I think August is a great month for vacations. In the Northern Hemisphere, it’s too hot to work anyway. Besides, it’s right before school starts and nothing ever happens in the markets during August. (Secretly, I like being in the office during August because it’s quieter and one of the best times for getting work done.) This August, however, we were all fooled.

Easy Money

There was one guaranteed way to make money in MLPs this past August, and you didn’t need hindsight or a crystal ball. Sanchez Production Partners (SPP) announced a 1-for-10 reverse split, effective after market close on August 3rd. Since “each unitholder will get at least one unit,” you could have bought one unit at $1.74 on the record date, and then had one unit for $17.40. It’s a guaranteed gain of 1,000%. Except, few investors can trade without commissions, and a $7.99 fee each way would have resulted in a net loss of $0.32, or 1.8%. So much for one easy trick to make money in MLPs.

Almost Easy Money

ONEOK Inc (OKE), the general partner of ONEOK Partners (OKS), tried the next-easiest way to make money in MLPs: they used cheap debt to buy cheap equity. On August 12th, OKE announced the purchase of 21,544,581 OKS common units for $650 million, or $30.17 per unit. On August 18th, OKE announced that it had sold $500 million of 2023 senior notes. The notes cost OKE $37.5 million annually in interest payments, while $500 million of OKS units equals $52.4 million in annual distributions. That’s technically $14.9 million of free money every year for the life of the notes, but it wasn’t without cost. Moody’s lowered OKE’s credit rating to Ba1 (i.e. junk), and S&P revised its outlook on both companies to negative.

Working for It

Now, if you have an incredible amount of wealth at your disposal, you can make your own luck. On August 6th, Carl Icahn announced an 8.2% ownership stake in Cheniere Energy Inc (LNG), the GP of Cheniere Energy Partners (CQP). A little over two weeks later, it was announced that his group was given two board seats. As the GP has no fiduciary duty to LP unitholders yet controls the LP, this change will also affect CQP holders.

Icahn also holds an 88% equity stake in his eponymous $8 billion diversified MLP Icahn Enterprises (IEP), which holds a majority position in CVR Energy (CVI), the GP of two variable distribution MLPs: CVR Refining (CVRR) and nitrogen fertilizer producer CVR Partners (UAN). UAN agreed to acquire competitor Rentech Nitrogen Partners (RNF) on August 10th, so he technically controls that MLP too. He also owns a stake in offshore driller Transocean Ltd (RIG), the GP of Transocean Partners (RIGP). Suffice it to say he is intimately involved with MLPs.

Final Bidding

Also in progress is the bidding around Williams Companies (WMB), the GP of Williams Partners (WPZ). Final bids were due during the final week of August, but so far, no news has been released. Energy Transfer Equity (ETE) made the initial bid with the caveat that WMB’s merger with WPZ be halted, suggesting that control of the assets in an MLP is more valuable than the assets themselves. Reportedly, Spectra Energy Corp (SE) will also make a bid, as will Kinder Morgan (KMI), though both may face anti-trust issues.

Laggards

August also marked the last upstream MLP holdout cutting its distribution. Memorial Production Partners (MEMP), having maintained or grown its distribution each quarter since going public in December 2011, finally slashed its quarterly payout. MEMP finished down 26.3% for the month. Other laggards included Summit Midstream Partners (SMLP), down 26.4%, possibly due to fears that its dropdown story would fall apart if the parent was acquired. The company also announced the departure of its COO with no replacement mentioned. Crestwood Midstream Partners (CMLP) also finished down more than 20% amid questions regarding the sustainability of its distribution growth.

