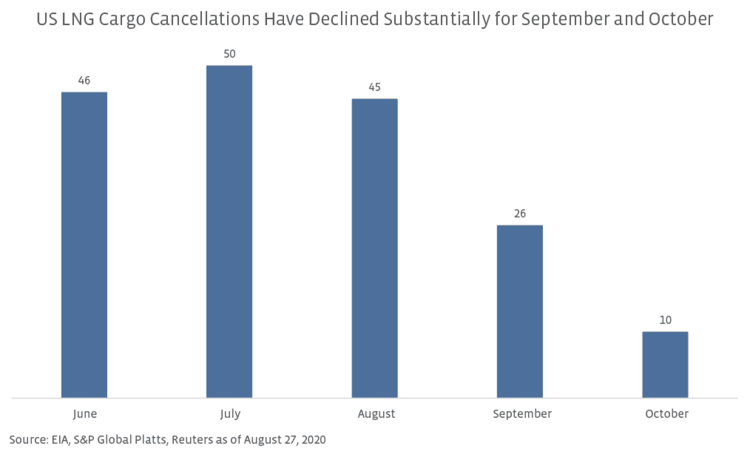

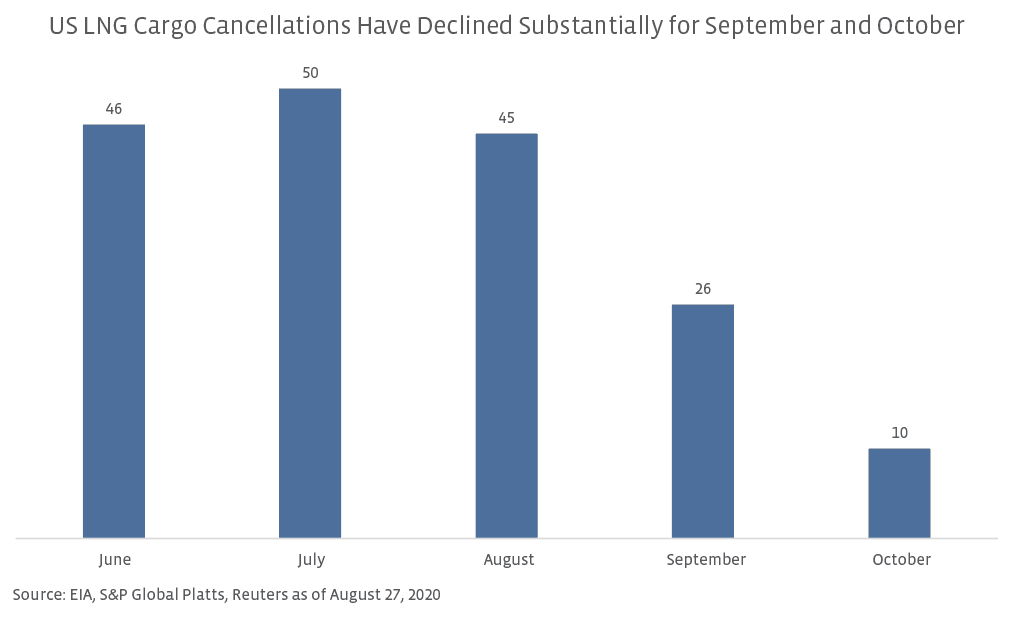

US LNG cargo cancellations beginning to ease.

