Last week, we examined how MLPs spend and categorized the cash necessary to maintain their assets and cash flows. This week, we’ll look at how they are spending capital to grow cash flows, either through building or buying new assets. Just like last week, we looked at the 18 MLPs in the Alerian Large Cap MLP Index (AMLI) that are not general partners. Luckily, despite no legal requirement, the majority of these companies not only disclose their capex numbers and break them out in maintenance and growth, but they also provide future guidance for the coming year’s capex.

At the beginning of the year, large caps had a collective market cap of around $218 billion, and all but two of the MLPs provided growth capex guidance. Collectively, they expect to spend about $19 billion this year to grow their businesses. Excluding the two MLPs, this compares to spending of $28 billion spent in 2015.

How Growth Capex Translates to Distribution Growth

Spending money to buy a turn-key asset will (if done correctly) be immediately accretive to distributions, and investors may expect to see higher payments as soon as the following quarter. However, if the asset is to be built, investors may not see a distribution increase from those dollars until the asset is not only in service, but operating at capacity. This could take months, or it could take many years. The saving grace here is that while growth capex dollars are generally committed by the time a shovel goes in the ground, they are only spent as needed.

Growth Capex: Is More Better?

Some years, MLPs gleefully report that they’ve identified seventy-jillion dollars of growth opportunities. Since the money spent on growth will translate (sooner or later) into distribution growth, investors often greet this news with enthusiasm. Especially in boom years like 2012.

However, in other years (like, say 2015), MLPs will proudly announce that they’ve been able to identify forty-jillion dollars of growth projects that can be canceled or delayed. Given that projects cost money, and access to capital has been limited (or expensive), especially for non-investment grade MLPs, the ability to delay projects can protect an MLP from needing to cut its distribution in order to fulfill its own contracts.

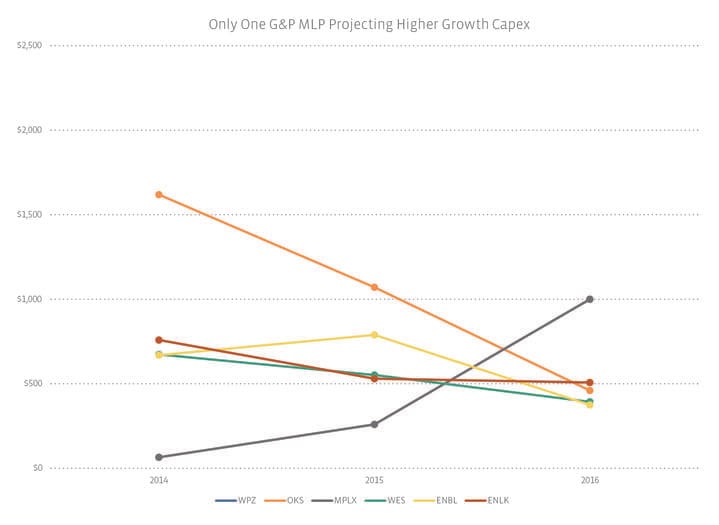

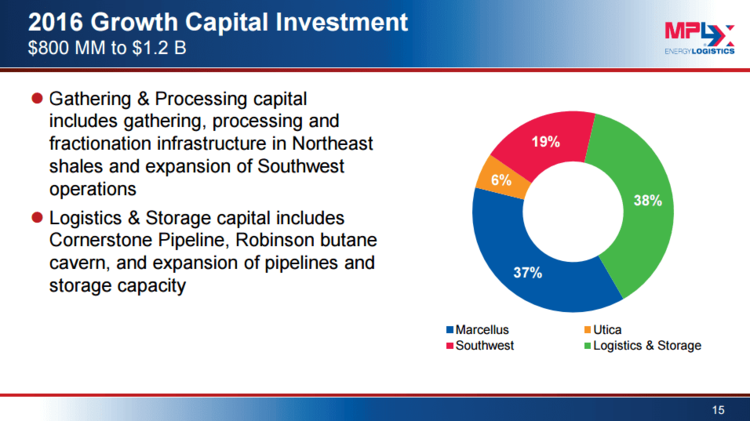

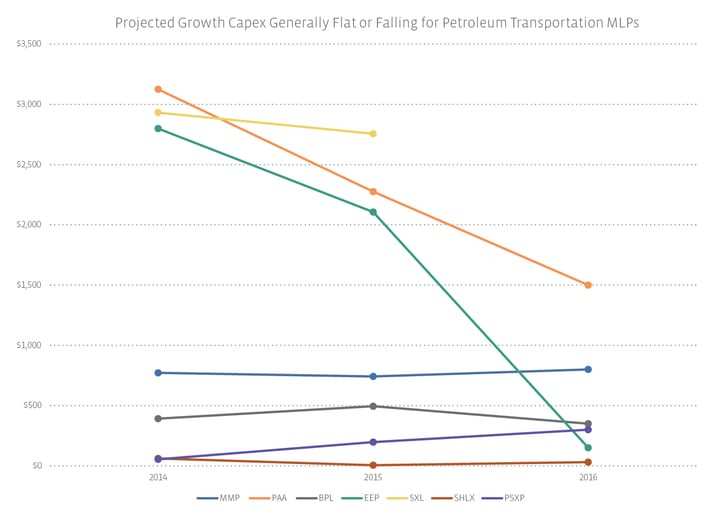

How Does Your Company Grow?

A few MLPs categorize the money they spent on acquisitions as separate from growth capex. Unless an acquisition is structured to be accretive (ie increase distributions) it’s possible that the extra cash flow from that acquisition covers only the distribution for the units issued to pay for it. Non-accretive acquisitions are rare and if they happen, it’s not like a company would proudly proclaim it after the fact.

Acquisition capex is very important for dropdown stories, as it signals how much the company will be able to grow that year. However, spending $100 million on an acquisition doesn’t guarantee a certain amount of EBITDA, which is why the industry prefers to think about acquisitions not in terms of absolute price, but in terms of how much EBITDA it generates in relation to the price. If the parent sells the asset at a price that is 10 times the EBITDA it generates (called a 10x multiple) that MLP will add $10 million to its EBITDA base. While unlikely, a parent could sell the asset to the MLP at a bargain price of 5x EBTIDA and then the MLP will add $20 million of EBITDA every year. Growth is different for every case.

After the MLP has acquired all the suitable assets from the parent, where does growth come from then? It will need to either buy assets from a third party, or build them itself.

Just as growth solely from dropdowns will eventually end, as Kelcy Warren was recently quoted in the NY Times for saying, “One cannot live on organic growth alone.” Typically, both types of growth will be needed for an MLP. As helpful as acquisition capex projections would be for investors, an MLP may chose to keep that number private, so as not to tip off any competitors about how much they are willing to spend.

Who Is Spending the Most?

On a pure dollar basis, Energy Transfer Partners (ETP) estimates that it will spend $4.2 billion in 2016 on growth projects. That’s down from the $4.95 billion it estimated at its November 2015 analyst day. As a percentage of total market cap, ETP once again will be spending the most: that $4.2 billion is approximately 30% of the currently $14 billion company.