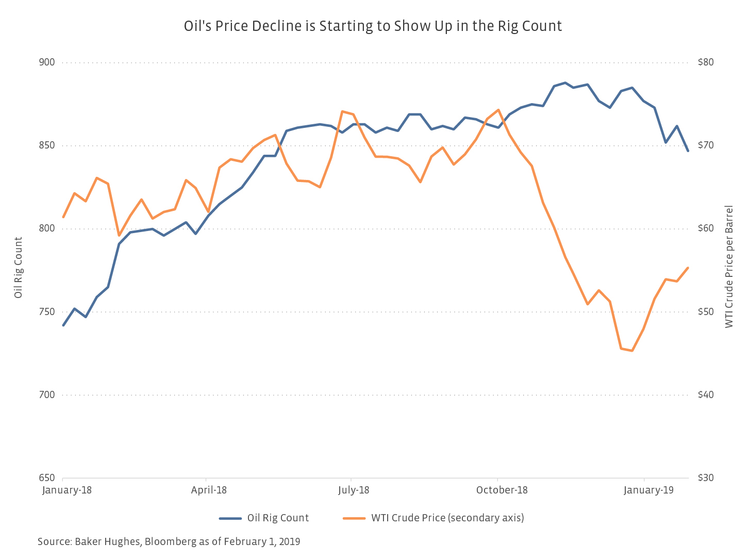

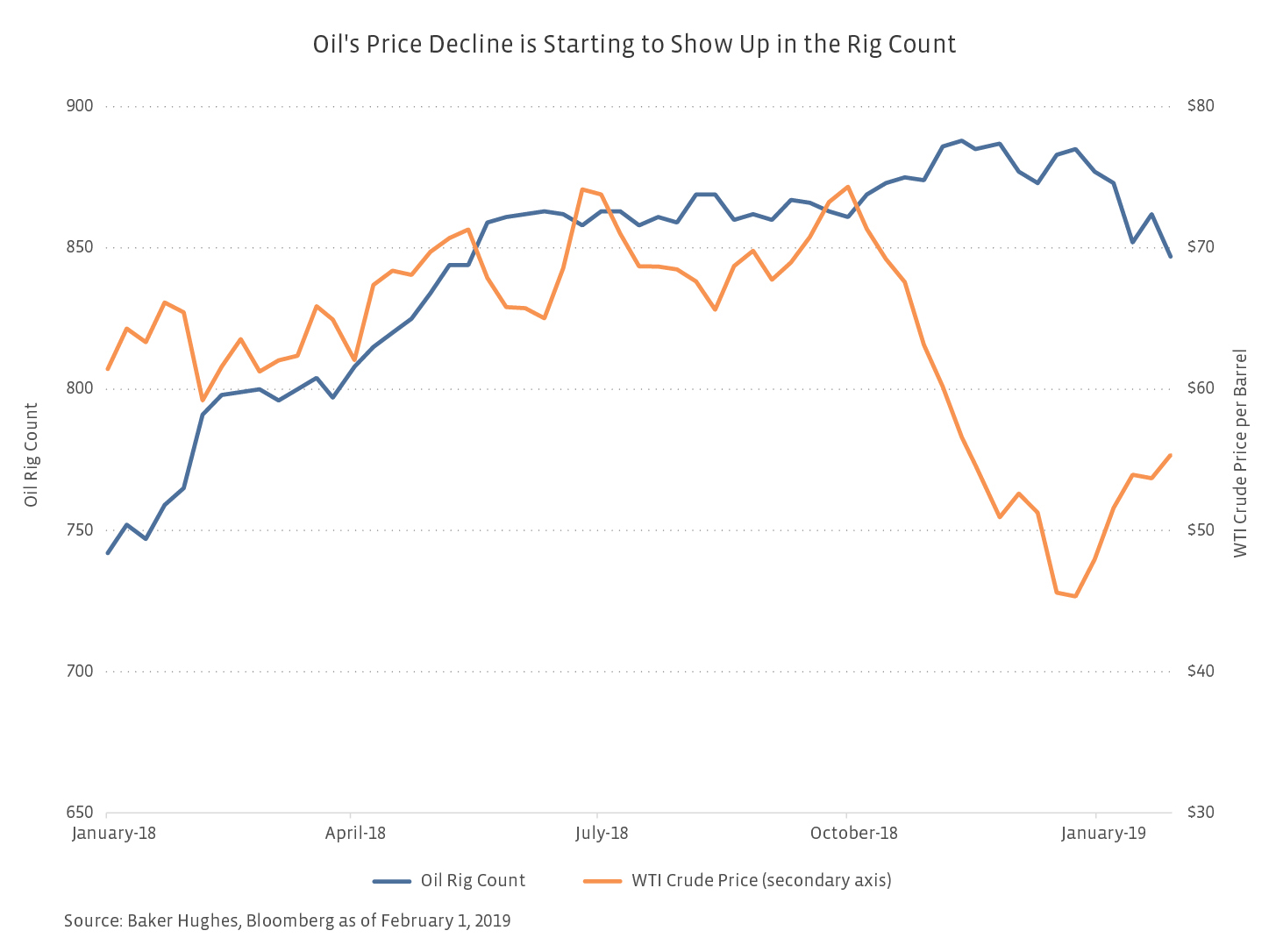

For the week ended January 18, 2019, the oil rig count in the US fell by a steep 21 rigs. To find a weekly decline of a similar magnitude, one would have to go back to early 2016 when the rig count fell by 85 rigs in a three-week period. Energy investors will recall that early 2016 marked a relative bottom for oil as WTI fell to $26 per barrel (bbl) on February 11, 2016. Of course, oil prices in the mid-$50s/bbl recently are in much better shape than in February 2016. Additionally, the US has a backlog of 8,000+ drilled but uncompleted wells (DUCs), which provides some visibility to production growth independent of the rig count. For the week ended February 1, the oil rig count slid 15 rigs after gaining 10 rigs the prior week. As we discuss below, even companies that are reducing their rig count are forecasting robust production growth next year, and the changing makeup of shale producers may also limit production impacts.

How are lower oil prices impacting upstream activity?

In late September 2018, the potential for $100/bbl oil was the topic du jour. The oil price picture changed very quickly as WTI crude fell from $76/bbl in early October to a relative bottom of $42/bbl on December 24. As frustrating as this oil move was for energy investors, it was similarly frustrating for the corporate planning departments of oil and gas producers, which were likely working on 2019 budgets as prices deteriorated. A budget based on $60/bbl WTI may have looked conservative in September but very aggressive in December.

In response to the oil price decline, some companies have adjusted their drilling plans. For example, Permian producer Diamondback Energy (FANG) announced in mid-December that it was dropping three rigs immediately and was releasing two completion crews. While reducing activity, FANG still guided to 2019 production growth of 28% at the mid-point. Similarly, Parsley Energy (PE) announced in December that it would average 12-14 rigs in 2019, down from 16 rigs, but PE anticipates 20% production growth in 2019. In its January presentation, international producer and Permian player Occidental Petroleum (OXY) forecasted 2019 total (i.e. not just Permian) production growth of 8-10% with WTI at $50/bbl. Other companies plan to announce 2019 budgets and drilling plans with 4Q18 earnings, which are currently underway.

