How and why the US is expected to dominate oil production growth

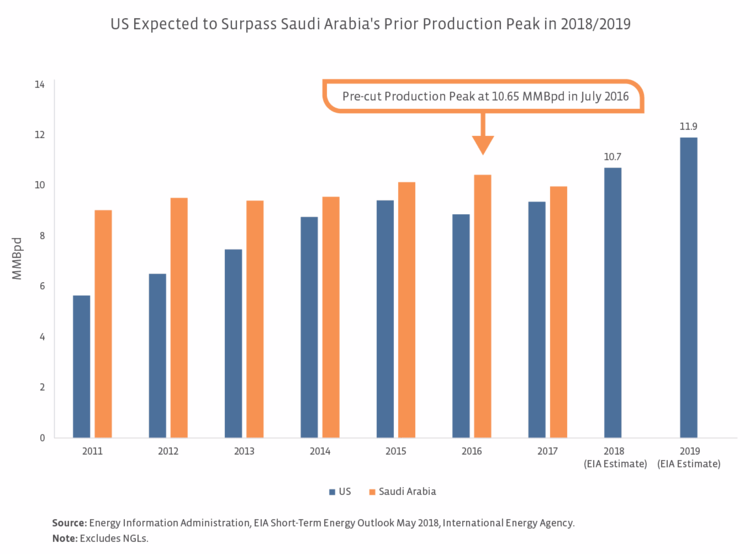

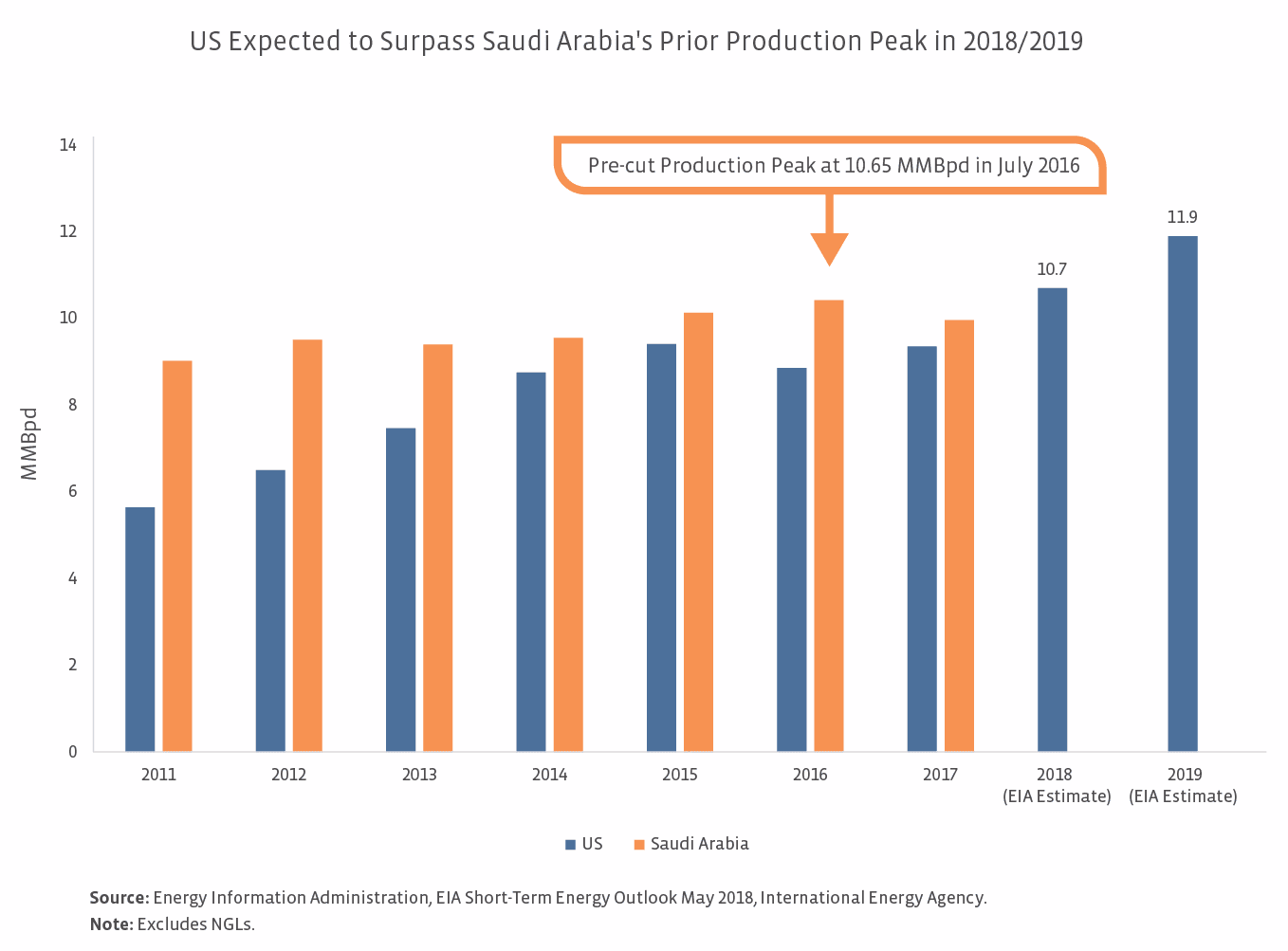

The International Energy Agency (IEA) forecasts that the US will represent greater than half of the global growth in oil production capacity over the next five years. Total liquids production, which includes oil and natural gas liquids (NGLs), is expected to reach approximately 17 million barrels per day (MMBpd). This expected production growth would firmly place the US in the top spot for oil production. When it comes to producing oil, the US enjoys a competitive advantage under the ground in terms of the resources in place (good geology) and above the ground in terms of technology, human capital, infrastructure, etc. that make production possible at a competitive cost (see our rig count post for more on productivity). The US can quickly bring production to market, as exemplified by the nearly 1.2 MMBpd of oil production growth, or 13.6% increase, from January 2017 to December 2017.

These advantages partially explain why the US is expected to dominate global crude production, but the other part is explained by what’s been going on in the rest of the world. From 2014 to 2016, global upstream oil and gas investment nosedived by 44% and was stagnant in 2017. (Investment in US shale was up 53% in 2017 compared to 2016.) You don’t need a degree in petroleum engineering to appreciate that offshore deep-water wells, for example, are much more complex, time-consuming, and expensive than drilling a well in the Permian, not to mention the greater risk. Deep-water wells are just one example of long-lead oil projects that became less attractive in a $50 oil price environment. In the IEA’s five-year projection, OPEC production capacity is expected to expand by less than 1 MMBpd on a net basis, while expected growth in the US is estimated at 3.7 MMBpd.

The US is similarly dominant when it comes to natural gas production (see our recent post). Because of the speed with which US production can react and the sheer volume of oil and gas production, the US is really becoming a major hydrocarbon producer for the world. We use hydrocarbon to encompass crude, refined products, liquified natural gas (LNG), as well as NGLs like ethane, propane, and butane.

Why exports?

