OPEC+ decision to extend output cuts alleviates some uncertainty.

While significant uncertainties remain in the oil market, OPEC and its allies (dubbed OPEC+) provided a dose of clarity by announcing a nine-month extension of their existing output cuts through March 2020, longer than the six months expected. OPEC+, which formalized the partnership between OPEC and its non-member allies with a “Charter of Cooperation,” agreed to maintain combined cuts of about 1.2 million barrels per day (MMBpd) as the group attempts to balance relatively tight supply conditions in light of US sanctions on Iran with a slowing global economy. In terms of compliance, OPEC+ fell short of delivering targeted cuts in January and February but have improved noticeably since then. Monthly compliance for March through May averaged 135.3% of targeted cuts according to data from the International Energy Agency (IEA). The continuation of production cuts from OPEC+ removes one significant wildcard for oil prices until at least the next OPEC general meeting in December.

US-Iran tensions drive increased geopolitical risk.

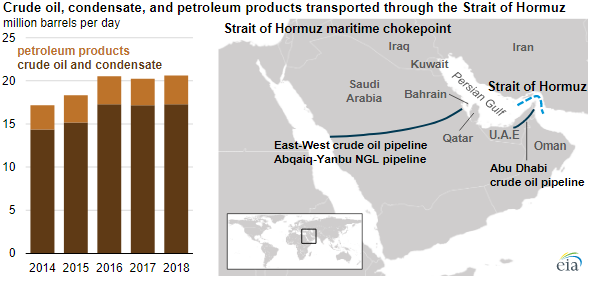

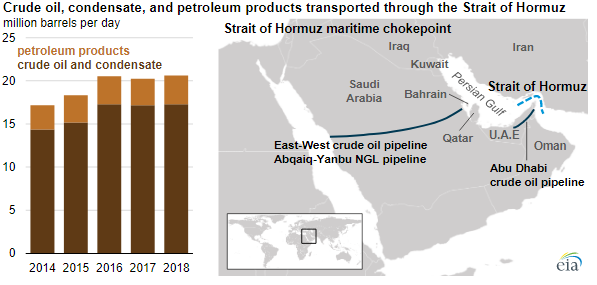

While US-Iran tensions have subsided somewhat recently, geopolitical factors have contributed to revived volatility over the last few months. In April, the Trump Administration announced it would not extend sanctions waivers for countries importing Iranian oil in an attempt to exert maximum pressure on Iran. Tensions between the US and Iran have flared over the last month near the Strait of Hormuz (see map below). In June, two oil tankers were attacked in the nearby Gulf of Oman, and a US drone was shot down over international waters in the Strait. The Strait of Hormuz is a crucial chokepoint for seaborne crude, with 20.7 MMBpd transported through the Strait on average in 2018, which represents about one-fifth of global oil demand. Tensions in the region remain elevated, and an escalation of conflict could impact oil flows from the region, leading to supply disruptions. While we see an interruption to oil flows through the Strait as unlikely, tensions reinforce the geopolitical risk in oil prices.

Source: Energy Information Administration

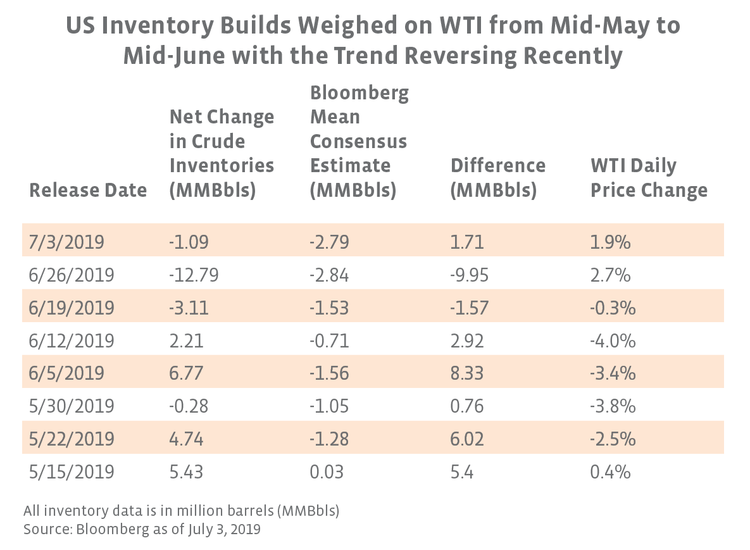

US crude inventory draws support oil prices after several weeks of large builds.

