Our Dallas office is less than a mile from Dealey Plaza, the grassy knoll, and the Sixth Floor Museum, where John F. Kennedy was assassinated. Sometimes when I visit the area, there are a few obsessed people handing out flyers with their personal conspiracy theories. Sometimes they’ve even set up a card table with albums of newspaper clippings. Even 51 years later, part of American culture remains fixated on finding more satisfying answers.

Energy investors found themselves doing the same in a month that featured an election, falling oil prices with OPEC sitting on its hands, and the consolidation of North America’s third largest energy company. All this led to most of us working in energy finance being pressed by our uncles during American Thanksgiving to give them stock tips, as well as enduring tipsy tirades from other drunken relatives about (a) Russia, (b) fracking, © Obama, or (d) why I haven’t moved back to my hometown yet.

Among the conspiracy theories circling around the energy space is whether OPEC and Saudi Arabia are trying to put US frackers out of business. The actual OPEC announcement states only that they are keeping production levels stable, as previously decided in 2011. Still, oil traded into the $60s on the news. Even if this is OPEC’s intention, whether or not it plays out is an entirely different story. US shale producers, even within the same basin, are an exceptionally heterogeneous group with different risk tolerances, capital markets access, and contract structures. This inherently means different breakeven prices, as well as varying degrees of patience should oil prices remain at multi-year lows. And with the cost structure continuing to drift downward in many plays due to efficiency gains, OPEC’s ploy for market share gains may not work out before a self-correction via increased demand takes hold.

In an entirely symbolic yet brilliant political move, Sen. Mary Landrieu (D – LA) pushed for a vote on Keystone XL. She made the vote happen, but it was one ballot shy of the 60 needed for approval. Since the project has now languished for six years, takeaway alternatives for Canadian crude have developed in the interim. It now costs producers $11-$12 per barrel to move Canadian crude to the Gulf on a pipeline, and $17-$18 per barrel on rail.

So far, there have been 18 MLP IPOs this year, which is tied for second-most in history. This month, we saw Antero Midstream Partners (AM) complete the largest MLP IPO in history, raising $1.15 billion in gross proceeds. Despite pricing aggressively at $25, the stock popped 12% on the first day and the units continue to trade above their initial offering price.

Not all new MLPs were so lucky. Navios Maritime Midstream Partners (NAP) saw its deal break despite pricing 25% below the middle of the range. Units tumbled 8% on the first day of trading and ended the month down 13% from its IPO price of $15. MLP investors are no longer assuming that everything with “midstream” in the name is a safe and stable pipeline business. In fact, NAP operates tankers, which typically experience more commodity price sensitivity than long-haul pipelines.

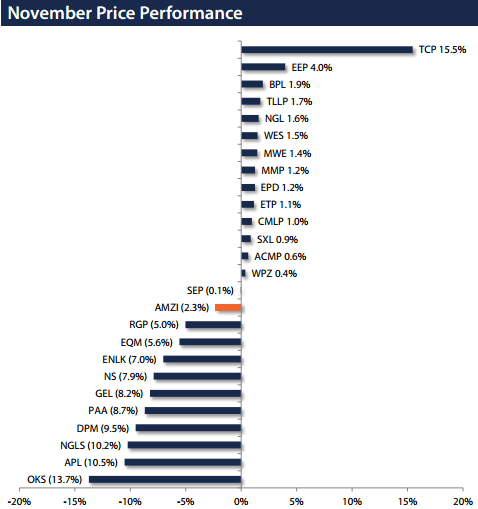

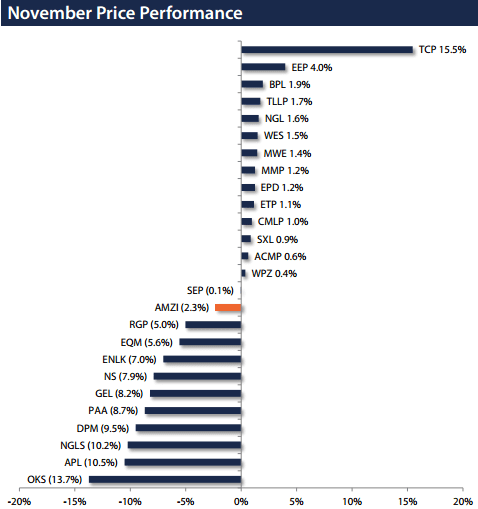

The Alerian MLP Infrastructure Index (AMZI) 1.8% on a total return basis during November. However, it is still up 11.1% for the year. One very bright spot this month was TC PipeLines (TCP), which returned 15.5% for the month. With parent TransCanada (TRP) offering its remaining 30% interest in GTN Pipeline to TCP on November 12th, investors were increasingly confident that management will deliver on the plan to drop down all US assets to its MLP subsidiary over the next few years.

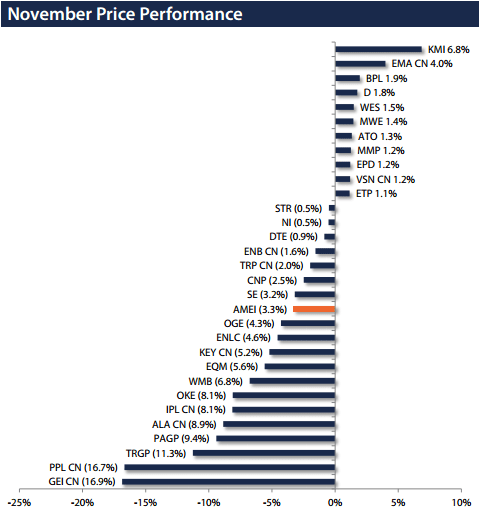

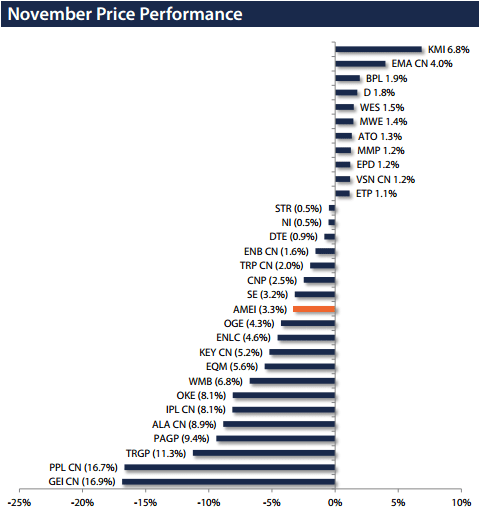

Looking more broadly at North American midstream performance, the Alerian Energy Infrastructure Index (AMEI) lost 3.0% during November. Leading the decline was Gibson Energy (TSX: GEI), which lost 16.9% during the month. Though there was no company specific news, investors were concerned about the sustainability of earnings coming from its commodity-sensitive businesses, which represented 33% of last quarter’s segment profit. Pembina Pipeline (TSX: PPL) lost 16.7% during November despite positive third quarter results and 71% of cash flows coming from fee-based or cost-plus contracts. In contrast, Kinder Morgan (KMI), now one publicly traded company instead of four, was up 6.8% during the month, likely reflecting fund flows into the stock from its meaningfully increased weighting in the S&P 500.

When hindsight is 20/20 and everyone’s a critic, it’s tough to sort through all the rumors and “best new thing” in MLPs. We continue to believe that the long-term build-out of North American energy infrastructure will support overall MLP distribution growth for years to come.

{kind=link}

{kind=link}