After a dismal 2022, financial markets began the new year on a more positive note. U.S. stocks and bonds advanced during the first quarter, joining most other major asset classes firmly in the green. While markets bounced back following a historically ugly year, the past three months were anything but uneventful. Bank runs, Fed rate hikes, stubborn inflation, and an uncertain future path for the economy took turns dominating the headlines.

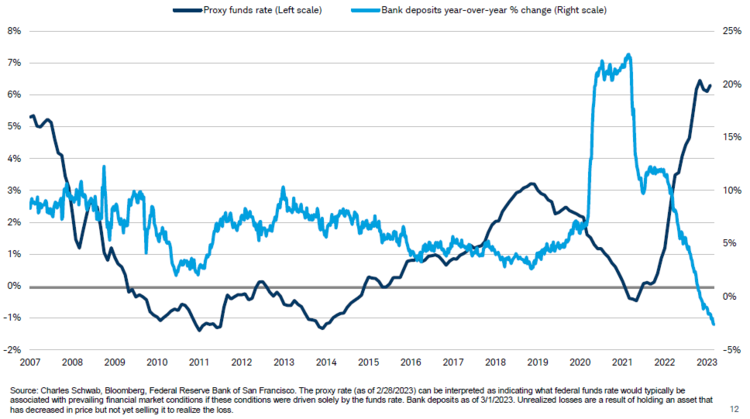

The recent “banking crisis” stirred the most drama during the quarter, as echoes of 2008’s global financial crisis spooked investors. Silicon Valley Bank collapsed in early March and was quickly followed by the failure of other regional banks, including Signature and Silvergate. The short-lived crisis hit a crescendo with the collapse of long-troubled global bank, Credit Suisse. There are nuances to the downfall of each, but the roots of their issues can be traced back to Federal Reserve and government policies over the past several years. The massive monetary and fiscal response to the pandemic resulted in an influx of cash deposits into banks. In an effort to squeeze out profits in a low interest rate environment, some banks invested large chunks of those deposits into longer-dated Treasuries and government agency bonds. As the Fed hiked interest rates over the past year in a battle against stubbornly high inflation, both the deposit and loan side of bank balance sheets were negatively impacted. How?

We previously described why the Fed is hiking rates:

“Higher interest rates impact everything from mortgages to auto loans to credit cards. Increased rates also make financing more expensive for businesses, who borrow money to pay for daily operations and invest in longer-term projects. All of this can have the effect of slowing the economy since consumers and businesses spend less when faced with higher rates. A reduction in consumer and business spending theoretically helps reduce inflation, since there is less demand for goods and services. Less demand puts downward pressure on prices, the Fed’s ultimate goal.”

A combination of higher interest rates and inflation has pressured both businesses and consumers over the past year, resulting in a greater need for cash. Businesses and consumers have tapped their money held at banks, resulting in deposit outflows. Meanwhile, bonds purchased by banks were bludgeoned by higher interest rates. As rates go up, bond prices go down – as most investors cruelly witnessed first-hand last year.

Without getting into the weeds, banks operate using a “fractional reserve” system. Very simply, this means that banks only keep a small percentage of cash on hand to meet deposit withdrawals. The remainder is loaned out (mortgages, auto loans, business loans, etc.) or invested in portfolios of bonds and other securities. By now, the problem should be clear.

Deposit outflows combined with substantial losses on bond portfolios is a bad combination for banks, especially when depositors start asking for their money back at the same time. It should also be noted that deposit outflows have accelerated due to banks paying peanuts on those deposits. The current national average savings account yield is 0.24%. The national average 1-year CD rate is 1.49%. Meanwhile, a 1-year Treasury bond yields 4.61%. Some depositors have questioned the merits of keeping extra money at a bank earning next to nothing versus earning 4-5% in Treasuries. So, what do those depositors do? They pull their money out of banks and move it to higher yielding investments.

Most banks are perfectly capable of handling this liquidity uncertainty without issue. However, banks with a certain type of depositor profile (in the case of Silicon Valley Bank, tech/crypto-related businesses that faced significant challenges over the past year and needed cash) and portfolios stuffed with longer-duration bonds (thanks to poor risk management by bank executives) have come under pressure. Add to that, depositors seeking a higher return on their cash and you have a recipe for a small “banking crisis”. That said, the vast majority of banks – and particularly the largest banks – remain well-capitalized and we do not view this recent episode as a repeat of 2008.