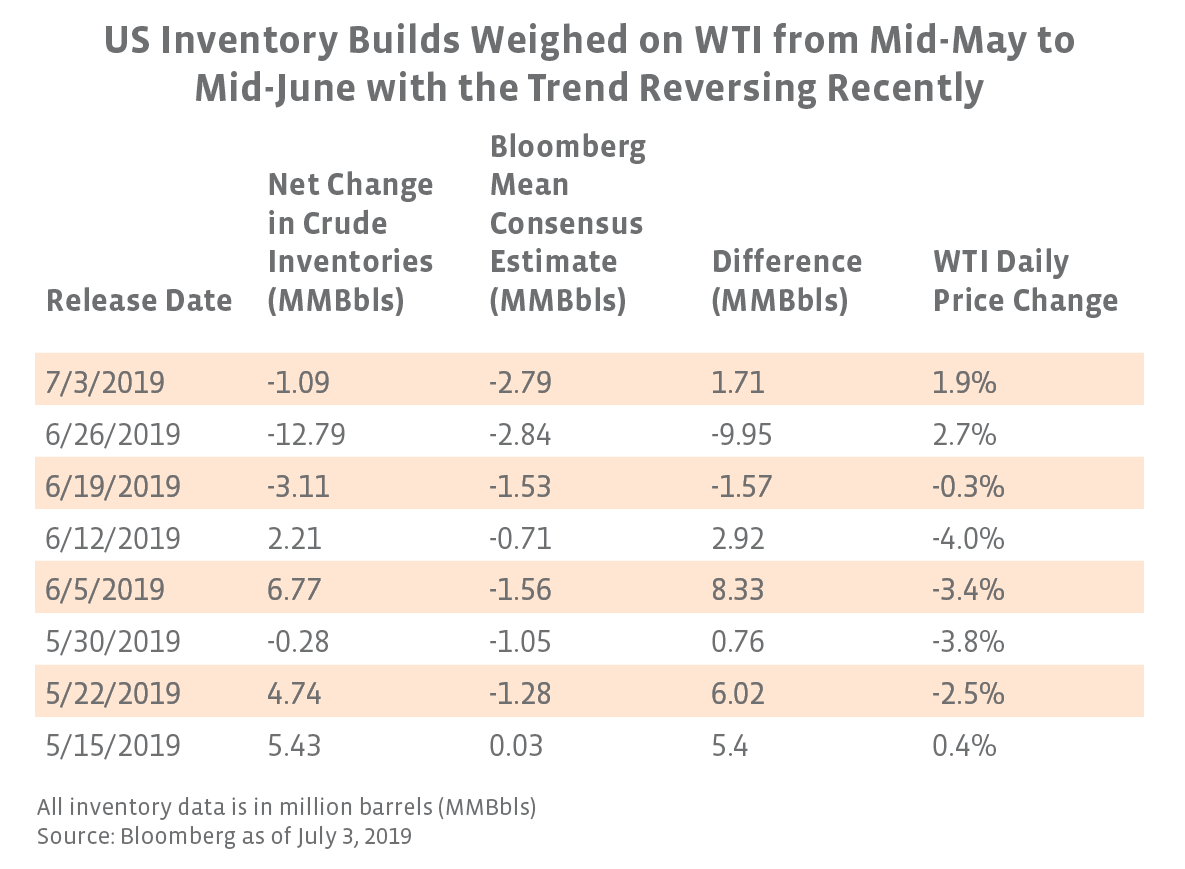

The Energy Information Administration’s (EIA) Weekly Petroleum Status Report provides data on US oil inventories (among many other data points) and typically influences oil prices upon release. The EIA has reported inventory draws for three consecutive weeks, including a large draw of nearly 13 million barrels for the week ended June 21. This decrease marked a reversal from the large, unexpected builds in mid-May and early June (see table below). These builds can largely be attributed to rising US crude imports and lower refinery utilization. May refinery utilization averaged 90.5%, which was below the five-year average of 91.3%. With refining utilization steady at over 94% for the last two weeks of June, crude inventories may continue to draw if imports moderate.

Slowing demand growth represents the primary downside case for oil.

While we have seen mostly bullish risk factors on the supply side, concerns have increased that the global economy is slowing, which would have a negative impact on global demand growth for oil and thus prices. The IEA cut its global oil demand growth projection for full-year 2019 from 1.4 MMBpd in April to 1.2 MMBpd in June, marking two consecutive monthly decreases. Similarly, OPEC cited slower demand growth as one of the primary reasons for its extension of supply cuts and trimmed its 2019 demand outlook by 70 MBpd in June to 1.14 MMBpd. The IEA currently projects non-OPEC supply growth of 1.9 MMBpd in 2019, but outsized non-OPEC supply growth could prove bearish if demand weakens further with OPEC+ already cutting.

