S&P Global released its year-end 2024 SPIVA report, which measured actively managed fund performance against passive benchmarks. The report highlighted two areas where active management significantly outperformed, in both small-caps and investment-grade bonds.

The SPIVA Scorecard from S&P DJI measures active funds to their respective benchmarks. It spans equities and bonds across Australia, Canada, Europe, India, Japan, Latin America, the Middle East, South Africa, and the U.S. SPIVA research spans over 20 years, offering insights into active trends and short-term versus long-term performance compared to passive.

It is worth noting that active funds may outperform in the short-term in various categories. However, over longer time horizons, active management consistently underperforms. “Over the 15-year period ending December 2024, there were no categories in which a majority of active managers outperformed,” the SPIVA authors explained.

2024: A Difficult Year for Active Equity Strategies

In a year of megacap technology stock outperformance and widening sector dispersion, actively managed equity funds largely languished. Just seven of the 22 equity categories measured yielded active outperformance in 2024. S&P Global reported a 65% underperformance rate for active large-cap funds compared to the S&P 500 Index in 2024. Active midcap strategies faired only marginally better, with a 62% underperformance compared to the S&P Midcap 400 Index.

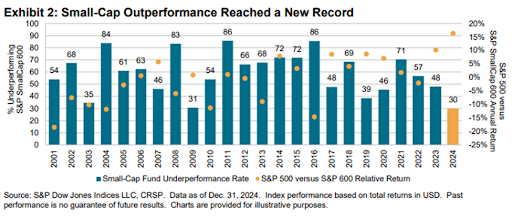

However, small-caps active strategies experienced their best year since SPIVA began tracking active management. In 2024, 70% of actively managed small-cap strategies outperformed the S&P SmallCap 600 Index.

This outperformance extended to international exposures as well. In the last year, only 43% of international small-cap strategies underperformed their benchmarks. For comparison, 84% of broad, active global funds fell below the S&P World Index’s performance in 2024. Emerging markets fared little better, at 71% underperformance compared to benchmarks.

Within equities, it seems relatively unsurprising that the categories with the largest performance disparities also offered the greatest outperformance potential for active management. The ability to not only select for more reliable performers but also divest of laggard stocks in small-caps can lead to notably differentiated performance.

Active Strategies More Successful in Bonds

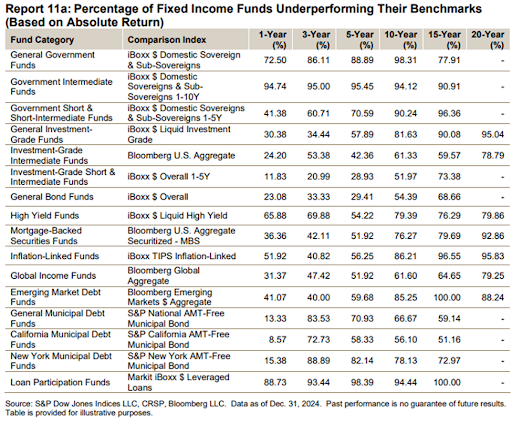

2024 proved a better year for active fixed income funds, with 11 out of 16 categories outperforming benchmarks on an absolute returns basis. That translated to a 41% underperformance rate last year across bonds. “The fortunes for U.S.-domiciled fixed income managers may have largely depended on which side of the credit or duration spectrum they landed on,” noted the authors.

The best performers within fixed income span an array of categories, reflecting the complex bond environment of 2024. Rising rates at the beginning of the year followed by rate cuts in the latter half of the year created a dynamic market environment.

The inverted 10-year and 2-year Treasury yield curve of the last two years reverted to normal last September, according to FRED data. Meanwhile, the Fed-preferred 10-year and 3-month Treasury yield curve also reverted to normal in December 2024, after two years of inversion. That measurement has since inverted again, as of the end of February 2025. Despite rising yields on long-term bonds, adding longer duration didn’t prove beneficial in 2024 for active managers.

In such an environment, 70% of broad, investment-grade active bond funds did better than their benchmarks in 2024. Strongest performing were short and intermediate investment-grade funds, at only 11.83% underperformance versus benchmarks. Actively managed municipal bond funds also proved notably consistent outperformers at 87%, compared to benchmarks. Emerging market debt did well, too, in 2024, compared to historical data, with 59% outperformance by active strategies.

Laggards within active fixed income included government intermediate funds at a staggering 95% underperformance rate. This proved a drag on the broad category, with only 27.5% of actively managed government funds outperforming. Actively managed high yield strategies also underperformed at 66% compared to benchmarks.

For more news, information, and strategy, visit ETF Trends.