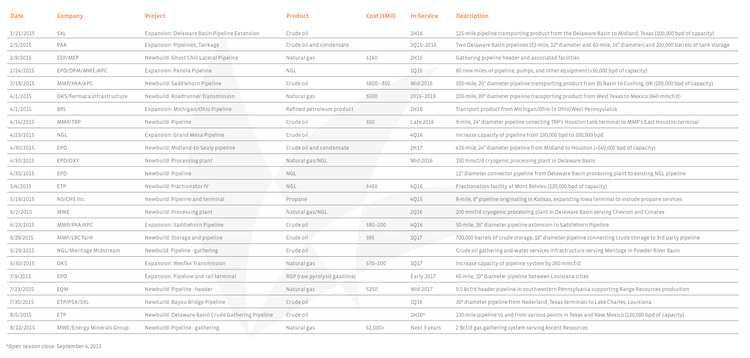

In aggregate, 24 projects have been announced by these MLPs in a standalone press release since the beginning of the year:

- By asset built: 21 pipelines, 2 processing plants, and 1 fractionation plant

- By construction type: 16 newbuild projects and 8 expansions to existing systems

- By product handled: 11 projects handling crude oil, 5 handling natural gas, 5 handling NGLs, and 3 handling other products

The projects are in basins across the US, but the basin that saw the highest number of announced projects was the Delaware Basin, bordering Texas and New Mexico in the western part of the Permian.

Only 10 of the projects disclosed estimated costs. When taking the low end of the estimates, these 10 projects will cost at least $3.5 billion.

The vast majority of these 24 projects are committed projects. Commitments can come in the form of a binding open season commitment, a negotiated contract to serve a producer’s acreage in a particular area, or a negotiated commitment to build a project based on a customer’s request.

I mention that the “vast majority” of projects are committed because some projects, such as connector pipelines, are built to improve the overall flow of systems and may not necessarily need an anchor shipper or receive firm commitments before being built. If there’s congestion on an existing system, it’s clear that the demand to decongest it is there.

While you may not see a headline announcing a new infrastructure project as frequently as you see commodity price change headlines, know that they are there. And unlike commodity prices that change every single second, these infrastructure projects are hard assets that will exist for many years to come. These projects point to the fact that infrastructure MLP cash flows are not only stable, but also growing. Whereas current levels of MLP cash flows are based on projects that are already in service, future levels of MLP cash flows—and distribution growth—will come from additional project announcements, such as these 24.

{kind=link}