By Dave Dierking

- Up until recently, dividend stock performance has been a mixed bag with high yielders being notable underachievers.

- A COVID vaccine-inspired economic recovery in 2021 could put value stocks, dividend payers and cyclicals back into market leadership positions.

- PEY is well-positioned in the themes that are poised to outperform over the next 12 months.

- Requiring 10+ year dividend growth histories to qualify for the portfolio adds a degree of safety should the market turn sideways.

- The current 4.5% dividend yield is well over double that of the S&P 500 and the dividend aristocrat universe.

Investment Thesis

Investing in the universe of dividend aristocrats remains one of the most popular income-producing strategies among investors. But they’re usually not known for their high yields. The ProShares S&P 500 Dividend Aristocrats ETF (NOBL ), perhaps one of the best benchmarks for this universe, yields just over 2%.

It doesn’t have to be that way. The Invesco High Yield Equity Dividend Achievers ETF (PEY ) provides exposure to long-term dividend growers and offers a yield of 4.6%, but it comes with some additional risks that investors should consider before jumping in.

Overview

In a market that has largely rewarded large-cap growth stocks up until recently, dividend ETF performance has been something of a mixed bag. As a whole, dividend stocks have underperformed the broader market, but there have been pockets of success.

Long-term dividend growers have generally achieved the best results. The period just before the great Fed pivot of 2018 and the 2020 COVID pandemic left many equity investors seeking out a “flight to safety” trade. Dividend growers and their relative balance sheet health and stability fit the bill for investors who wanted to maintain equity exposure but remain on the more conservative end of the spectrum.

High yielders, on the other hand, have suffered. High yield was generally interpreted as high risk, exactly the type of securities that made less sense in a declining market. Some high yield stocks didn’t necessarily come with above average risk, but many did and that was enough to make this segment of the market a significant underperformer.

Quality dividends, those backed by strong margins and cash flows, have fallen somewhere in the middle. I’m a bit surprised by this since their very definition should have been something that dividend investors would have sought out, but dividend growers ended up being about the only group that managed to reasonably keep up with the market.

November has been a different story.

With Pfizer’s (PFE) news that the COVID vaccine it has been developing delivered encouraging results in its trial, followed by additional promising results from the likes of Moderna (MRNA) and AstraZeneca (AZN), investors have shifted their focus to a post-COVID economy. While short-term economic risks, including additional social and business restrictions in some states, are still quite high and a double-dip recession isn’t out of the question, the idea of a full-fledged economic recovery is definitely on investors’ minds.

That puts some of the market’s previous underperformers, including cyclicals, value stocks and dividend payers, back into focus. These are the types of sectors that tend to outperform coming out of an economic trough. We’ve already seen this narrative start playing out in November and there’s reason to believe that this trend could continue barring any unforeseen hiccups in the re-opening trade.

That could put the Invesco High Yield Equity Dividend Achievers ETF (PEY) squarely in the market’s sweet spot.

Background

PEY benchmarks to the NASDAQ US Broad Dividend Achievers 50 Index. To qualify for inclusion in the index, a company must have increased its annual regular cash dividend payments for at least 10 consecutive years and must have a minimum market cap of $1 billion. The final index includes the 50 companies with the highest yield that meet the above criteria and yield-weights the underlying components.

You can see the differences with NOBL right off the bat. PEY uses the “dividend achiever” designation, not the “dividend aristocrat” definition, so it has somewhat looser criteria for making it into its dividend growth portfolio. PEY also yield-weights its portfolio of the 50 highest-yielding names, whereas NOBL equal-weights all companies that have 25-year dividend growth streaks.