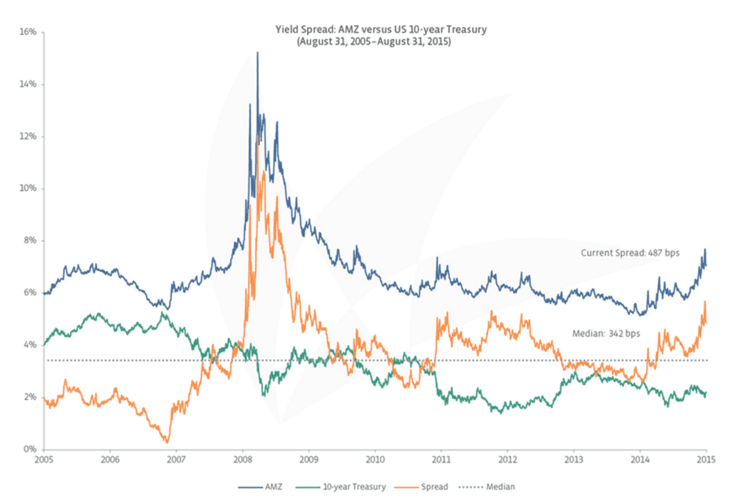

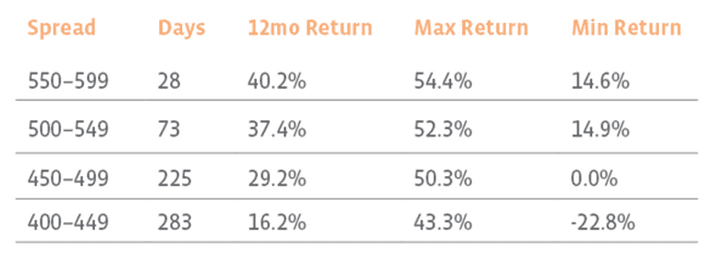

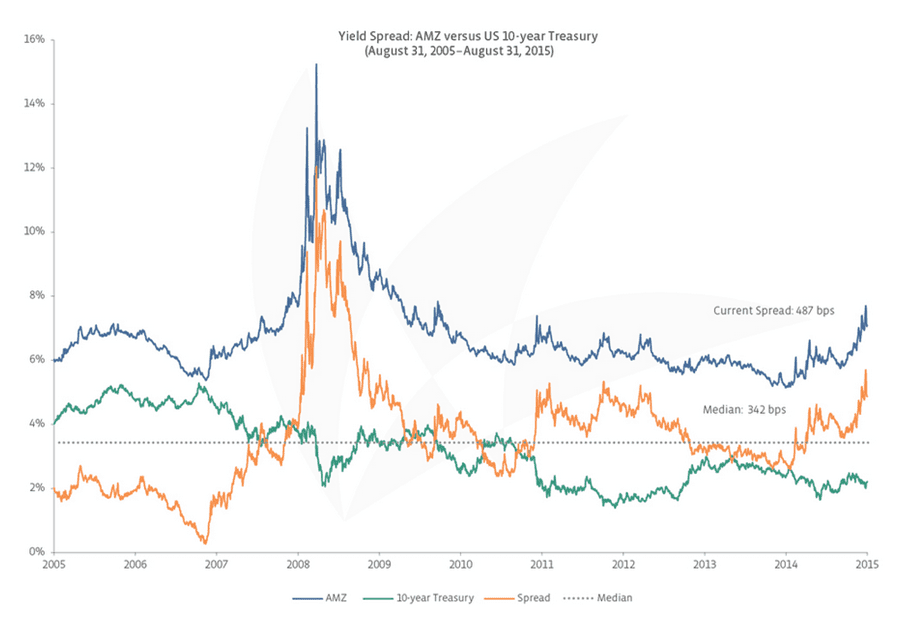

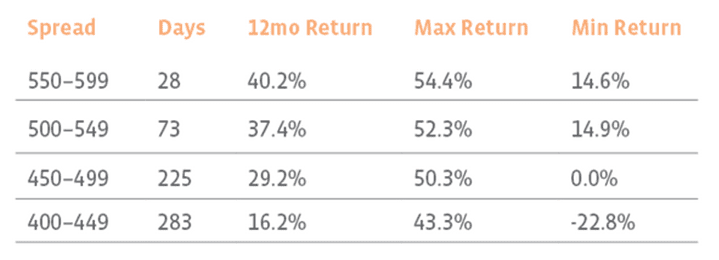

Valuations, Generally

Alerian generally does not comment on valuation, and when we do, we advocate for metrics such as P/DCF or EV/EBITDA over spreads to the 10-year Treasury. Nonetheless, yield spreads are widely referenced, and for that reason alone are at least worth following anecdotally. Over the past 10 years, the median spread to Treasuries has been 342 bps. Currently, it stands at 481 bps for the AMZ and 487 bps for the AMZI, after reaching a high of 570 bps in August. Talk of rate increases is everywhere, but if MLP investors really are concerned with Fed rate hikes and inflation, and do not believe MLPs are undervalued, this implies these investors also believe the 10-year is on its way to 3.7%.

{kind=link}

{kind=link}