[Note: The Alerian Mid Cap MLP Index (AMMI) is included in all tables, but the analysis provided here is between large and small caps. Mid cap MLPs perform somewhere in the middle, but more similarly to large caps than to small caps. My colleague, James Wang, has explored the differences between the indices in depth and concluded that the AMMI “came away with the best balance of stability and performance” over the past ten years.]

Intuition Is Wrong: A Counter Example

It seems surprising, right? We can all think of small cap MLPs that have had remarkable performance in 2016. To illustrate just one: American Midstream Partners (AMID) is up nearly 300% from its lows last December. The units jumped 30% at the end of the year on the announcement that its general partner, private equity firm ArcLight, believed it was undervalued and would be purchasing $75 million in units. Then it jumped another 30% in the week following the April announcement that AMID would be cutting its distribution, a move the market viewed as prudent. That press release also included news of $225 million of acquisitions, which would increase the size of the company by over 50%.

So the first lesson we can learn from this is that the plural of anecdote is not data and human brains are fallible. AMID may have done well, but two other companies filed for bankruptcy and were removed from the AMSI. AMID may be up 300%, but two other companies are down over 90%. Even beyond that, as my brain popped up example after example, was how many of these high performing small cap MLPs have received external help. As with AMID, this could come in the form of an investment from an outside party, or a dropdown from the parent, or other payment (IDR) relief. These are positive and helpful signs the market recognizes, but importantly, they are not operational or fundamental improvements.

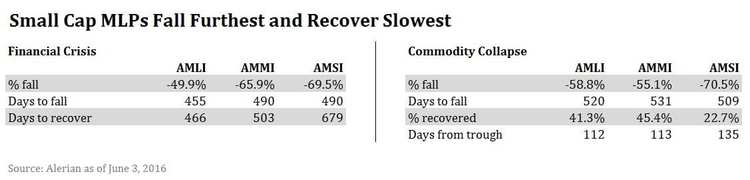

Small Caps Fall Fastest, Fall Hardest

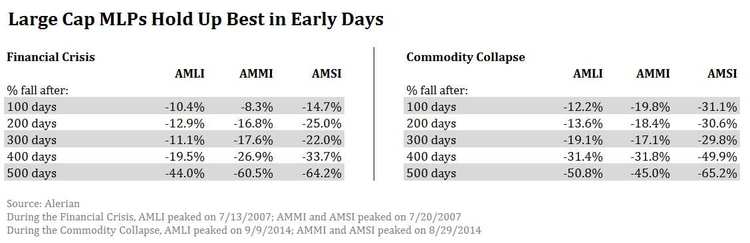

Small cap MLPs led both bear markets, falling 50% further than large caps did in the first 100 days. Large caps managed to keep losses to 10%-20% until well over a year into the pull back. In a difficult environment, it will be those MLPs with the thinnest balance sheets and most concentrated risk that are least able to maintain business as usual. In the slow-moving, always-cautious energy infrastructure business, it appears that there is no such thing as being nimble.

This table does raise one chicken-or-the-egg question: do large caps respond as the rest of the space is hitting a bottom, or do the falling unit prices of large caps signal the bottom?

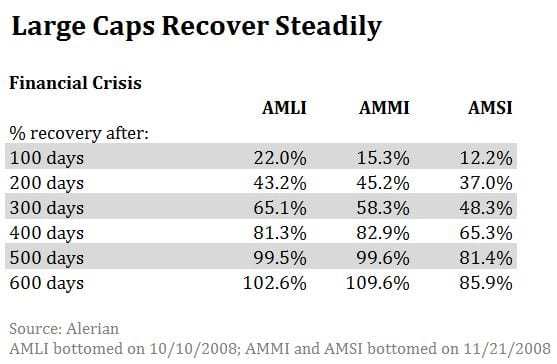

Last Time, Large Caps Recovered and Recovered and Recovered

We are now just over 100 days into the current recovery (in the case of the AMSI: 135 days since it bottomed in January). Large caps are up over 40% and small caps are up over 20%. To compare this to the recovery during the financial crisis:

The current recovery seems to be happening much faster than the last one, as each index is already much further along than it was after 100 days back in 2009. It may be that if you aren’t already invested, you missed the first and biggest boat. Then again, we could always retest the bottoms. Or MLPs could go up 300% tomorrow. My crystal ball is cloudy today. Jokes aside, this is a data set of one (2007-2009) and as I mentioned above: the plural of anecdote isn’t data. It is entirely possible that small caps could make a steeper, faster recovery this time around.

If you believe this recovery will look like the last one, and you want to get into the game now, an investment in large cap MLPs may make sense if you don’t mind that you’ve missed the first 50% and you believe the recovery will continue at this pace. However, small cap MLPs may make sense for the portfolio of the investor who believes history will repeat, wants to get in closer to the bottom, and doesn’t mind if the recovery takes a while.

2016.06.10 11:00am CST – Edited to clarify the decline period of the AMSI.