The ongoing trade war between the US and China and a potential interest rate cut from the Federal Reserve also carry implications for oil demand. At the G20 summit in late June, the US and China agreed to renew trade negotiations and halt implementation of new tariffs – a positive development for the broader market. A conclusion to the trade dispute or an extended détente would potentially boost the trade and economies of both countries and therefore support oil demand. At its June meeting, the Fed decided to hold interest rates steady but suggested in its written statement that a rate cut was possible at a future meeting. Interest rate cuts are constructive in their potential to bolster the broader economy, supporting oil demand, while a weaker dollar is supportive for crude prices.

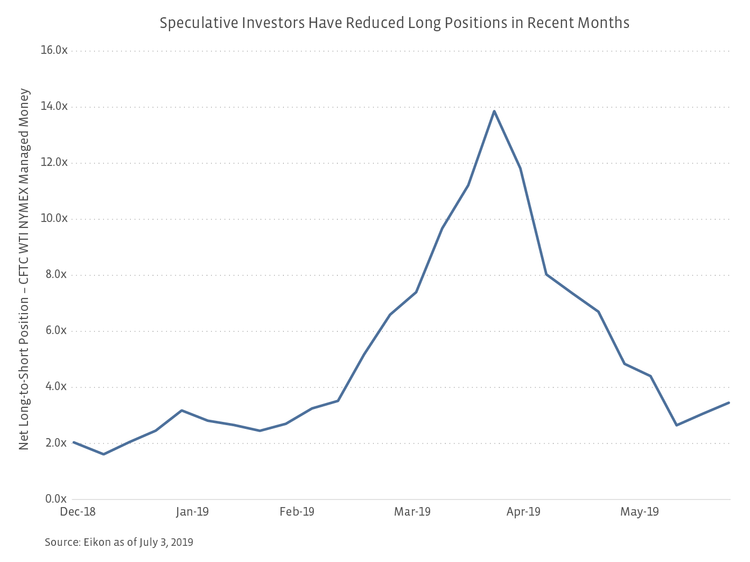

Speculative money has tilted more bearish on oil.

