Since their introduction in 2006, leveraged ETFs have attracted tens of billions of dollars in cash inflows and become immensely popular among investors looking to accomplish a variety of objectives. As scrutiny of these products has intensified, the conception that leveraged ETFs are overly-complex products beyond the grasp of most investors has spread.

While many of the intricacies surrounding leveraged ETFs are far from simple, the underpinnings and mechanics of these products are actually quite simple.

Under The Hood

Most leveraged ETFs are designed to deliver a multiple (such as 2x or -3x) of their under underlying on a daily basis (before fees and expenses, of course). There are a number of ways for leveraged ETFs to achieve the amount of exposure necessary to deliver these returns. While the exact blend of securities used may vary from fund to fund, most of these products use various derivatives to accomplish the states objectives.

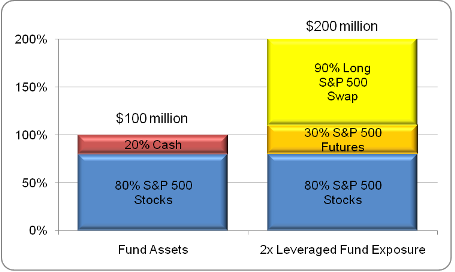

For example, a 2x long S&P 500 ETF may use a combination of equities, futures, and swaps to essentially double its exposure. A fund with $100 million in assets might invest $80 million in the underlying assets of the underlying benchmark (in this case the S&P 500), leaving $20 million in cash. A portion of this cash could be used to purchase S&P 500 futures contracts — exchange-traded derivatives that provided exposure to a benchmark without direct ownership.

A futures contract is essentially a standardized contract between two parties that agree to buy (and sell) an underlying index at a future date at the market price. The buyer of a contract has a long position in the underlying, while the seller has a short position. A portion of the cash held by the fund could be used as collateral for the futures position.

See also: The Curious Case Of Leveraged ETFs: Understanding How Compounding Works.

In addition, a leveraged ETF may enter into an index swap agreement with a counterparty to increase its exposure to the underlying index. Swaps are customized agreements between two counterparties to exchange two sets of cash flows over a specified period of time. In an equity index swap, one party generally pays cash equal to the total return on the underlying index, while the other pays a floating interest rate.

By investing in a combination of these assets, a 2x leveraged ETF can establish $200 million of exposure with $100 million in assets:

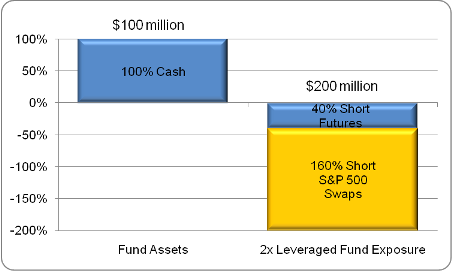

The process for constructing a -2x leveraged ETF has some similarities. Because such a fund would be designed to deliver exposure equivalent to a multiple of the inverse return on a benchmark, it could keep a significant portion of its assets in cash, which would be used as collateral for futures and swaps contracts that would increase in value if the related benchmark declined:

Rebalancing Process

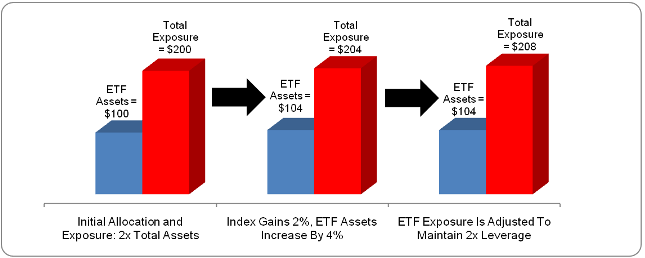

Much of the confusion over leveraged ETFs relates to the rebalancing process. In order to deliver results that correspond to the indicated multiple of daily returns on an underlying index, leveraged ETFs must rebalance their holdings on a daily basis. Consider a hypothetical 2x long leveraged ETF with $100 million in assets that achieved $200 worth of exposure through the processes described above.

See also: Why Everything You’ve Heard About Leveraged ETFs Is Wrong.

If the underlying index increased by 2%, total fund assets would increase by approximately $4, or 4%. At the beginning of the next day, the leveraged ETF would have $104 in assets, and as such would need to achieve $208 worth of exposure. There are a number of ways for the fund to do this, most of which involve the use of various derivative products.

It is this rebalancing process that creates the potential for divergent results if leveraged funds are held for multiple trading sessions. Because long leveraged ETFs increase exposure after a gain and decrease exposure after a loss, a seesawing market can result in return erosion, since leveraged ETFs would effectively be increasing exposure ahead of a losing session and decreasing exposure ahead of a winning session.

Disclosure: No positions at time of writing.