Source: Energy Information Administration

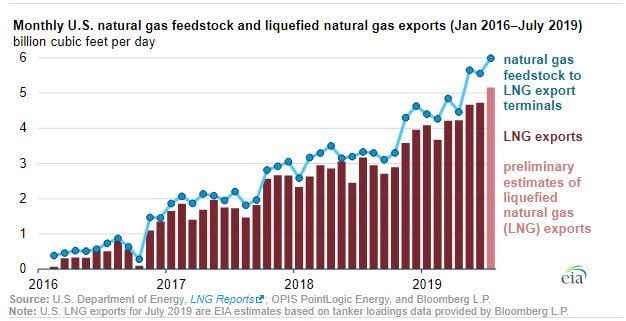

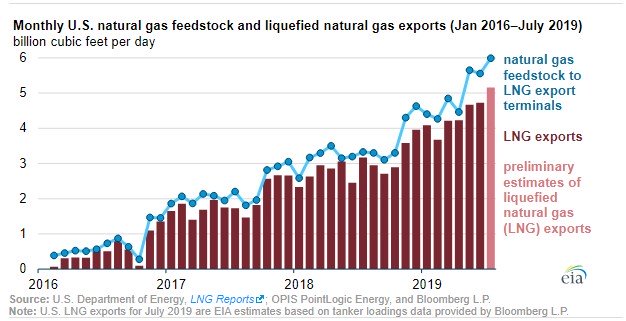

US export growth has remained robust despite pricing and other headwinds, such as the ongoing trade war between the US and China. China raised its tariff on imports of US LNG from 10% to 25% in May, and unsurprisingly, the EIA reported that US LNG exports to China remained at zero for June. While China’s retaliation is impactful for exporters, the Department of Energy’s (DOE) LNG Monthly shows that US exporters have been able to deliver LNG to other countries. The top five destinations – South Korea, Chile, Mexico, Japan, and Spain – represented nearly 60% of total US LNG exports in June. Despite the relative flexibility of US exports, the stagnation in trade talks over the last few months adds uncertainty for US LNG exporters who are approaching a final investment decision (FID) on projects. Specifically, the trade war makes it more difficult for LNG exporters to acquire long-term purchase agreements with Chinese buyers, who represent one of the largest importers of LNG globally. While progress in trade negotiations has been slow, the Trump Administration is expected to renew official talks with Chinese Vice Premier Liu He in October, and any progress toward reducing tariffs would be welcome news for LNG companies.

LNG exporters weather short-term price weakness with eyes on long-term thesis.