What About the Fed?

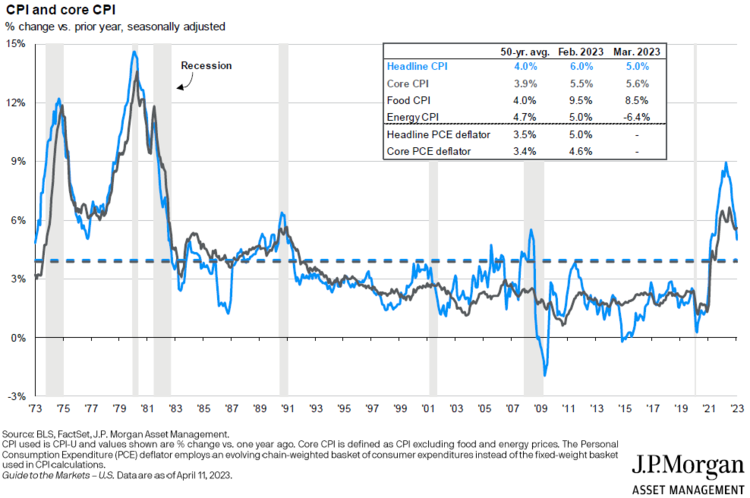

While the Fed’s aggressive rate hiking campaign has caused heartburn for some banks, the more important question moving forward centers on how these rate hikes will affect the broader economy. The Fed increased rates by 0.25% twice during the quarter, despite weaker economic data. The Fed desperately wants to bring inflation under control and has messaged that they remain committed to doing so even if there is some economic collateral damage. While inflation has cooled somewhat, prices remain elevated.

In a nutshell, the Fed is attempting to kill inflation without killing the economy. They’re attempting to orchestrate what’s referred to as a “soft landing”, essentially bringing inflation under control without tipping the economy into recession. We noted last quarter the single biggest question for financial markets in 2023 is whether the Fed could pull off this “soft landing” or if they instead would clumsily maneuver a “hard landing” (a sharper economic downturn). Nothing we’ve witnessed so far this year has changed our view regarding the importance of the Fed’s policies to the overall health of the markets. If the Fed is too aggressive in their battle against inflation, that could lead to a harder landing. If the Fed is too soft, they might struggle to bring inflation back under control.

So, What Does This Mean for Investor Portfolios?

On the stock side of the equation, our focus is squarely on corporate earnings. If the Fed is overly aggressive and the economy enters a recession, that will negatively impact earnings and likely stock prices. If the Fed is able to thread the needle, corporate earnings could show some resiliency and stocks should remain buoyant. Again, as we noted last quarter, valuations are not exactly cheap, which means corporate profits will need to do the heavy lifting to continue propelling stocks forward over the shorter-term:

“Perhaps the biggest factor in the shorter-term is the earnings component of the price-to-earnings ratio. Companies are grappling with higher labor and input costs. Consumers are struggling with resultant higher prices, which could ultimately curtail spending and negatively impact corporate revenue and earnings. This is a classic negative feedback loop that is leading to increased “recession” talk, particularly given the recent acceleration of corporate layoffs.”

On the bond side, as we noted earlier, investors can now obtain 4-5% yields risk free. That’s a much-welcomed change after years of hardly any income. Bonds are now providing real portfolio value, finally pulling their weight after free-loading on declining interest rates for the better part of a decade.

Longer-term, we continue to view stocks as highly effective wealth generators and bonds as excellent diversifiers (especially now that you’re paid to hold them). Markets are never really “normal”, but today’s environment is much more normalized than we’ve experienced in the recent past. Things like corporate earnings and risk-free yields actually matter again. While there is a lot of market noise and headlines right now – regional banks, the Fed, inflation, etc. – good, old-fashioned fundamentals are once again taking center stage. We view that as a longer-term positive and remain committed to taking a longer-term approach to investment management – typically the best recipe for success.

For more news, information, and analysis, visit VettaFi | ETFDB.