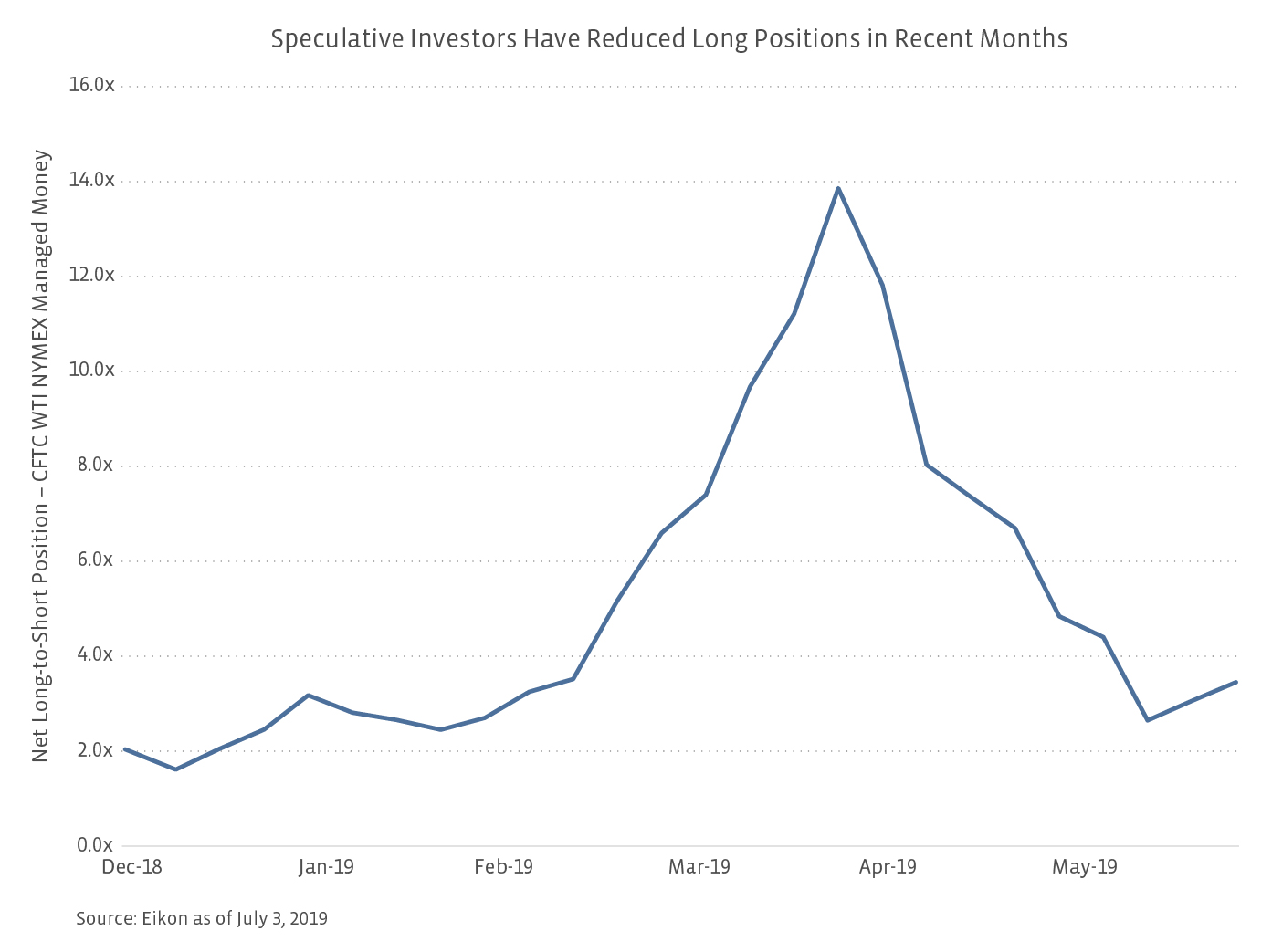

The positioning of speculative investors, such as hedge funds and other money managers, has turned relatively bearish in recent months. According to Refinitiv Eikon, the net long position for managed money in WTI crude oil decreased from a 13.9x net long-to-short position on April 23 at oil’s relative peak to 2.6x on June 11 (see chart below). While the net long position has ticked up to 3.5x in the most recent report on June 25, this increase likely resulted from short covering rather than an absolute increase in long positions. Liquidation of long positions over the last few months indicates speculators have some concerns about oil fundamentals; however, the pace of liquidations has slowed in recent weeks, which may indicate a reversal of sentiment.

Midstream’s defensive business model is attractive during periods of oil volatility.

With oil price volatility likely to persist, midstream may be an attractive investment option within energy because of the defensive nature of the business, which generates fees based on the volumes of hydrocarbons transported, stored, or processed. As a result, midstream cash flows are less sensitive to commodity price moves and are insulated from the direct effects of price volatility. This defensiveness was evident in the recent pullback in oil prices. While WTI dropped 22.9% from its recent high on April 23 to its relative low on June 12, the Alerian Midstream Energy Index (AMNA) fell only 3.8% on a price-return basis, while the Energy Select Sector Index (IXE) fell 12.3% on a price-return basis during the same timeframe. When comparing the sector to other energy investments, midstream stacks up favorably for those concerned about oil price volatility going forward.

