There has been ample speculation about how ETFs might penetrate the exclusive realm of private assets, but two firms have managed to pull off launching a pair of private credit CLO ETFs in the past week.

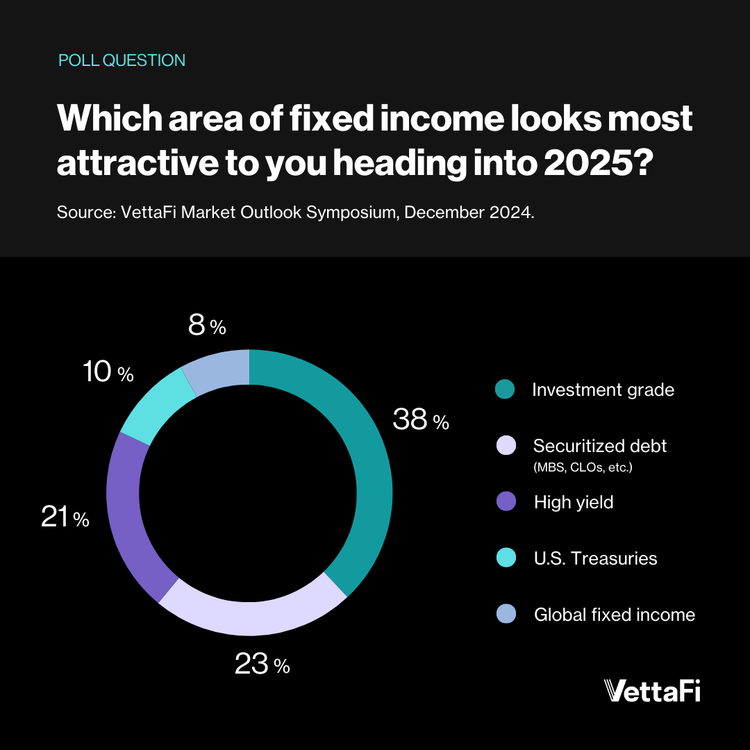

At VettaFi’s Market Outlook Symposium, we asked our live advisor audience which segment of fixed income looked most attractive in the coming 12 months. While most still stuck with investment-grade and high-yield corporate bonds, nearly 30% said securitized debt looked most attractive in 2025.

Historically, CLOs fare well during times of market duress, such as the 2008 Global Financial Crisis (not to be confused with CDOs, the culprits behind the crash). But private credit CLOs have yet to prove their mettle in times of severe market dislocation.

CLO ETFs first emerged in the fall of 2020 and have stormed the scene ever since . They took off in the post-Covid era and rose to reach $19 billion in total assets. That makes the CLO ETF market larger than some of the biggest high yield bond and senior loan ETFs on the market. But the recent private credit rollouts aim to provide access to exclusive markets. These markets are historically reserved for high-net worth individuals and institutional investors.

ETF Pathways to Private Credit

BondBloxx, which focuses solely on providing precision bond ETFs, was first to market with the BondBloxx Private Credit CLO ETF (PCMM ). The fund charges 0.68% and provides exposure to a portfolio of actively managed, private credit, middle market loan CLOs. The higher fee stems from the underlying debt spanning a range of tranches. During VettaFi’s Market Outlook Symposium this week, Joanne Bianco, Investment Strategist at BondBloxx, told me the fund was formed in response to consistent client demand for exposure to private credit CLOs.

“This fund is one of our top picks because we like private credit’s potential for compelling yield and total return performance, all with the low volatility that it provides,” she said.

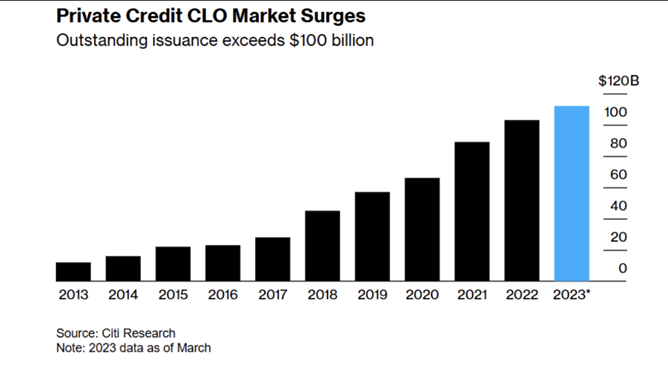

The global private credit market has doubled in size over the last five years. It is now bumping up against the $2 trillion mark. Meanwhile, the private credit CLO market has been gaining ground. It is now projected to capture one-third of the CLO market by the end of the year. This is up from 11% in 2023.

Private Credit Returns

Over the past 18 years, private credit has also delivered the second highest annualized returns . It also has the lowest volatility of any asset class, across both fixed income and equities.

“We think middle market companies are still in a great position to benefit from our strong economy,” Bianco added. “They not only consistently provide higher yields than their larger publicly traded peers, but the middle market loan asset class also provides diversification benefits for investors.”

In the blink of an eye, Virtus Investment Partners launched its own Virtus Seix AAA Private Credit CLO ETF (PCLO ) on the same day. The fund charges 0.29%. It aims to invest in the highest-quality, "strongest and most undervalued” AAA-rated private credit CLOs, according to the company press release. To date, no AAA-rated CLO has ever defaulted before. PCLO may apportion a smaller slice of its net assets to publicly traded securities. These could include ETFs, senior loans, or junk bonds.

Both funds will invest at least 80% of total assets in CLOs backed by a pool of private credit loans.

More to Come

These moves mark the latest strides the ETF industry has taken to broaden its reach into the private asset pool. First to make waves was State Street’s September filing for a private credit ETF with Apollo. BlackRock’s recent acquisition of HPS Investment Partners has the world’s largest asset manager more than doubling its private credit business. This could mean big moves coming in the pipeline.

With more ETF issuers racing to brave the private market frontier, the landscape of ETF investing is poised for a transformative shift, which could redefine how investors approach private assets. Advisors will need to weigh the risks carefully. However, the potential for enhanced returns and portfolio diversification makes private credit CLO ETFs an exciting development. As with all private assets, there are also outstanding liquidity and pricing concerns. Both funds address those in their SEC filings. However, BondBloxx asserts that “CLOs are generally considered to be long-term investments and there is no guarantee that an active secondary market will exist or be maintained for any given CLO.”

For more news, information, and analysis, visit VettaFi | ETFDB.