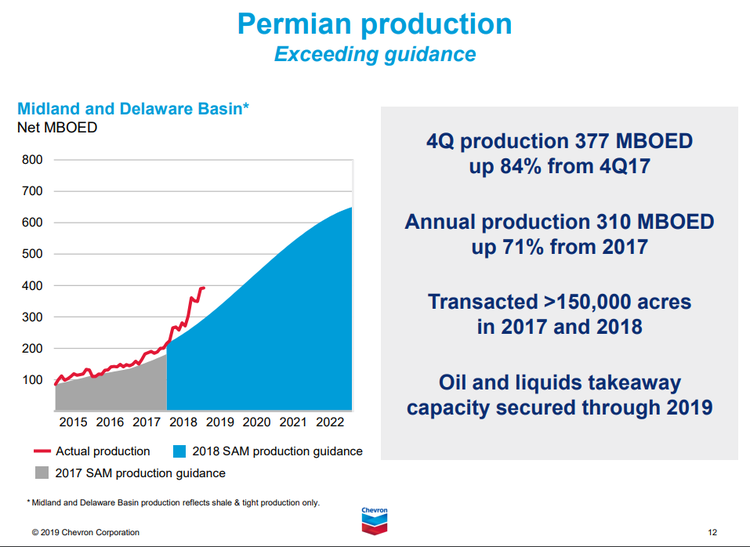

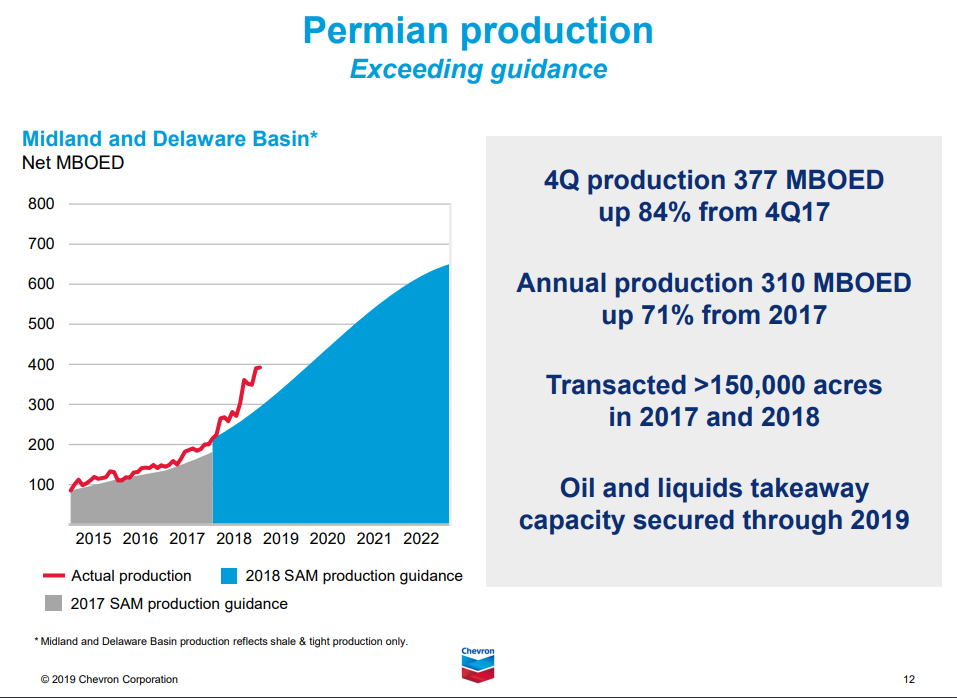

It is also important to keep in mind that the profile of shale producers is changing. Larger producers, including integrated majors Chevron (CVX) and Exxon (XOM), which doubled its Permian position with an acquisition in early 2017, are significant shale producers. These companies tend to be less sensitive to short-term moves in oil prices and predominately focused on long-term targets. Furthermore, shale functions as an important growth driver for these companies, which may face production declines from legacy assets in their portfolios. At its 2018 analyst day, XOM guided to 600 thousand barrels per day (MBpd) of Permian production by 2025, and their 4Q18 earnings call presentation notes that they are ahead of their plan. Similarly, as shown in the slide below from its 4Q18 earnings call presentation, Chevron has seen its Permian production growth exceed prior guidance.

Source: Chevron

Admittedly, we have highlighted only a few companies, and several have not yet provided 2019 outlooks. That said, the combination of growing production from the majors and from E&Ps such as FANG and PE, despite a lower rig count, should help reassure investors when it comes to 2019 production growth.

Is US oil production growth slowing? Should midstream investors be worried?

The US Energy Information Administration’s (EIA) Drilling Productivity Report (DPR) is forecasting month-over-month oil production growth of 62 MBpd in February 2019 from the seven onshore producing basins modeled – a slowdown from the 100+ MBpd month-over-month increases that had been projected for January 2019 and December 2018. The February estimate includes a 23 MBpd increase from the Permian, which has been the powerhouse of US production growth. Winter weather can interfere with production, but February 2017 and February 2018 saw month-over-month increases in production of over 100 MBpd. Considering that there were three months in 2018 when Permian oil production grew more than 150 MBpd month-over-month, the 23 MBpd growth projection falls flat at best and raises concerns at worst.

