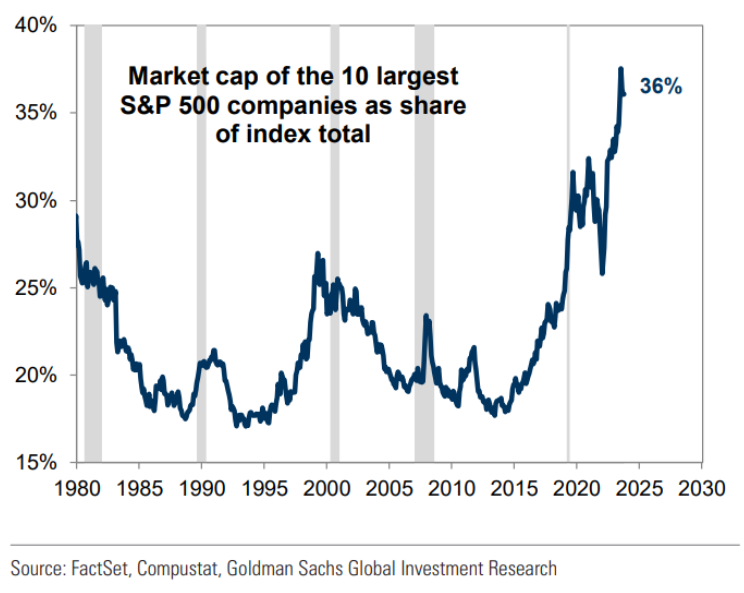

Earnings season is in full swing, and five of the “Magnificent 7” are reporting quarterly results this week. Wall Street has been steadily raising the alarm on mega-cap concentration risks, and recent notes out from Goldman Sachs and Vanguard have cranked up the hazard level a notch. Citing the worst equity market concentration in roughly 100 years, Goldman is now projecting a mere 3% nominal return for the cap-weighted S&P 500 over the next 10 years. This equates to just a 1% real return. Excluding the concentration variable, the annualized return would rise to 7%.

Vanguard expressed a similarly lackluster view on equity returns over the next decade, to the tune of 3-5% — well below the 13% average gain the market has experienced over the last 10 years and well below average analyst estimates of 6–7%. Such predictions raise questions about the appeal of stocks compared to risk-free 10-year Treasury yields, which exceed 4%. Many investors are now looking to de-risk by dialing down their exposure to the space.

Naturally, such gloomy forecasts have been met with skepticism and challenges from other analysts — who cite powerful bullish factors, such as the transformative impact of artificial intelligence, strong mega-cap business fundamentals, and declining rates as reasons to stand strong on stocks.

Doorways to De-risking

But for investors looking to broaden out beyond the most dominant names, the most popular equal-weighted ETF is the Invesco S&P 500 Equal Weight ETF (RSP ) — the largest and most liquid on the market. The fund is just coming off an all-time high, up 14% year-to-date — with north of $9 billion in net inflows this year ($1.5 billion over the past month alone).

On a performance basis, the Astoria U.S. Equal Weight Quality Kings ETF (ROE ) continues to top the charts — boasting total returns of 19% in 2024 and more than 30% over the past 12 months. ROE actively takes a more quantitative, sector-neutral approach by equal-weighting 100 of the highest-quality mid- and large-cap U.S. companies. The idea is to not sacrifice performance by underrepresenting technology too much, which still makes up a hefty third of the S&P 500. Simply applying an equal-weighted overlay nearly slices that allocation in half.

Other funds, such as the Goldman Sachs Equal Weight U.S. Large Cap Equity ETF (GSEW ) and the ALPS Equal Sector Weight ETF (EQL ), have also done well — up 18% each.

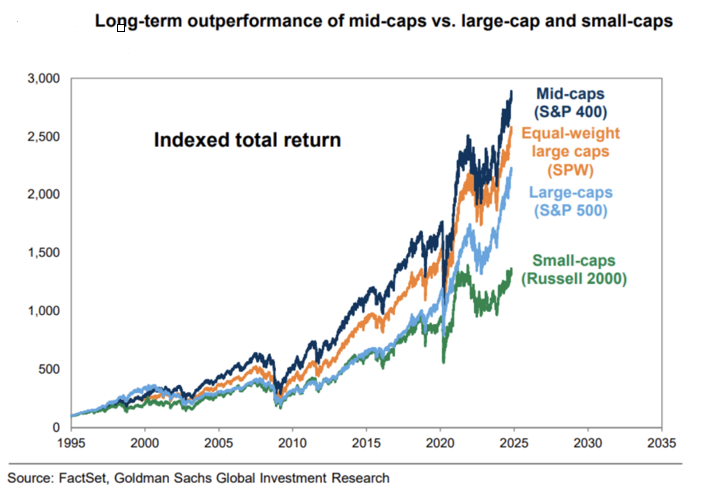

Beyond equal-weighted large caps, small- and mid-caps have also seen revitalized interest — as evidenced by continued strong inflows into the Avantis U.S. Small Cap Value ETF (AVUV ) and the Pacer U.S. Small Cap Cash Cows 100 ETF (CALF ). Mid-caps, in particular, have historically outshone the broader indices. Going back to 1995, the S&P 400 Mid-Cap index has outperformed the equal-weight, plain vanilla S&P 500 and small-cap Russell 2000.

The most popular middle-tier plays this year include the iShares Core S&P Mid-Cap ETF (IJH ) — which has hauled in $5.5 billion in net inflows — as well as the Invesco S&P MidCap Quality ETF (XMHQ ) and Vanguard Mid-Cap ETF (VO ), which have netted nearly $3 billion each.

New Launches Respond to Concentration Risks

Several new entrants have entered the ETF fray in response to these rising concentration risks. BlackRock just launched a suite of large-cap equity ETFs that aim to help investors capture more granular growth among the largest U.S. companies. Included among the recent launches was the iShares Nasdaq-100 ex Top 30 ETF (QNXT ), which strips out the top 30 tech titans and invests in the remaining 70 stocks across technology, health care, consumer goods and industrials.

The Roundhill Magnificent Seven ETF (MAGS ) has enjoyed red-hot returns over the last couple of years, rallying nearly 50% in 2024 and amassing $800 million in assets. But many investors want to diversify beyond seven stocks. Defiance just debuted a new ETF that allows investors to bet on the exact opposite of that — the Large Cap Ex-Magnificent Seven ETF (XMAG ). By stripping out the infamous Mag 7, investors can expect a reverse-funnel effect away from the mega-caps and a more level playing field for broader markets exposure.

Based on near-term momentum, market concentration may or may not be headed to further extremes. However, in the long run, few would dispute that demand for diversification is growing by the day. Many ETFs exist to offer advisors tools to help clients focus less on making targeted bets elsewhere in the markets, and more on navigating around their concerns over current market composition and its sustainability.

For more news, information, and analysis, visit VettaFi | ETFDB.