stream in a situation known as ethane rejection. Ethane prices generally track near natural gas prices with some variation possible as a result of international market dynamics from increasing export levels. In our last piece on NGLs, we noted the price of ethane spiked in 3Q18 to its highest level since 2012 as a result of fractionation constraints at Mont Belvieu. Today, ethane is trading slightly above its three-year low at 20 cents per gallon (cpg) and briefly hit 10 cpg at the end of July, which represents the lowest ethane price at Mont Belvieu in at least ten years. Incremental demand for ethane primarily stems from demand growth at petrochemical plants, which have been somewhat in flux recently. Sasol’s (SSL) Lake Charles Ethane Cracker, which has a 1.54 million ton per year nameplate capacity, reached beneficial operation at the end of August but was running at only 50% of capacity. Sasol has indicated it is closer to full completion of the project, which has been delayed due to technical challenges. A fire at ExxonMobil’s (XOM) Baytown Olefins Plant in July resulted in an unscheduled outage and the plant running at reduced rates. Lotte Chemical and Westlake Chemical (WLK) held a grand opening ceremony for their Lake Charles ethylene facility in May, but detailed updates on operations have been limited since then. Finally, Formosa Plastics expected to achieve commercial operations at its polyethylene plants by the end of this year. Ethane inventories peaked in June before declining by 8.2% through August, which is potentially the result of a slow ramping in ethane consumption by these plants.

What’s driving demand for domestically produced NGLs?