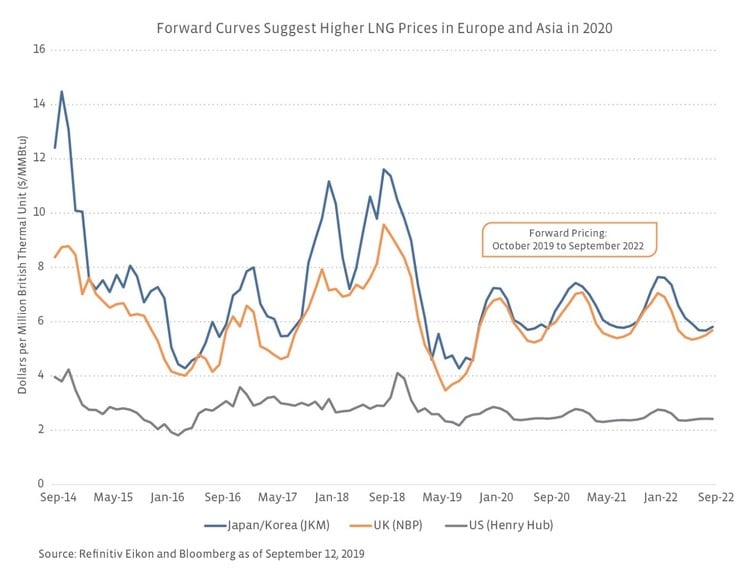

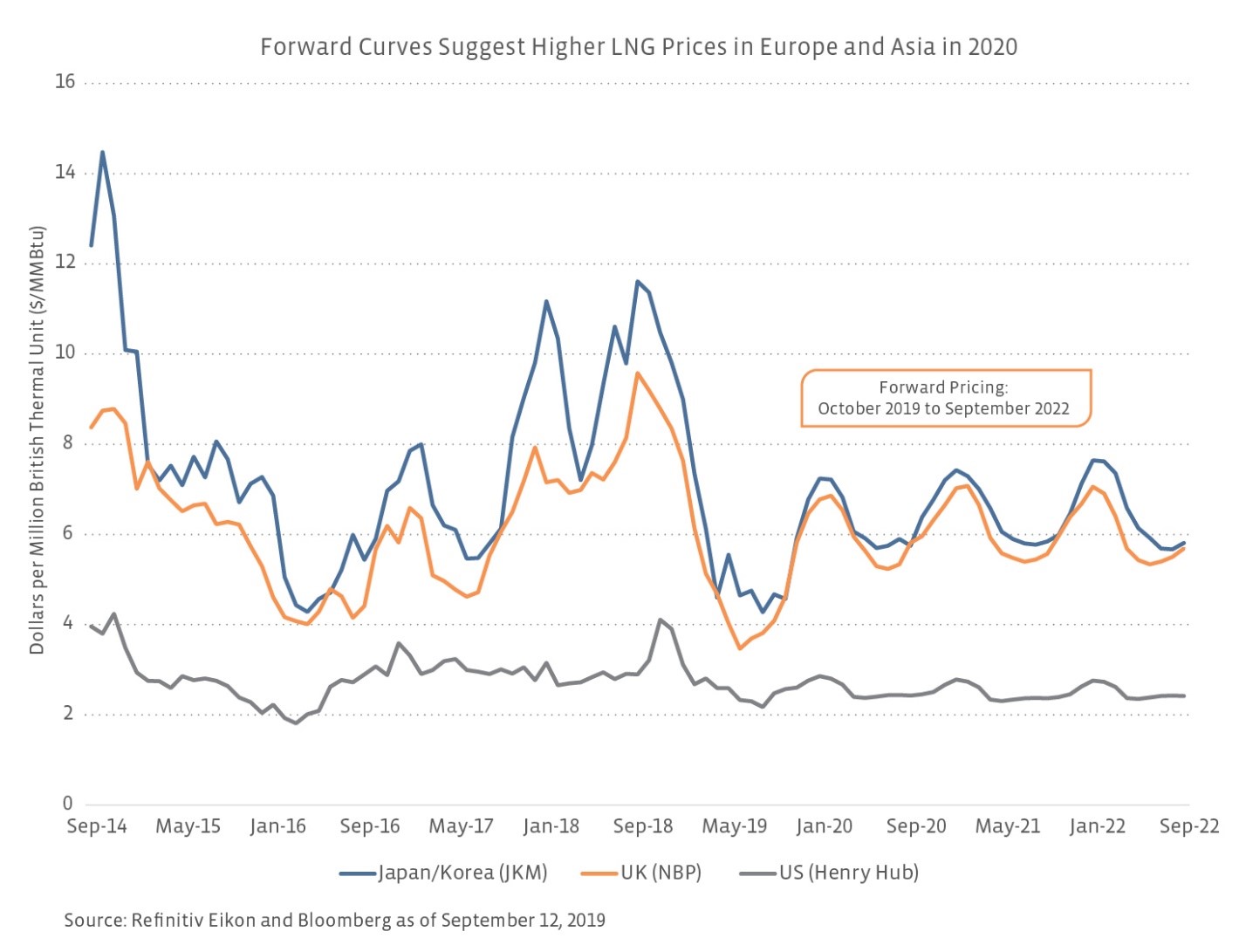

Lower short-term prices have placed pressure on LNG exporters recently. The price of LNG in Asia, as measured by the Japan/Korea Marker (JKM), and in the UK, as measured by the National Balancing Point (NBP), fell nearly 60% year-over-year as of September 1, just above August’s multi-year lows (see chart below). On its 2Q19 earnings call, Cheniere Energy’s (LNG) Chief Commercial Officer Anatol Feygin cited multiple factors for the global price weakness, including significant supply growth worldwide, warm weather in Europe and Asia, and high inventory levels in Europe as a result of storage injections and strong import levels. Both Cheniere and Tellurian (TELL) have expressed some optimism that prices will rebound off their current low levels, with TELL CEO Meg Gentle saying in a recent presentation that they expect prices to reach an inflection point in the coming months depending on weather conditions. As you can see in the chart below, forward LNG prices for Europe and Asia are in relatively strong contango in late 2019 and early 2020, meaning prices are expected to rise.

