As investors flood back into bonds on rising economic uncertainty, there’s benefits to looking beyond the benchmarks. With nearly half of the bond market now outside of the Agg, a number of opportunities exist for those seeking diversification in their fixed income portfolio.

While the Bloomberg U.S. Aggregate Bond Index covers an expansive range of sectors and securities, the rules of the benchmark index exclude a significant number of bonds. David Vick, CFA, managing director, head of fixed income portfolio specialists multi-sector at TCW noted in a recent paper that nearly 47% of fixed income securities aren’t found within the Agg.

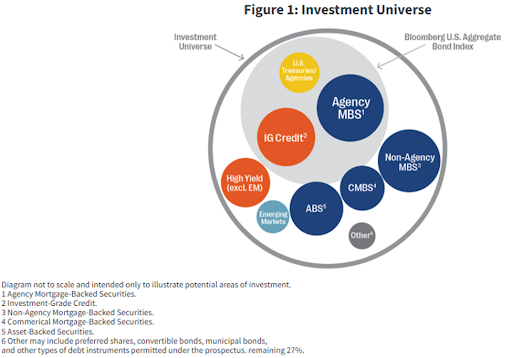

“The big issue is that the Agg only includes bonds that are rated investment grade, publicly registered, have a fixed rate coupon, at least a year of maturity remaining, are denominated in U.S. dollars, and meet certain minimum size requirements,” Vick explained.

The U.S. Bond Universe Outgrows Its Benchmark

The Agg’s methodology currently limits exposures to investment-grade securities and those with a fixed rate coupon. It limits sector exposures to Treasuries, corporate, government-related, and securitized — mortgage-backed securities, asset-backed securities, covered, and commercial mortgage-backed securities. Fixed income securities included in the Agg must also have at least one year until final maturity.

That leaves out a wide swathe of bonds that include TIPS, money markets, and floating rate securities such as collateralized loan obligations (CLOs). It also excludes high yield and other below-investment grade bonds, and non-U.S. dollar denominated bonds. Collectively, fixed income securities beyond the Agg make up approximately $26 trillion just in the U.S.

“This isn’t the first time that a market outgrew an index,” noted Vick. “The Nasdaq Composite, for example, became more influential when the traditional companies contained in the Dow Jones Industrial Average didn’t reflect the growing investor focus on technology.”

In a challenging economic and market environment, looking beyond the traditional bond benchmark may prove beneficial for investors. However, many of the sectors beyond the Agg carry higher risk profiles, or require greater expertise before investing. For example, when high yield bond investing, understanding not only what metrics matter more, but also the relation of earnings and the economic environment, matters.

Active May Provide Solutions for Investing Beyond the Agg

It’s what makes actively managed strategies particularly appealing for bond sectors outside the Agg. Advisors and investors can tap into the knowledge and experience of active fund managers. For advisors, this frees up valuable resources. And for investors, it may provide peace of mind to know that more complex investments are handled by experienced, knowledgeable portfolio managers.

Diversifying beyond the bond benchmark may prove advantageous for investors looking ahead. Whether the Agg’s rules and methodology ever expand to cover more sectors and bond types is unknown. However, Vick outlined the growing exposure of the Agg to Treasuries due to rising budget deficits.

With U.S. budget deficits likely to grow in the coming months and years, the Agg will only take on greater weight to Treasuries. It also limits upside potential for the benchmark index. “In essence, that means investors may be leaving money on the table,” explained Vick.

For more news, information, and strategy, visit "ETFdb":http://etfdb.com.