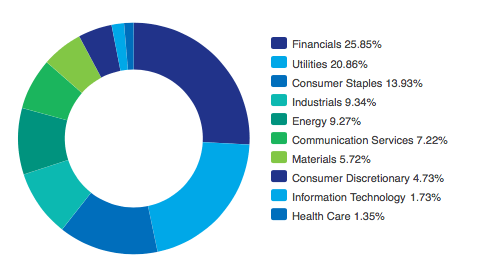

As you might expect, the high yield targeting component leads to overweights in areas of the market, such as utilities and financials, that may be more economically sensitive. In order to reasonably expect PEY to outperform over the next 12 months or so, we really need to see follow-through on the vaccine development, a slowing of the coronavirus spread and a corresponding recovery that would come with a wide-scale reopening.

As mentioned earlier, PEY’s current portfolio positioning could make it a prime candidate to do particularly well if the recovery scenario plays out.

Profile

PEY’s portfolio is filled with the types of names you might expect. There’s a heavy presence of financials, utilities and consumer staples – the types of companies that are big cash flow generators and have the ability to sustain shareholder payments over time.

The one thing you won’t find much of is growth stocks. The tech sector is a scant 2% of the portfolio, while consumer discretionary and communication services can’t even get near a double-digit allocation. Even the companies that qualify from comm services are the traditional telecoms, like AT&T (T) and Verizon (VZ). This is a portfolio comprised almost entirely of defensive and cyclical sectors.

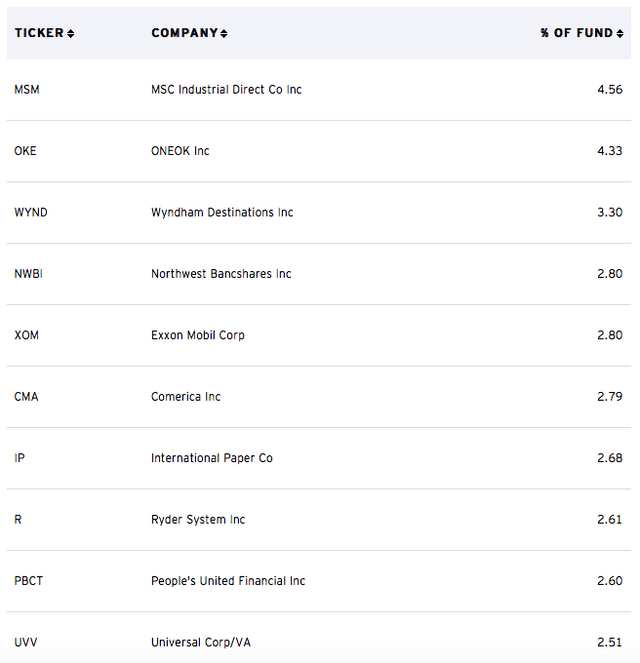

It’s an interesting group of names in the top 10, including several names who might be getting ready to get booted. Wyndham Destinations (WYND) will get kicked out at the next reconstitution since it’s already cut its dividend. Other names, including ExxonMobil (XOM), International Paper (IP) and Ryder Systems®, are at risk of getting removed as they have forgone dividend increases in recent quarters. Unless something changes soon, they may soon get stripped of “achiever” status.