For most of 2018, the story in the Permian was outsized discounts in crude and natural gas due to insufficient takeaway capacity (though Permian crude differentials have improved recently with WTI Midland trading ~$0.30/bbl below Cushing and only $5/bbl below Houston on 2/1). Some producers discussed reallocating resources from the Permian to other basins or reducing Permian activity given the widened crude discounts. On their 2Q18 earnings call, Noble Energy’s (NBL) management said they would reduce completions in 2H18 and into 2019 in the Permian to better align activity with the addition of pipeline takeaway capacity. As noted on its recent earnings call, Halliburton’s (HAL) management expects activity in the Permian to increase in 2Q19 ahead of additional pipeline takeaway capacity coming online. Early 2019 could mark a relative lull in Permian production growth, as companies accelerate activity in coming quarters once additional pipeline capacity has come online. The Permian maintains a healthy oil rig count at 481 rigs as of February 1 – a modest decrease from the relative peak of 493 rigs in November 2018.

More broadly, the EIA is forecasting that US oil production will grow by 1.2 million barrels per day (MMBpd) in 2019 to 12.1 MMBpd on average (+11%), with most of the growth expected to come from the Permian. Admittedly, this would be a slowdown from the record 1.6 MMBpd increase in 2018, but if you are a midstream company, it would be hard to complain about annual oil production growth exceeding 1 MMBpd.

Bottom line

If EIA projections prove to be correct, US production growth is slowing in the near-term based on expectations for shale production in February and is also slowing in 2019 relative to the record growth experienced in 2018. That said, production growth is expected to remain robust. Production trends are important for midstream companies as volume-driven businesses. Increasing production means more opportunities to build new energy infrastructure. Recent headlines about the falling rig count and slowing production growth may give midstream investors pause, but we believe the outlook for production growth remains strong. Admittedly, a period of 6-8 weeks with WTI in the low $40s could temporarily interrupt production growth as companies adjust plans, but we don’t see the recent oil price pain from 4Q18 causing concern for US oil production today. While we focus on the short-term in this piece, we believe the long-term outlook for US oil production growth remains strong (read more).

{kind=link}

{kind=link}