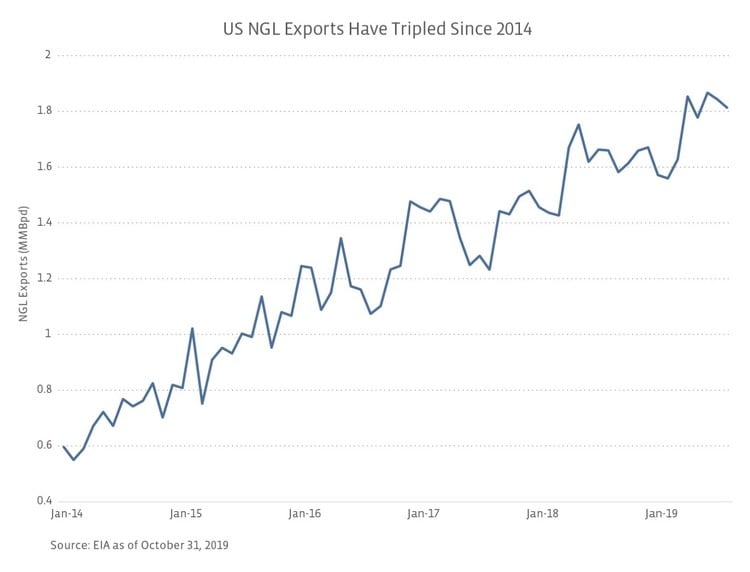

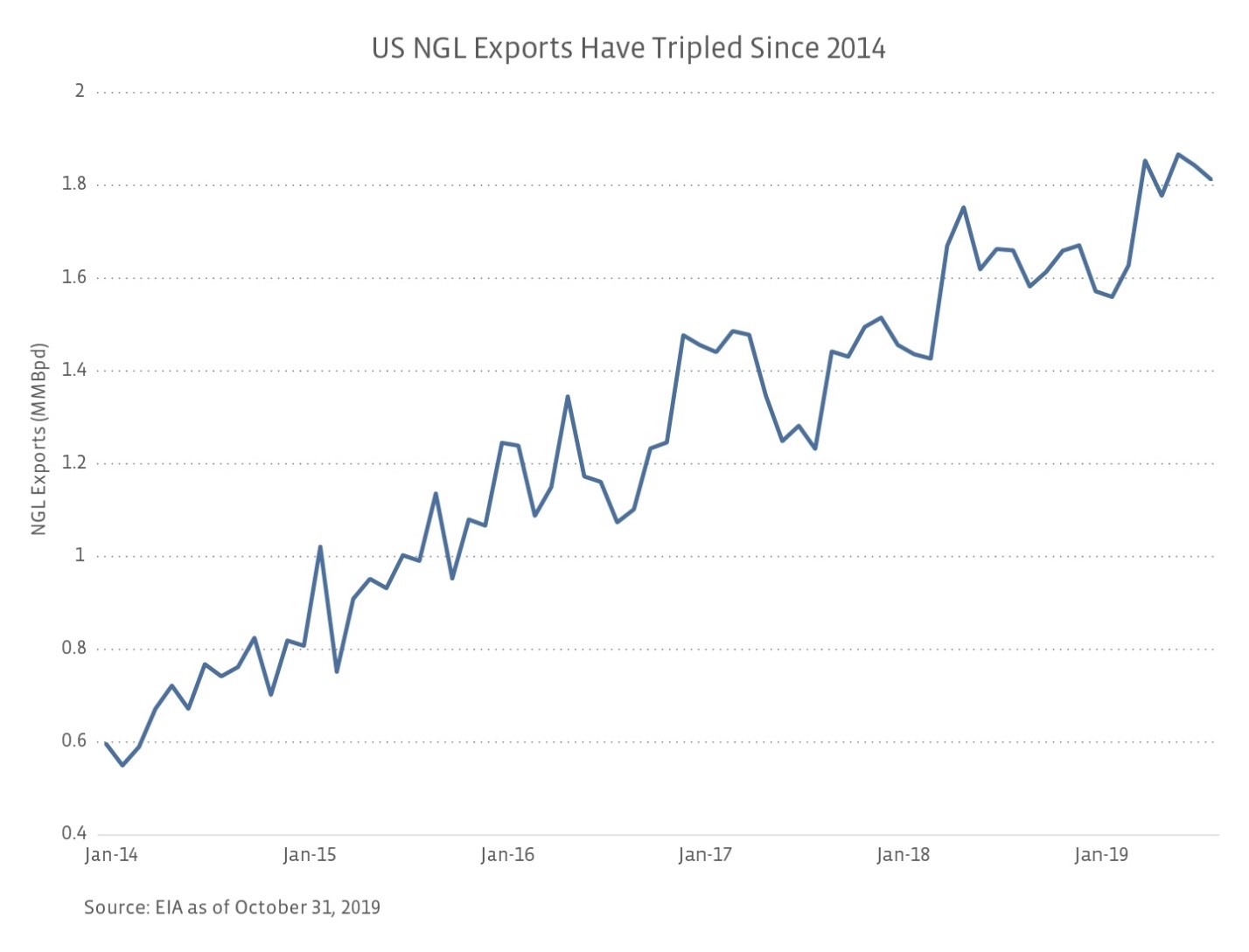

The US is currently the fastest growing exporter of crude and NGLs globally and has been a net exporter of NGLs since 2014. Aside from ethane cracker additions discussed above, domestic demand growth for NGLs is expected to remain relatively flat, meaning the incremental barrel of US NGL production will likely need to be exported. Since the beginning of 2014, NGL exports have tripled to exceed 1.8 MMBpd. At its recent investor day, Phillips 66 (PSX) said it expected LPG exports to increase by 50% between now and 2024. Global NGL consumption will be driven by economies with emerging middle classes in Asia, Latin America, and Africa, among others. These regions will require more NGLs for use in petrochemical plants, industry, heating, and other commercial processes.

Several midstream companies are developing projects to expand export capacity along the Gulf Coast. In July, EPD announced an expansion project to increase LPG loading capacity in the Houston area by an additional 260 MBpd. When combined with a recently completed 175-MBpd expansion, Enterprise will have expanded its LPG export capacity in Houston to more than 1 MMBpd. EPD is also leveraging its NGL value chain by constructing a second propane dehydrogenation (PDH) plant that will consume up to 35 MBpd of propane when it is completed in 1H23. TRGP is expanding its export capacity in the Houston area at its Galena Park Marine Terminal by up to 67% to 11-15 million barrels per month by 3Q20. Up north, Pembina Pipeline (PPL CN) is investing $250 MM to construct the 25-MBpd Prince Rupert LPG export terminal in British Columbia, which is expected to be completed in mid-2020. Pembina is also developing a new $2.5 billion PDH plant, which is an opportunity to diversify its revenue stream and integrate its petrochemicals and NGLs businesses in Western Canada. As with crude and natural gas, NGL exports continue to represent a significant growth opportunity to connect production with growing demand abroad.

Bottom Line

Despite elevated inventories, delayed cracker additions, and steady export levels, Mont Belvieu NGL prices have increased off their late-summer lows, with seasonal demand likely helping. While a number of NGL-focused pipelines have recently come online or are nearing completion, NGLs will remain a growth area for midstream companies that extends beyond pipelines. New and expanded infrastructure will facilitate NGL production growth and increasingly move these hydrocarbons abroad.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}