Like many analysts and investors, I’m always searching for the next big idea—whether it’s a new company that creates a path to a whole new industry, an innovative ETF, or a new megatrend. I’m still an advocate of crypto, artificial intelligence, and other disruptive technologies, but sometimes good investment ideas aren’t always obscure. This week I’m looking at the aerospace and defense industry. As part of the industrial sector, the aerospace and defense industry often flies under-the-radar (pun intended) unless there is news of geopolitical conflict and tension. As an industry that is less sensitive to economic cycles, the defense industry can be a good option for investors looking to diversify their holdings while seeking relatively stable performance and growth opportunities beyond mega-cap tech.

Industry drivers are particularly important during an election year

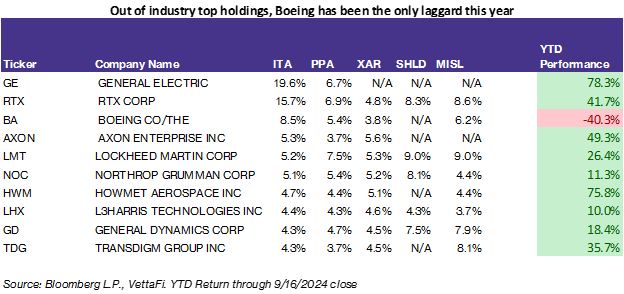

Aerospace and defense companies often receive more investor interest during times of geopolitical conflict due to increase demand in defense systems. We’ve had no shortage of conflicts this year with continued tension in the Middle East and Ukraine, among other areas. But what makes the industry attractive to many investors is that defense companies tend to be less cyclical due to their dependence on long-term sales contracts with the government. RTX Corp (RTX), for instance, derived 46% of its total net sales to the U.S. government last year. Lockheed Martin (LMT), saw 73% of last year’s net sales from the U.S. government (including 64% from the Department of Defense).

Government contracts have their own risks—relationships can be lost, terms of contracts can be less contractor friendly (e.g., fixed price contracts), and contract renewals are dependent on the overall government budget. According to the U.S. Department of Defense, defense spending is around 3% of U.S. GDP—which is near its record low. The year-over-year amount, however, has still increased. This year, the budget increase request was 4.1%, and defense spending continues to be a hot topic in bipartisan legislation (and very important for an election year).

Price performance and net inflows (mostly) soar

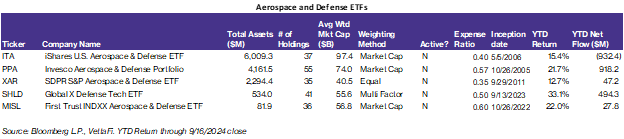

Excluding leveraged ETFs, there are five ETFs in this sector: the iShares U.S. Aerospace & Defense ETF (ITA ), the Invesco Aerospace & Defense Portfolio (PPA ), the SPDR S&P Aerospace & Defense ETF (XAR ), the Global X Defense Tech ETF (SHLD ), and the First Trust INDXX Aerospace & Defense ETF (MISL ). Most of these ETFs received positive net inflows this year. Interestingly, ITA saw around $900 million in net outflows this year, while the next largest ETF PPA received around the same amount of inflows.

Some of the outflows from ITA could be explained due to its large allocation in Boeing (BA) compared to its peers, which has fallen close to 40% this year due to a wide range of issues from faulty jets to worker strikes. But Boeing is an outlier and overall aerospace and defense companies have performed well, which has driven price performance of these ETFs. YTD all aerospace and defense ETFs saw double digit gains thanks to large allocations to companies like General Electric (GE), Howmet Aerospace (HWM), Axon Enterprise (AXON), RTX Corp, and Lockheed Martin Corp.

While these ETFs all share similarities, there are a few key differences:

- The iShares U.S. Aerospace & Defense ETF (ITA): This ETF is currently the largest aerospace and defense ETF with over $6 billion in assets. ITA focuses on U.S. companies that manufacture commercial and military aircrafts and other defense equipment. It follows an index with a straightforward methodology—constituents are chosen from a universe based on the aerospace and defense subsectors and are eligible if they have a fair market capitalization of at least $500 million. These constituents are then market cap weighted (with an individual cap of 22.5%).

- The Invesco Aerospace & Defense Portfolio (PPA): This is the oldest ETF in the sector (but only six months older than ITA). It consists of companies involved in development, manufacturing, operations and support of U.S. defense, homeland security, and aerospace operations. The index uses a proprietary weighting methodology called TrueCap which reduces overweighting of diversified companies—in this case General Electric (GE), which is almost 20% of ITA is only around 7% of PPA. While PPA has just over $4 billion in net assets, this fund has seen over $900 million in net inflows YTD.

- The SPDR S&P Aerospace & Defense ETF (XAR): This is another ETF with a relatively straightforward selection process based on industry classification. Unlike its peers, XAR uses an modified equal-weight methodology. This methodology has reduced the recent negative impact from Boeing, while offering greater exposure to small-cap components.

- The Global X Defense Tech ETF (SHLD): Unlike its peers, SHLD does not include commercial aerospace exposure. The ETF focuses on pure-play defense technology, cybersecurity, and advanced military systems. While many of its top holdings are similar to other ETFs, SHLD has a large exposure to Palantir Technologies (PLTR)—which was up 112% YTD. This ETF also has exposure to international names like Bae Systems (BA LN), Rheinmetall AG (RHM GR), and Thales SA (HO FP), while the other ETFs all focus on U.S. stocks.

- The First Trust INDXX Aerospace & Defense ETF (MISL): This ETF takes an updated view on the industry and includes traditional aerospace and defense companies in addition to “advanced aerospace and defense” like space technologies, air mobility, and cybersecurity. Unique holdings include AST Spacemobile (ASTS) and Intuitive Machines (LUNR). This ETF is also the smallest and most expensive of the group.

For more news, information, and analysis, visit VettaFi | ETFDB.