ETFdb.com analyzes the search patterns of our visitors each week. By sharing these trends with our readers, we hope to provide insights into what the financial world is concerned about and how to position your portfolio.

This week investors have been surprised by Theresa May’s strong suggestion that her government will focus on immigration rather than business interests in the upcoming Brexit talks, negatively impacting the British pound. Elsewhere on the list, semiconductors have been boosted by Apple’s newly launched iPhone 7, while OPEC’s surprising production freeze underpinned oil prices. Finally, Amazon garnered interest for its market consolidation move, and Deutsche Bank’s woes directed attention to the Financials sector.

British Pound: May’s Anti-Immigration Message Sparks Sell-off

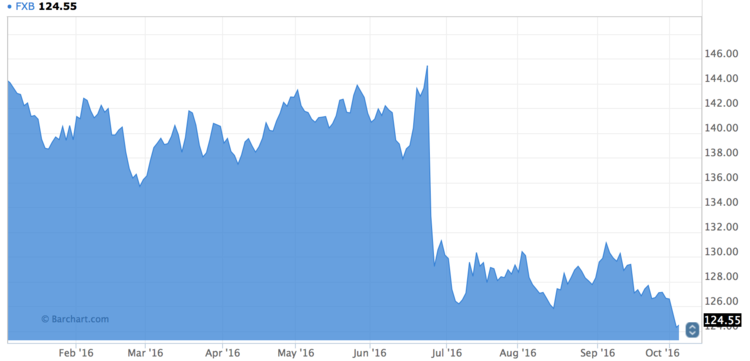

U.K. Prime Minister Theresa May strongly suggested in a recent speech that her government will push for a so-called hard Brexit, sending the British pound to 31-year lows and sparking our readers’ interest. Traffic for the currency surged as much as 413% over the past week, as bewildered investors watched May’s speech in dismay. Guggenheim’s British Pound Sterling Trust (FXB ) dropped more than 2% since last Thursday until Wednesday’s close, extending year-to-date losses to a staggering 13.7%.

May’s stance on Brexit took investors by surprise. She signaled a departure from the small government policies of her predecessor David Cameron, clearly suggesting that immigration will dominate the upcoming negotiations with the European Union. Although May said business interests are paramount to Britain’s success, she downplayed the importance of the banking sector, which is apparently closer than ever to losing its so-called passporting rights when Brexit completes. May seemingly has taken a broader message from the referendum and looks set to change course from a business-oriented government to a social one.

The Prime Minister has also been reported to refuse to prioritize financial services’ interests in negotiations with the EU, setting the stage for a more dramatic post-Brexit change than previously thought by investors. Banks were quick to warn on Tuesday that about 70,000 jobs and $13 billion in taxes were at risk, if they aren’t able to sell their services across the European Union. But that message is unlikely to sway a strikingly decisive May.

Semiconductors: Thanks iPhone 7

Semiconductor ETFs have seen their traffic surge as much as 70% this week, far behind the British pound. Semiconductor companies are in great demand from investors at the moment. For example, VanEck Vectors Semiconductor (SMH ) jumped about 2.6% since last Thursday, extending year-to-date gains to as much as 30%.

Semiconductor stocks have been boosted following reports by Apple (AAPL) that pre-orders for its latest product – iPhone 7 – were strong. Cirrus Logic (CRUS) and Skyworks Solutions (SWKS), both Apple suppliers, were among the best performers.

However, many stocks, including blue-chips such as Intel (INTC), have been getting a lot of interest from short sellers lately, suggesting the sector is overheating.

Oil and Gas: OPEC Lends a Hand to U.S. Fracking Rivals

OPEC’s surprising production cut agreement has enticed readers towards the oil and gas sector, which posted a rise in traffic of 68%. Although it was surely not intended, OPEC seems to have given a much-needed lifeline to distressed U.S. shale companies, as the subsequent rise in oil prices could give U.S. producers more confidence and make them a touch more aggressive than they had planned.

A rise in rig efficiency and an unexpected $60 per barrel could embolden investors who have stayed away from oil and gas companies to finally get in the market. Those wanting to partake in a revival of the industry have SPDR S&P Oil & Gas Exploration & Production ETF (XOP ) as a primary option. The ETF has risen nearly 4% over the past five days, and is up 29% since the beginning of the year.

With OPEC seemingly prepared to take action, many shale plays that have become unprofitable during this bearish period will once again be open for business, leading to a corresponding bump in U.S. output.

Amazon Prime Gets Boosted

The introduction of Prime Reading aroused interest in Amazon (AMZN), as traffic increased by 60% over the past week. The new service grants access to a plethora of Kindle books, magazines, short works and other top products, all without supplementary cost. And since no Kindle is required, Prime membership is expected to spike, thus consolidating Amazon’s positions in the face of competitors like Alphabet (GOOG).

Analysts hiked the stock’s price target, citing strong growth for Amazon Prime loyalty service as well as compelling growth in net income, robust revenue growth and expanding profit margins. Amazon continuously tries to add features to incentivize new Prime subscribers. Growth in Prime membership is key for the company, as analysts’ surveys have also found that Prime members tend to spend far more on the platform than non-subscribers. To this end, Consumer Discretionary Select Sector SPDR Fund (XLY ) is an option to play the upcoming improvement in Amazon’s balance sheet. Despite a low 3.2% year-to-date performance, Consumer Discretionary Select offers exposure to a sector that is set to regain investor appeal.

Financials: Fears of Contagion Escalate

Investors seeking clues as to whether Deutsche Bank’s troubles will spread contagion toward U.S. financials have sparked a 57% rise in viewership week-over-week. Both the European Central Bank and Bank of Japan are firmly planted at the dovish end of the policy spectrum, sporting negative rates and pursuing large-scale asset purchase programs. These policies hurt bank profitability and have largely failed so far to boost their respective economies and get inflation off the zero bound.

However, the German lender’s struggle seems contained to Europe. Although acknowledged as a net contributor to systemic risk to the global financial system, it is not clear at the moment whether Deutsche Bank is actually in such a distressed situation as to pose a real threat to financial markets. Investors are thus advised to keep a close eye on the bank’s credit default swaps’ movements, as well as future developments regarding the recently disclosed U.S. Department of Justice investigation into mortgage-backed securities misselling.

Investors seeking a targeted exposure to the U.S. Financials sector have the Vanguard Financials (VFH ) at hand. With around 500 individual securities in the underlying portfolio and about 25% exposure to real estate, Vanguard Financials is the go-to option for investing in the banking sector through a risk-adjusted strategy.

The Bottom Line

The British pound garnered the most attention from our readers, as it continued its downward spiral following Prime Minister Theresa May’s hardline remarks on immigration. Semiconductors have been in the spotlight for their surprising ascent lately, but the performance attracted short sellers. Amazon has continued to grow and consolidate its business, while the oil and gas sector has gotten an unexpected boost from OPEC, which agreed to a production cut. Finally, Financials has been on investors’ minds for fears Deutsche Bank’s issues may spread contagion.

By analyzing how you, our valued readers, search our property each week, we hope to uncover important trends that will help you understand how the market is behaving so you can fine-tune your investment strategy. At the end of the week, we’ll share these trends, giving you better insight into the relevant market events that will allow you to make more valuable decisions for your portfolio.