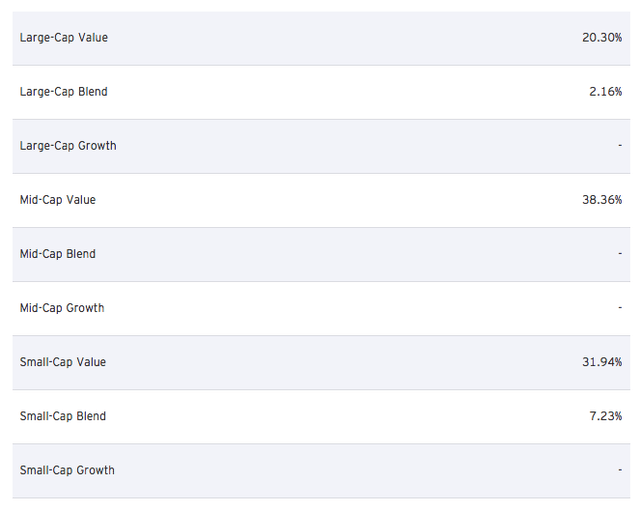

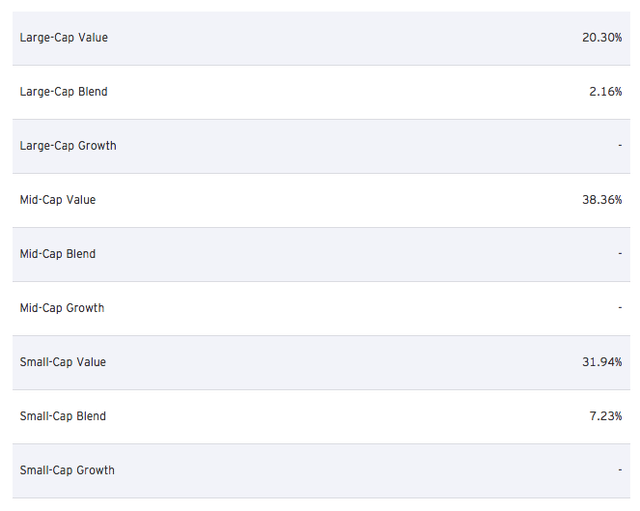

As mentioned earlier, there is nary a hint of growth to be found. Only 10% of the portfolio even qualifies as a “blend”, so this is almost entirely a value fund.

Morningstar categorizes PEY as a mid-cap value fund, which technically it would be if you average things out, but, in reality, it’s an all-cap value fund. The mix of investments across large-, mid- and small-caps is actually an attractive feature given that the economic recovery trade we’ve seen in recent weeks has led to a powerful rally in smaller company stocks.

The fundamentals of the portfolio, however, suggest this isn’t just a value fund. It’s a deep value fund.

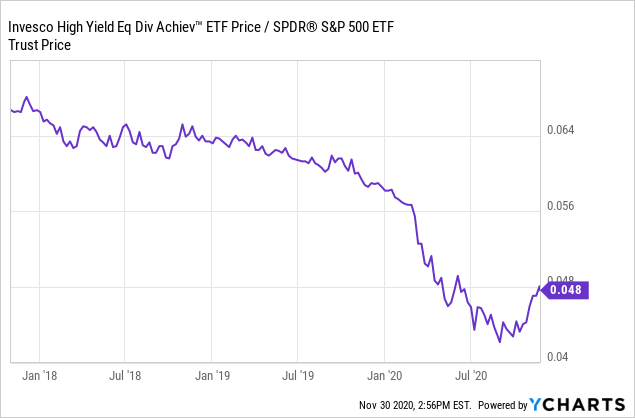

A U.S. stock portfolio with a forward P/E of just 12 is about as cheap as you’ll find unless you start digging around in pure turnaround plays. When you see P/E ratios this low, you should be a bit skeptical. There’s a chance that some of these stocks are cheap because their stock price has taken a dive, earnings are about to be revised downward, the dividend is about to be cut or some combination of all three.

We’ve seen just by looking at the top 10 names that there’s plenty of risk of dividend cuts or freezes. That provides an added element of downside pressure that makes the forward P/E ratio look somewhat less attractive.

Dividend Yield And Performance

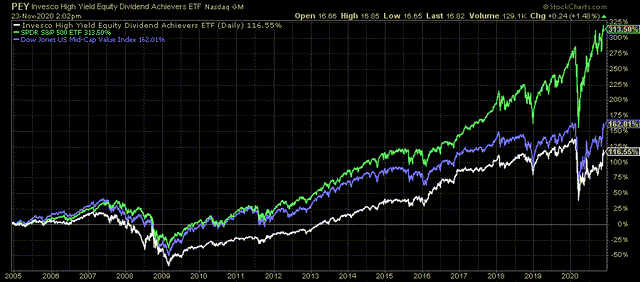

While the fund’s current positioning makes it relatively attractive given the current economic backdrop, it can’t be ignored that PEY is a long-term underperformer.