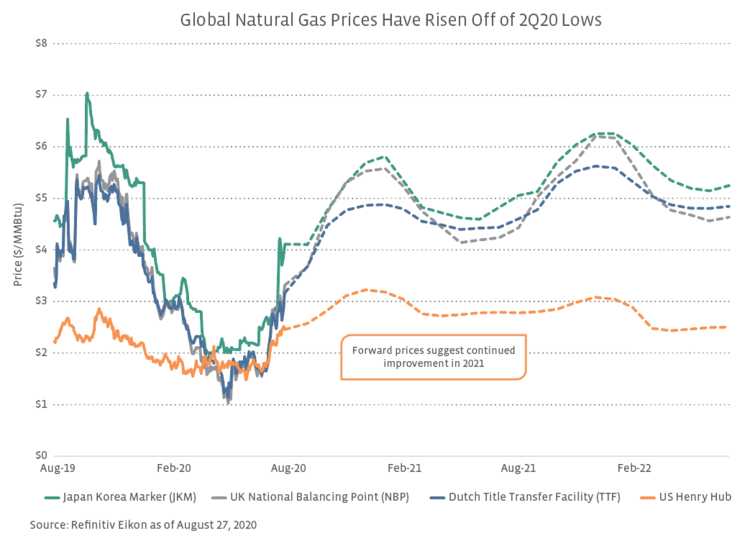

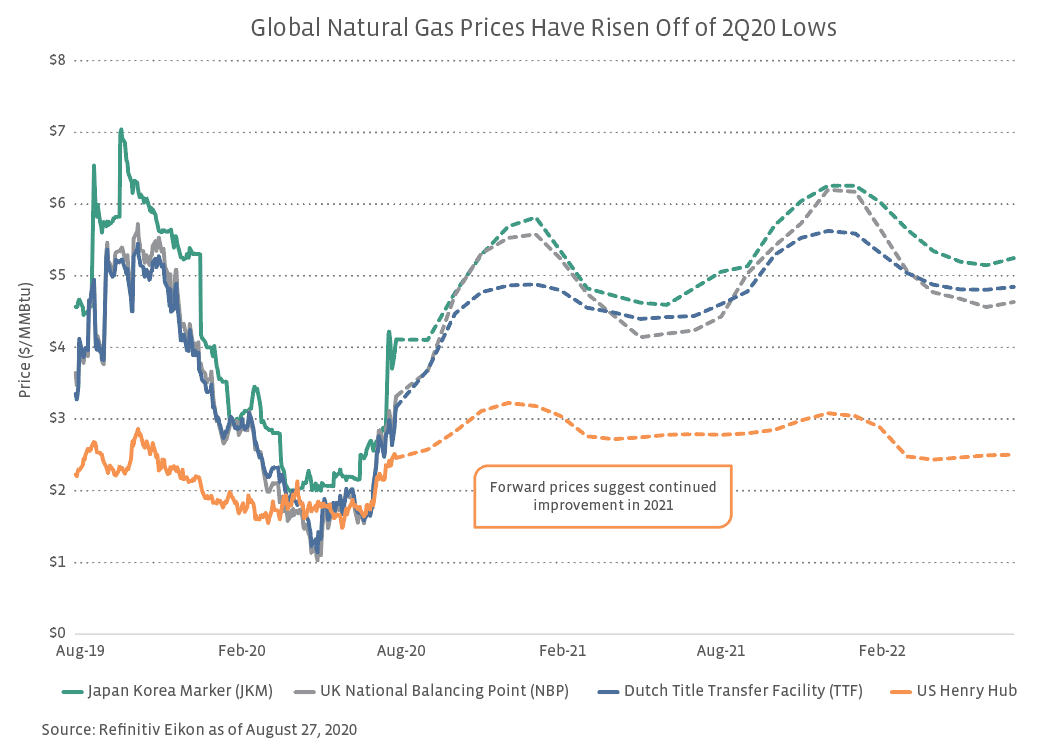

Recent price improvements and the modest widening in differentials between US and foreign LNG prices are welcome developments for US exporters, who have seen customers opt to cancel dozens of cargoes over recent months due to uneconomic conditions. For cargoes scheduled for loading from June through August, 141 US cargoes are estimated to have been canceled (see chart below). Notably, however, cargo cancellations are expected to be much lower at an estimated 26 cargoes for September and only 10 for October as demand has begun to recover. Cheniere Chief Financial Officer Zach Davis said the company expected continued improvement in market conditions and did not expect cancellations of contracted volumes this winter, further supporting the idea that the worst of the cargo cancellations are over.

Cheniere reported about 50 cargo cancellations for 2Q20, with the company reminding investors on its earnings call of its contract optionality that allows customers to suspend or cancel cargoes with adequate notice. The company exported 78 cargoes of LNG in 2Q20 compared to 128 cargoes in 1Q20 and 104 in 2Q19. Cargo cancellations resulted in a noisy quarter for Cheniere in terms of earnings, with 2Q20 adjusted EBITDA coming in more than 50% above the Bloomberg consensus estimate. Customers who cancel cargoes pay Cheniere a fixed liquefaction fee, and revenue associated with the cargoes is recognized upon receipt of the cancellation notice. Alongside 2Q20 results, Cheniere reconfirmed its full-year adjusted EBITDA guidance of $4.2 billion at the midpoint and distributable cash flow guidance of $1.15 billion at the midpoint. Separately, Cheniere Energy Partners (CQP) was one of the few MLPs to raise its distribution sequentially for 2Q20, increasing it by 0.8%. In late August, Brookfield Asset Management agreed to buy Blackstone’s approximately 40% interest in CQP for $34.25 per unit in an approximately $7 billion transaction. Sabine Pass LNG, the largest LNG terminal in the US, is operated by a subsidiary of CQP.

Hurricane Laura’s impact is likely temporary for US LNG.

