Say you built your portfolio with care. You put in the time and energy to learn the basics and then proceeded to discuss your investment objectives with your spouse, decide on a good asset allocation, and consult with advisors to build a good diversified portfolio of stocks, bonds, funds and more. You left no stone unturned and did everything you could to make sure your financial future is secure.

And then it turns out – your timing was wrong.

You took positions in solid companies but are now getting crushed in the market. What do you do? Should you sell everything and get out? That would be a classic “greed buy and fear sell.” Or do you buy more of what you own at lower prices, in order to bring down your average cost? Or maybe, if you have the experience, start short selling so that you gain from the downtrend?

Why Inverse ETFs?

Another option is inverse ETFs. Inverse ETFs come in handy as a short-term strategy when you are caught unawares in a market correction. You don’t need a margin account to take a position in an inverse ETF. Since you’re not shorting individual stocks but taking a view on broader market segments, the risk is much lower. It is definitely cheaper and simpler than taking many individual short positions or executing complex derivative strategies (which sophisticated investors generally use to protect themselves in a bear phase).

Inverse ETFs are especially useful for portfolio managers who want to hedge against short-term market risk without dismantling and reconstructing their portfolio. It’s not just capital gains that they need to think about. First, it is very expensive to change the asset and security allocation of your portfolio. Each move costs time and money. Secondly, what if they don’t want to sell the stocks they own? If a company is ready to dominate its sector or likely to pay solid dividends for the next five years, it doesn’t make sense to sell it just because it’s hit a speedbump. Like leveraged ETFs, there are leveraged inverse ETFs, too. So if you have a high risk appetite and are fairly confident of a downturn (say in a particular sector), you can always make use of that.

Beware of the "Choppy" Market

It’s obvious that if you are wrong in your assessment (or too late to enter the bear phase), you will lose money. If you got yourself a 2x inverse ETF, you will lose two times more money. However, an often ignored factor is that of a choppy or volatile market.

In short, inverse ETFs don’t work in volatile market situations. Here’s why:

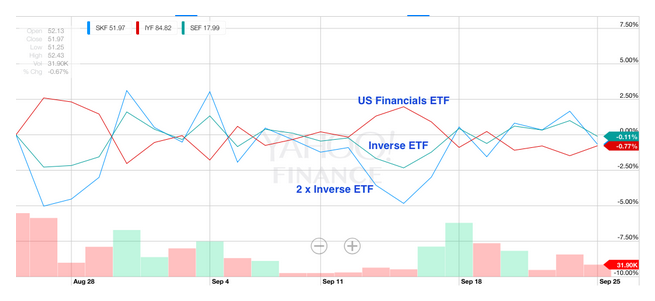

The below is a comparison between an ETF that tracks the Dow Jones U.S. Financials Index (IYF ), an ETF that tracks the inverse (SEF ), and an ETF that tracks 2x the inverse (SKF ). Since financial stocks have been choppy in the last month, there is barely any difference of return between the three.

Even worse would be an “evenly” volatile market. Say an index tracks the following for four consecutive days: -10%, +10%, -10%, +10%.

- The normal ETF would return 0.9 * 1.1 * 0.9 * 1.1 = 0.98 (or a loss of approximately 2%).

- A negative ETF would return 1.1* 0.9 * 1.1 * 0.9 = 0.98 (or a loss of approximately 2%).

- A 2x negative ETF would return 1.2* 0.8 * 1.2 * 0.8 = 0.92 (or a loss of approximately 8%).

So if the market has been evenly choppy, a 2x inverse ETF would end up losing way more than a normal or a negative ETF.

The Bottom Line

There are a few key takeaways to keep in mind regarding inverse ETFs.

Inverse ETFs should be used in the short term and not as a long-term strategy. Actually, any strategy with a bearish outlook is typically bad for the long term because markets tend to move in a positive direction over longer time frames. Further, since it’s more of a “tactical day-to-day maneuver” than a strategy, an inverse ETF position requires more time to get in and get out of positions quickly. If you don’t have time to watch and react, it is better not to try out inverse ETFs.

Another important point is that returns are not exactly a 1% gain on a 1% downturn. There are commissions (the usual) and management fees involved. And the management fees of inverse ETFs are higher than normal ETFs.

Finally, there are also inverse fixed-income ETFs (e.g. ProShares UltraShort 20+ Year Treasury (TBT ) in addition to regular inverse equity ETFs. These can help you protect yourself against interest changes.

For more information, check out The Impact of Rising Interest Rates on Your Fixed-Income Fund.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net