Despite depressed prices recently, Cheniere reconfirmed full-year 2019 adjusted EBITDA guidance of $2.9 to $3.2 billion as a result of operational and construction execution to date this year. The impacts of weaker spot prices are mitigated for companies like Cheniere that boast a large amount of volumes committed to long-term agreements (about 75% of Cheniere’s volumes are currently contracted in long-term sales and purchase agreements). Producer-backed agreements, such as Cheniere’s agreement announced this week with EOG Resources (EOG), provide another means of securing commitments in a weak price tape. While companies like Tellurian and NextDecade (NEXT) may face more uncertainty over current macro headwinds as they develop their respective export terminals, both companies have also been able to secure commitments and make progress toward a FID in recent months. In July, for instance, Total reached agreements with TELL to invest $500 million in Driftwood LNG and purchase one million tons per annum (MTpa) of LNG. Looking forward, LNG companies continue to project that LNG demand will outpace supply. NEXT estimates that global demand will exceed available supply by as much as 150 MTpa by 2025, with North American projects possibly filling two-thirds of this shortfall. TELL similarly projects $150 to $225 billion in total investment required to build out the LNG and supporting infrastructure to export the estimated 100-150 MTpa surplus supply in the same timeframe.

One project completion and two FIDs this summer, while others get closer.

