Thought to ponder…

“Because of the spirit, I say. Because of the heart. Writing and reading decrease our sense of isolation. They deepen and widen and expand our sense of life: they feed the soul.”

- Anne Lamott, Bird by Bird

The View from 30,000 feet

Thursday marked the final trading day of the week, month and quarter. It seemed only fitting the two major data releases on Thursday delivered the overarching message of 2024 – better than expected growth, mixed with a downshift in the disinflationary trends of last year. On Thursday, Q4 2023 GDP was revised higher and Q4 2023 GDI was released, showing a catch up between GDI and GDP, that squashed the dreams of many a bear. Earlier in the week the Atlanta Fed GDPNow was also revised higher, now projecting Q1 2024 grew at a 2.3% annualized rate. Strategists have been scrambling all quarter to upgrade their GDP and equity market forecasts for 2024, but still look behind the ball, as the both the economy and the equity markets continue to surprise on the upside.

Thursday’s PCE release was inline with expectations showing that the disinflationary trends related to Goods disinflation in 2023 are running out of steam, and it will now be up to housing, wages and the service sector to finish the disinflationary story in the coming year. Last week’s message from the Fed highlighted two camps that are forming within the Fed – The Powell Camp and The Waller Camp. Powell, restated his case last week that he believes the disinflationary trends will persist, although along a bumpy path. Waller, showed another side of the Fed, one that is concerned that disinflationary trends will stall in the coming year. What this means for interest rates this year is the difference between three rate cuts, or as few as zero rate cuts. What this means for equities, however, may be subtle. Either way growth wins, either by virtue of being goosed by lower rates, or by being driven by spending.

Although the path for the remainder of the year will not be linear, there are few negative catalysts showing their faces.

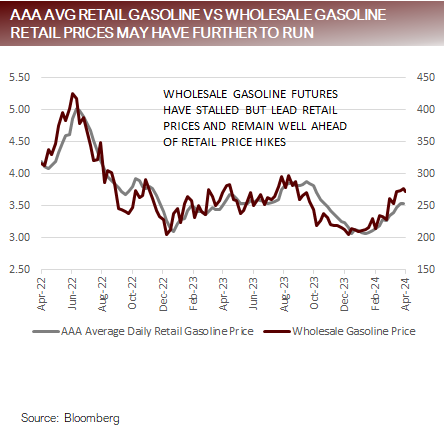

PCE highlighted the disinflationary handoff that needs to happen between goods and services

PCE Core Service Less Housing still supports friendly Fed; gasoline has wildcard potential

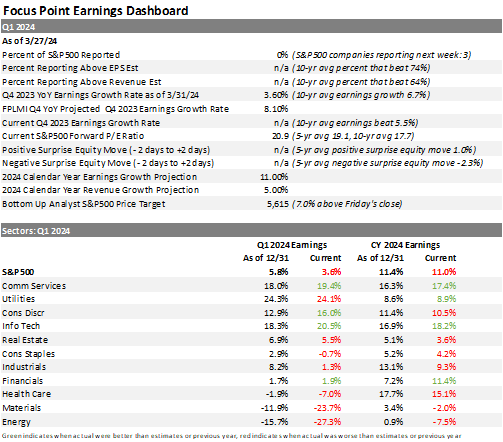

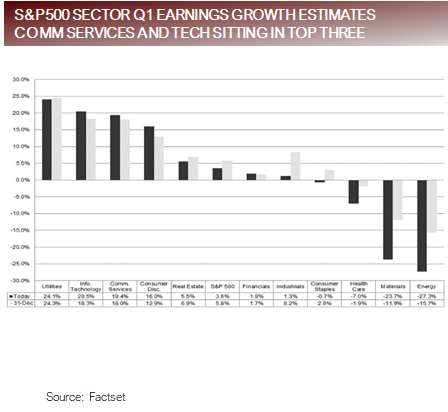

Preview of Q1 2024 earnings season

The rally has broadened out but earnings growth still concentrated Comm and Tech

The Focus Point Leading Market Indicator ticks slightly higher

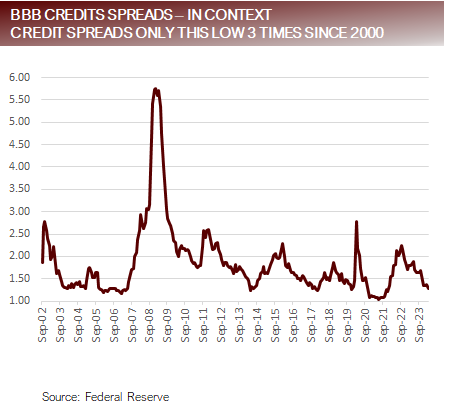

Strains in corporate Balance Sheets, and market liquidity not visible in recent data

FAQ: Do higher interest rates matter to the economy?

Terming out debt and deficit spending have been big contributors to easing impact of rates

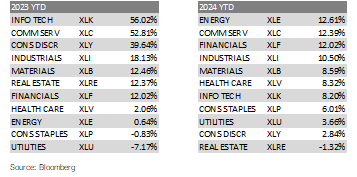

Focus Point Sector Rotation Update

Putting it all together

For more information, please visit VettaFi.com | ETF Trends.