Hurricane Laura is expected to have a short-term impact on the US LNG market after making landfall as a powerful but fast-moving Category 4 hurricane on August 27. The storm impacted East Texas and Southwest Louisiana, where several LNG facilities are operating or in development. In terms of operating facilities, Cheniere’s Sabine Pass and Sempra Energy’s (SRE) Cameron LNG shut down and evacuated most employees on site in preparation for the storm. Cameron had only recently begun full operations upon completion of train 3. With these two large facilities temporarily down, an estimate of US LNG exports by Refinitiv for August 27 showed a decline to 2.7 Bcf/d, the lowest level since February 2019. The outages, while likely temporary, are contributing to a tighter global LNG market by keeping supply in check. On Monday, Cheniere reported no significant damage to Sabine Pass and said it had begun the process to restart the facility. SRE also disclosed on Monday that Cameron LNG and Port Arthur LNG, which is currently under development, had minimal flooding and no catastrophic wind damage. Cameron operations are expected to fully resume as soon as safely possible. Restarting LNG facilities can take time. After Hurricane Barry made landfall in Louisiana in 2019, some liquefaction capacity returned in days, but it took more than two weeks to fully restore LNG production. Cheniere has some flexibility to offset impacts at Sabine Pass by loading cargoes at its Corpus Christi LNG facility, with natural gas delivered to Corpus Christi appearing to ramp week-over-week as of August 27.

Turning to projects under development, privately owned Venture Global LNG, which is constructing the Calcasieu Pass LNG facility in Cameron, Louisiana, reported minimal damage. Similar statements were released by ExxonMobil (XOM) and Qatar Petroleum’s Golden Pass LNG and Energy Transfer’s (ET) Lake Charles LNG.

Mixed US and global project news recently could have implications for the coming years.

Recent updates for US LNG projects have been mixed, with positive progress for some and delays of final investment decisions (FID) for others. In addition to Cameron reaching full commercial operations in August, Kinder Morgan (KMI) placed the final units in service for its 0.35-Bcf/d Elba Island LNG facility in Georgia during the month. Notably, Elba is expected to export its first cargo since January this week. In conjunction with 2Q20 earnings, Cheniere moved up the expected date of substantial completion for Sabine Pass train 6 from 1H23 to 2H22 and reaffirmed the 1H21 completion date for Corpus Christi train 3. The Department of Energy announced it had approved exports from Pembina Pipeline’s (PPL CN) proposed Jordan Cove LNG terminal in Oregon. The 1.08-Bcf/d export facility would be the first on the US West Coast, and Pembina has continued to work on gaining state regulatory approvals and finding a partner for the project, though the timing for an FID remains uncertain.

In 2Q20, several companies announced they would delay the FID on projects under development because of the challenging market and sought to improve financial flexibility (read more). in addition to seeking cheap sources of natural gas for Driftwood LNG and reevaluating the project’s scope, Tellurian (TELL) plans to reduce total Driftwood project costs by an estimated 30% by deferring the related 4.0-Bcf/d Permian Global Access Pipeline, 2.0-Bcf/d Haynesville Global Access Pipeline, and 2.0-Bcf/d Delhi Connector Pipeline. In July, NextDecade (NEXT) said it would construct only five of the six planned trains for its Rio Grande LNG project but noted the facility would be able to produce the same total LNG volumes as originally planned.

Delays have not been isolated to US exporters. In April, Qatar Petroleum delayed the expected start-up of the first phase of its North Field LNG Expansion to 2025. Similarly, Australia’s Woodside Petroleum (WPL AU) deferred the targeted FID for Scarborough and Pluto Train 2 from 2020 to 2H21 as a result of demand uncertainty. ExxonMobil also further moved back the FID for Rovuma LNG in Mozambique to 2021. The delay of several projects globally could create opportunities for companies with existing capacity and those who can get their projects over the finish line if there is a mismatch between supply and demand. After a modest decline in demand in 2020 reflecting the effects of COVID-19, the International Energy Agency projects global gas demand will rebound in 2021 and grow through 2025, with countries in emerging Asia expected to be the biggest drivers of this growth. The result is a continued need for additional LNG export capacity and a fundamental case for LNG over the next several years.

Bottom Line

LNG market conditions have been challenging for much of 2020, but improving prices and fewer cargo cancellations are signs that the worst is likely behind US exporters. The medium and long-term thesis for LNG remains intact given the expectations for growth in Asia, with the competitive landscape potentially becoming more enticing for some exporters given several liquefaction projects have been delayed or canceled this year. While some challenges remain for US LNG exporters, temporary headwinds seem to be subsiding.

{kind=link}

{kind=link}