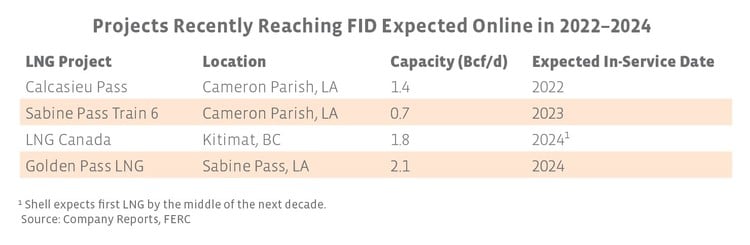

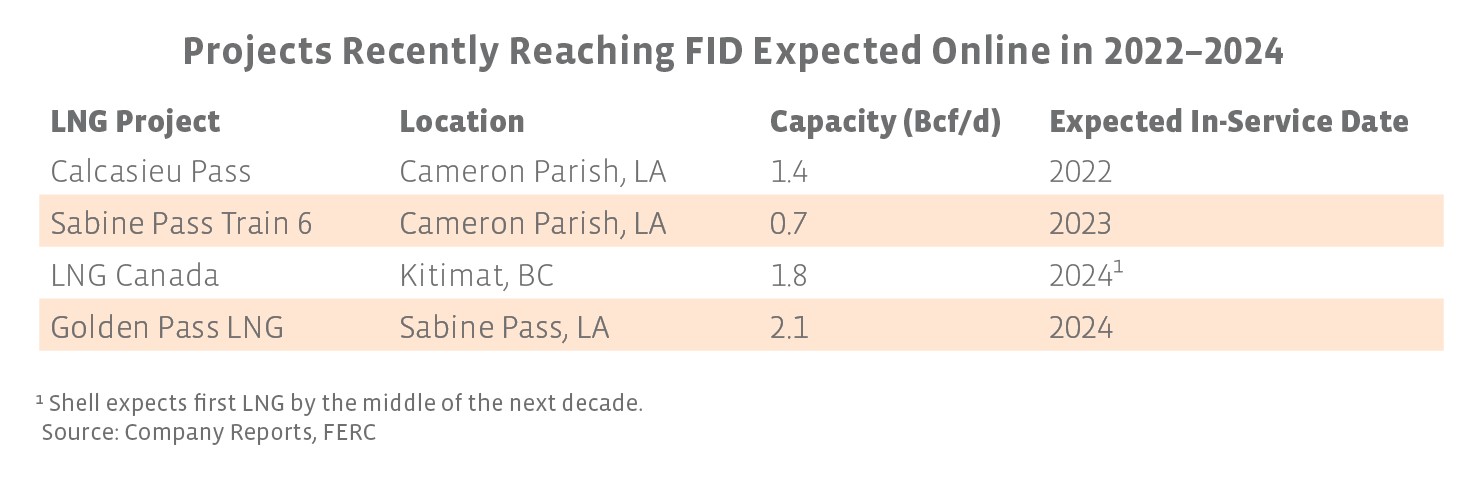

Since our last update on LNG projects, there have been a number of notable announcements that have moved projects forward. In August, Venture Global’s Calcasieu Pass LNG project reached a positive FID, joining LNG Canada and Golden Pass LNG this year (see table below). Calcasieu Pass will have a capacity of 1.4 Bcf/d and is expected in service in 2022. In a recent press release, TELL’s Meg Gentle noted that the company expects to reach FID on its Driftwood LNG project in 2019. In June, Cheniere announced a positive FID for Sabine Pass Train 6, which is expected to enter service in 2023. More recently, Cheniere reported that it had reached substantial completion on Train 2 at its Corpus Christi liquefaction facility. In regulatory news, FERC recently approved Driftwood LNG, Sempra Energy’s (SRE) Port Arthur LNG, and Freeport LNG’s Train 4 expansion, while the DOE announced approval for Kinder Morgan’s (KMI) Gulf LNG. In a busy few months, FERC also released positive final environmental impact statements for Gulf LNG, NEXT’s Rio Grande LNG, Venture Global’s Plaquemines LNG, and Annova LNG’s Brownsville project.

A few projects in various stages of development have hit some snags. Despite facing significant delays due to hurricane-related delays, regulatory issues, and construction delays, Freeport LNG and KMI’s Elba Island LNG project are expected to reach commercial service by the end of 2019. In early September, Texas-based Freeport LNG announced it had shipped its first commissioning cargo for train 1 after an approximately nine month delay, with commercial operations expected to start in late September. Freeport LNG also anticipates reaching FID within the next several months on its expansion to a fourth train and has already received regulatory approvals. After initially being delayed by mechanical issues in the liquefaction units that moved the startup date from 4Q18 to May 2019, KMI was forced to delay its Elba Island LNG project located near Savannah, Georgia, as a result of a heating issue and Hurricane Dorian. Per recent updates and KMI’s 2Q earnings call, construction has resumed, and the first train is expected to be in service soon.

Bottom Line

While the ongoing US-China trade war and price weakness have created noise for the LNG space, the long-term need for LNG remains evident. Going forward, natural gas consumption is projected to increase for both power generation and industrial uses, and the US is expected to be among the leaders for gas production growth through 2025, with much of that incremental growth likely to be exported. LNG export growth continues to create a need for both export and supporting infrastructure to facilitate the movement of gas to the coast.

{kind=link}

{kind=link}

{kind=link}