Puerto Rico’s default has put pressure on a number of high-yield municipal bond exchange-traded funds that hold positions in the island commonwealth, but the selling pressure may end up creating a unique buying opportunity for value investors.

Many high-yield muni bond ETFs have exposure to Puerto Rico – after all, the territory is offering high yields – but the amount of exposure varies greatly between funds. In some cases, closed-end funds have completely divested Puerto Rico bonds from their portfolios, which means they no longer have any exposure to the risks, but still suffer from the broader aggregate capital outflows from the asset class due in part to the island’s crisis.

Some of the most popular ETFs with exposure include (as of 8/7/2015):

| Ticker Symbol | Exposure | 6-Mo. Performance | 12-Mo. Yield |

|---|---|---|---|

| Market Vectors High Yield Municipal Index ETF (HYD ) | 2.90% | -3.36% | 4.91% |

| SPDR Nuveen S&P High Yield Municipal Bond ETF (HYMB ) | 8.80% | -4.80% | 4.57% |

| Market Vectors Short High-Yield Municipal Index ETF (SHYD ) | 5.10% | -2.31% | 3.19% |

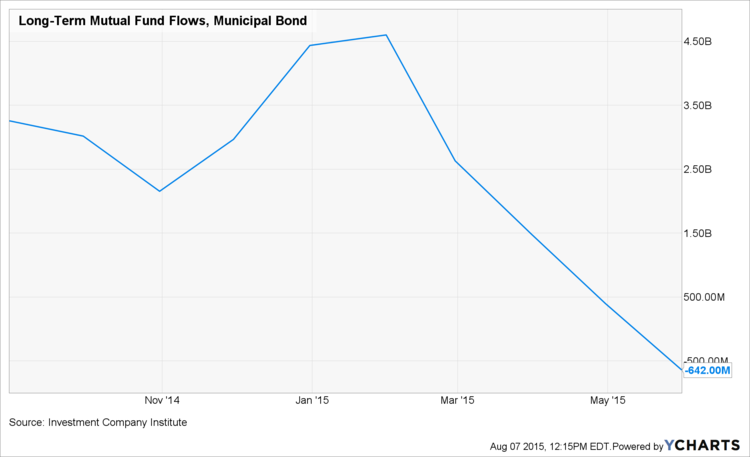

High-yield muni bonds have also been suffering from the anticipated Federal Reserve rate hike later this year, which promises to increase bond yields and lower bond prices. These dynamics have taken a toll on many bond and bond funds in general, although mixed economic data has some analysts predicting that a rate hike may not happen until next year. Of course, that hasn’t stopped mutual fund outflows from taking a toll on muni bond prices (see Figure 1. below).

So, why consider high-yield muni bonds at all?

High-yield muni bonds have some of the highest yields in the world, particularly for investors capable of realizing their tax benefits, while maintaining much lower default rates than comparably rated corporates. According to Morningstar, high-yield muni funds have average yields of between 4% and 5% – an impressive feat with 10-year Treasuries at 2.6% – but investors in the top income bracket could be receiving equivalent yields upwards of 7%.

Unlike corporate issuers, high-yield muni bonds won’t suffer as much from the monetary policy-related impact of higher interest rates, or from the impact of lower commodity prices. The Puerto Rico crisis may have a limited impact on some fund portfolios, but most funds are well-diversified and others have already divested their holdings in the island. But even then the impact will only be felt if there’s a full default at all – some politicians are hoping otherwise.

Finally, muni bond prices have taken a beating over the past year due to these concerns, which could mean that many of the risks are already priced in to the asset class – at least to some extent – creating the potential for yield and price appreciation.

That said, investors should still be very cognizant of the risks associated with investing in high-yield muni bonds and funds. There’s little doubt that a Puerto Rico default would negatively impact prices in the near-term, if it materializes, while higher interest rates are universally a negative for the entire fixed income space. While bonds in general may not be all that attractive, high-yield muni bonds may be worth considering for those seeking income.

Key Takeaway Points

- High-yield muni bonds – and funds – have moved significantly lower over the past year amid concerns of Puerto Rico’s default and an interest rate hike.

- The two major risk factors affecting prices remain uncertain to some extent, which means that investors may have overreacted.

- High-yield muni bonds provide some of the highest yields in the world right now, while maintaining better credit quality than corporate or emerging market alternatives.

Disclosure: No positions at time of writing.