Bottom Line

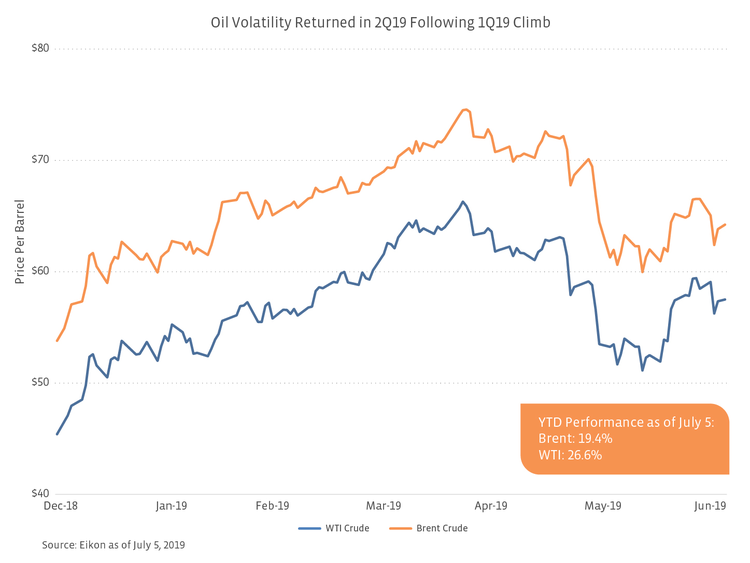

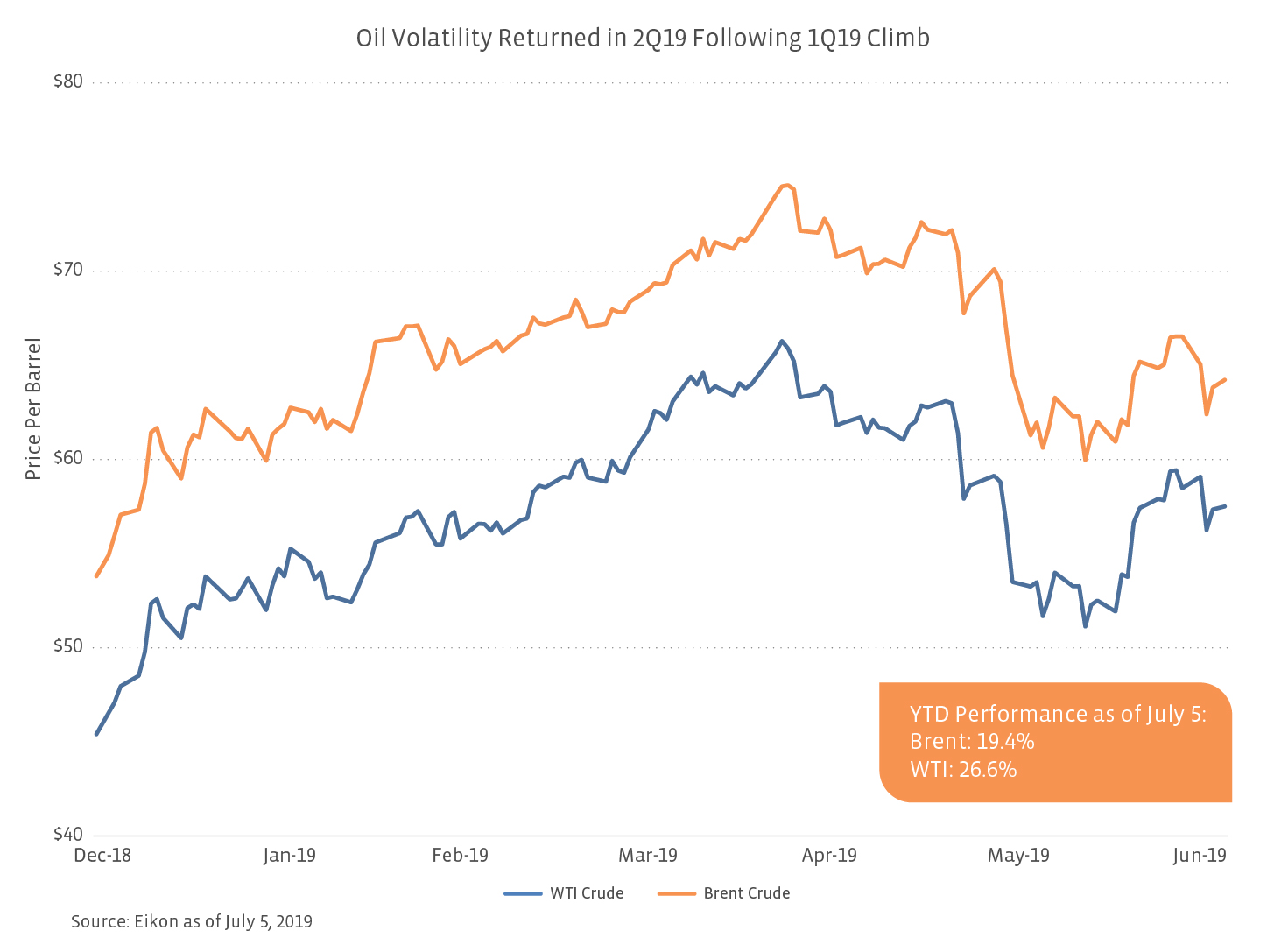

After climbing during the first four months of the year, crude prices have turned volatile in recent months in large part due to the variety of political and economic wildcards that have disrupted (or threatened to disrupt) the oil market’s supply and demand balance. Given the continued presence of sanctions and tensions between the US and Iran, the ongoing trade war between the US and China, and the potential for an economic slowdown, oil prices are likely to remain volatile in the short term. Investors can look to midstream for energy exposure that is more defensive in a volatile price environment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}