The fund has significantly underperformed the U.S. Mid-Cap Value Index since its inception and has badly lagged the S&P 500 (SPY). PEY was hit hard during the financial crisis when it’s high allocation to bank stocks got hammered and has trailed ever since. The subsequent growth stock rally throughout the 2010s did not play into PEY’s hands and it’s been unable to stage a notable rally.

Whether a post-COVID economic rebound is the magic elixir that turns PEY into an outperformer again remains to be seen, but early evidence suggests it could be.

High yield dividend payers, which tend to be overweight in financials and other cyclicals, have rebounded strongly in November, an indication that the fund could do very well if these conditions continue in 2021.

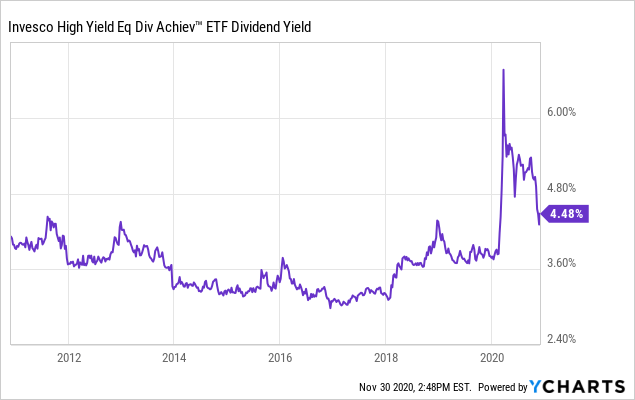

In the meantime, investors can enjoy a 4.5% dividend yield.

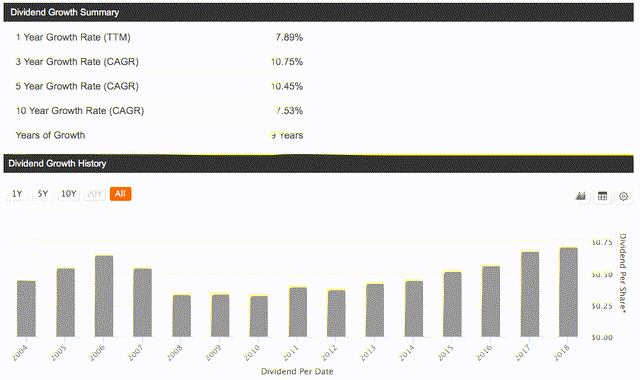

That number is on the higher end of where it’s been historically, so there is some extra value here at the moment. Given that PEY itself has consistently grown its annual dividend for nearly a decade, the above average yield could be interpreted that the share price may have some catching up to do relative its expected dividend payments.

The total 2020 dividend for PEY may end up coming in slightly below that of 2019 given some of the dividend suspensions and cuts, but even in this COVID-impacted economy, this fund is mostly targeting the companies that have the financial ability to continue rewarding shareholders going forward.

Conclusion

Long dividend growth streaks mean less today than they have in years past, so one shouldn’t assume that this portfolio is exempt from dividend cut risk. In fact, a simple look at the fund’s top 10 holdings shows that there’s actually a fair amount of risk in this portfolio.

The fact that PEY yield-weights the portfolio’s components tends to push the higher risk names up the top holdings list. There’s likely some portfolio shuffling coming up over the next several months as some of those stocks with cuts or suspensions get shaken out of the portfolio.

The big question now is most of the dividend cut risk behind us. I think it is. We could still see a cut or suspension here or there, but the most significant risk, I believe, is already baked in.

While the portfolio is positioned well to take advantage of the current climate, it needs an economic rebound to take place in order for the narrative to play out. If we dip into another recession, a COVID vaccine takes longer than expected to be widely produced or business restrictions begin impacting employment, corporate revenues, etc., this cyclical-heavy portfolio could become a laggard again.

At this point, I’m betting on an economic recovery throughout 2021 and think PEY is an ideal dividend ETF to play it.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.