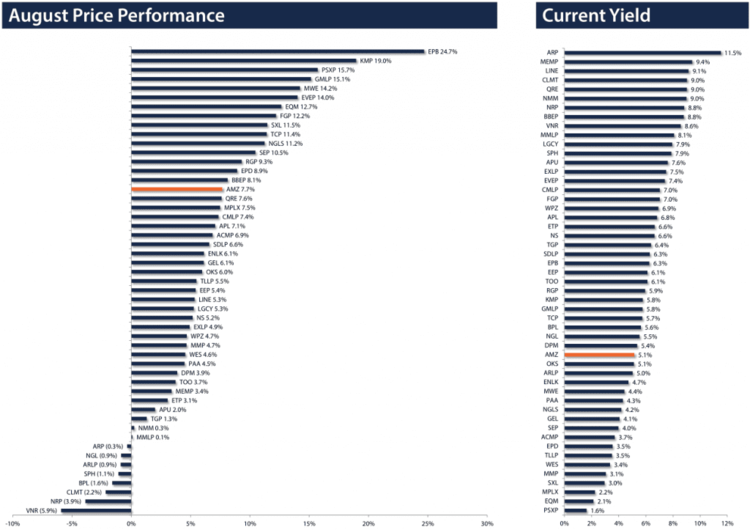

Anyone who has read anything about MLPs in the past month knows about the Kinder Morgan transaction. Let’s start the school year by focusing more broadly on the MLP space. Aside from saying that a rising tide can lift all ships (and the AMZ was up 7.7% on a price return basis for August), let’s focus on what else happened.

The month opened with an MLP roundtable as Barron’s feature article, “The New Frontier for MLPs.” There’s a really good section that I want to quote wholesale. Becca Followill from US Capital Advisors and Michael Blum from Wells Fargo are asked questions on MLP M&A:

Followill: The first half of the year saw about $31 billion in deals, up from $29 billion for the first half of 2013. Part of what is driving it is a general view that we have found all the big shale plays, so now we have maturing basins [large-scale rock formations that often contain fossil fuels] — Bakken, Permian, Eagle Ford, Appalachian — and there’s a bit of a land grab going on. Companies want a strategic asset in a basin, and many are willing to pay up for it.

Blum: The cost of capital is low right now, and MLP valuations are high, so they’re in a good position to make acquisitions. At the same time, this is a pretty good time for private-equity investors to sell.

Later, Blum adds that he’s “been surprised by the level of M&A in this market, because MLPs have a lot of opportunity for organic growth, and the returns on those projects will be much higher than they will be for mergers.” As it turns out, MLPs were active on both the acquisition (buying a new backpack) and the organic growth (sewing that backpack yourself) fronts this past month.

Martin Midstream Partners (MMLP) acquired the remaining ~58% interest in Cardinal Gas Storage Partners for $120 million, increasing their percentage of fee-based business and giving management cause to recommend a distribution increase. Previous to this acquisition, Alinda Capital acquired a ~50% interest in MMLP’s general partner, giving MMLP access to further dropdowns. Despite these opportunities, MMLP was nearly flat for the month, perhaps due to investor concern for price paid, debt used, and/or leverage incurred.

Natural Resource Partners (NRP) announced their $205 million purchase of VantaCore Partners, a privately held MLP that owns hard rock quarries, sand and gravel pits, asphalt plants, and a marine terminal. With NRP’s purchase, VantaCore is now no longer a potential IPO candidate.

While we’re still discussing acquisitions, we would be remiss to exclude the merger-that-wasn’t. In July, NGL Energy Partners (NGL) acquired the general partner of TransMontaigne Partners (TLP) and offered to buy the remaining interest in TLP. However, on August 15th, the companies issued a joint press release indicating the termination of discussions. While we won’t know what happened behind closed doors, the market has speculated that talks broke down over price. NGL still owns the GP of TLP, though.

On the organic growth side, back-to-school shopping was all about foreign exchange students and studying abroad (ie imports and exports). Oregon LNG received a 20-year permit to export natural gas to countries without free trade agreements with the United States. The facility would include an LNG export facility to be built near the mouth of the Columbia River. While Oregon LNG is owned by Leucadia National Corporation (LUK), the project would receive gas from Northwest Pipeline, a Williams (WMB) system that provides access to gas from Canada and the Rocky Mountains, as well as the San Juan Basin.

On the quasi-export side, Hawaii and other US territories are highly dependent on petroleum imports, as they do not have resources locally and are very remote from most places that do. While they have historically imported petroleum products for most energy demands, Hawaii and Puerto Rico are now testing the viability of small-scale LNG imports.

I’d like to stretch the school analogy further, but if I start talking about taxation and budgeting, we’ve just gone too far down the rabbit hole. Still, there was another significant happening in August that I would be remiss not to mention. The Joint Committee of Taxation, a nonpartisan committee of the US Congress, released their yearly study of all US tax expenditures. Notably, remarkably, MLP tax expenditure estimates decreased from the estimates made during last year’s study. Fluctuation is normal and expected in this study, but given the size of the industry ($590 billion), the tax expenditure ($1.26 billion per year) is quite low. Last year, the tax expenditure estimate was $1.5 billion per year relative to a market capitalization of $330 billion as of the start of 2013.

The lower tax expenditure is due, at least in part, to accelerated depreciation rules, which benefit those MLPs that are continually building assets. Which is to say, given the energy renaissance, nearly all of them.

{kind=link}