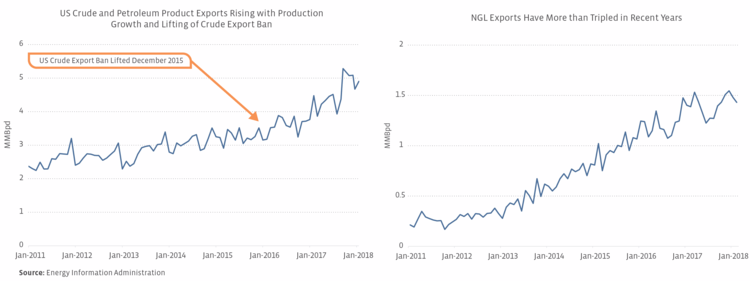

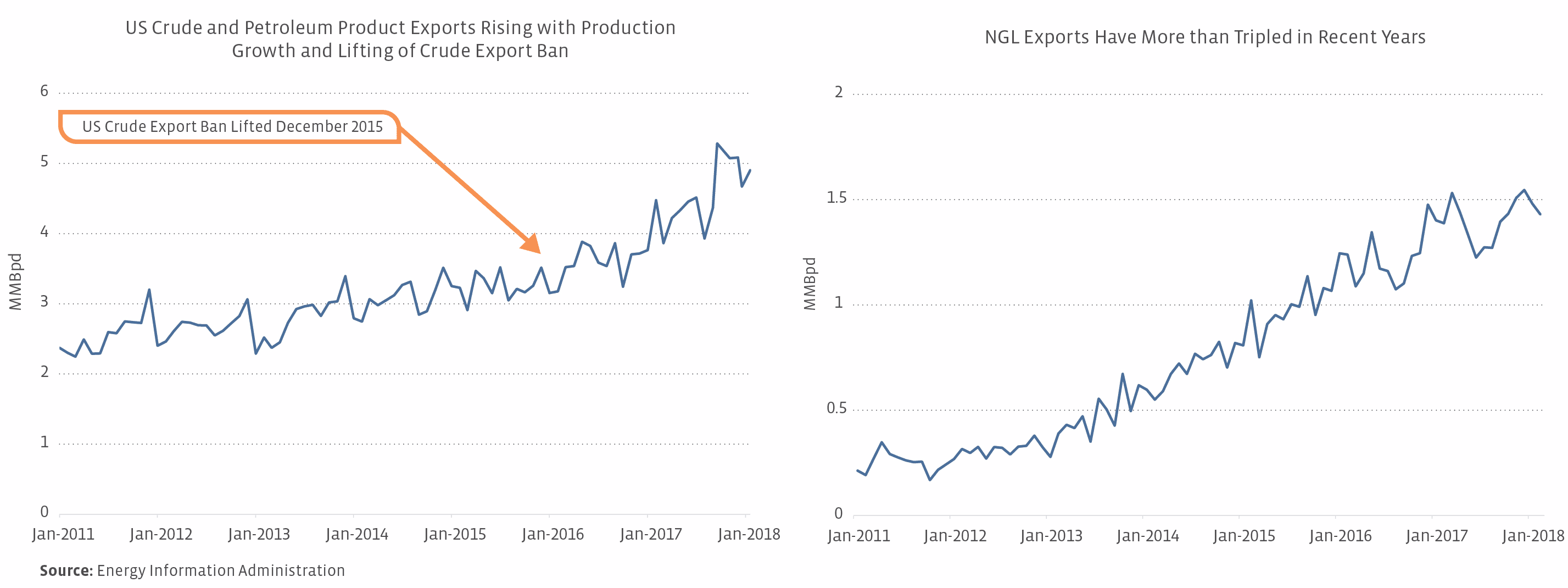

Petroleum demand in the US averaged 19.9 MMBpd in 2017, so it would seem that the projected production of 17 MMBpd could all be used domestically. In reality, it’s not that simple. US Gulf Coast refiners are geared to run significant volumes of heavy crude, which they will continue to import from Canada, Latin America or the Middle East even as US light oil production grows. The East Coast, which is short on refining capacity, imports refined products from overseas to supplement volumes supplied by Gulf Coast refiners. This just scratches the surface, but suffice it to say, US supply does not perfectly match US demand, opening the door for exports. In its base case, the EIA forecasts that the US will become a net energy exporter in 2022, but it could happen by 2020 in an environment of higher oil prices.

Exports also provide access to the fastest-growing demand centers globally. According to the IEA, India is expected to represent the largest growth driver for global primary energy demand to 2040 – accounting for approximately 30%. More broadly, developing countries in Asia (including India) are expected to drive two-thirds of global energy demand growth, with the balance predominately coming from the Middle East and Africa. It isn’t that much of a stretch to say that an investment in US energy infrastructure and MLPs is a derivative play on growing energy demand in Asia.

Exports require infrastructure

At the risk of stating the obvious, infrastructure is vital to facilitating exports. MLPs and EI companies can support exports in a few ways: 1) processing hydrocarbons into usable form (refining, gas processing for shipment in pipelines, fractionating natural gas liquids, liquefaction of natural gas) 2) transporting the hydrocarbons to the coast, and 3) storing hydrocarbons and loading tankers at marine terminals. There have been several export-driven MLP project announcements already this year, including pipelines and terminals.

Buckeye (BPL) is constructing a new deep-water marine terminal in Ingleside, Texas, with Phillips 66 Partners (PSXP) and Andeavor (ANDV) to support crude exports. The South Texas Gateway Terminal will be supplied by the new Gray Oak Pipeline from the Permian, being built by PSXP and expected in-service by the end of 2019.

Energy Transfer Partners (ETP) is building a new ethane export facility that will supply Satellite Petrochemical’s ethane crackers, with the export terminal expected to be in-service in 4Q2020.

Enterprise Products Partners (EPD) recently purchased additional property to expand its Enterprise Hydrocarbon Terminal to allow for more exports.- EPD is also building an ethylene export facility with Navigator Holdings (NVGS) that will be capable of exporting 1 million tons of ethylene per year, with start-up anticipated by 1Q2020.

- PSXP is building a new pipeline to a marine terminal to support increased refined product exports from the Lake Charles Refinery.

These are just a few examples of export projects announced this year for crude, refined products, and NGLs. Several projects to export LNG are also under way. We will likely see additional crude export projects in the future as light crude production overwhelms US refiners’ appetite for light crude.

Bottom line

The US has become a dominant player in the global energy market and expected production growth will result in US hydrocarbons increasingly being shipped overseas. Rising exports will require new infrastructure, creating growth opportunities for MLPs and EI companies.

{kind=link}

{kind=link}