A large consensus has been to stay the course with long-term portfolio goals despite recent tariff volatility. While this is generally true, short-term fluctuations still matter. We have had plenty of those recently — by the time you read this note, the market could be either up or down. Regardless, it’s still important to talk about these fluctuations — even if they do disappear in the long term. These are some thoughts on why investors need to pay attention to tariffs, implications for the market and ETFs, and what this could mean for the future.

Fundamentals vs. Sentiment: Both are important.

There is a never-ending battle between fundamentals and sentiment. Many investment professionals stand by fundamentals (i.e., examining information like a company’s earnings statements and macroeconomic data to forecast long-term growth). While sentiment is not always based on real facts, its effect on portfolios is always real. It is easy to brush off sentiment because of this and urge investors to look long term. But short-term fluctuations are difficult emotionally (red is an infuriating color to see). Part of investment research is providing investment recommendations. But it’s also providing education on why the market makes moves and what precedent is set for the future.

Uncertainty persists – expect more wild swings.

Right now, tariffs are synonymous with uncertainty. There are many layers to the tariffs — baseline, reciprocal, retaliatory, certain items have separate tariffs, certain items are exempt, etc. It is also uncertain how much can be negotiated and how much is set in stone. We recently saw the extreme side of it when China was hit with a 125% tariff (and we were hit with an 84% tariff in return). With all of these moving parts, it is almost impossible to parse the total economic impact. Companies, e.g., Delta Airlines (DAL), are starting to cut or withdraw their full-year outlooks. In the investment world, the unknown can have an even bigger impact than the known. Until we have more certainty on the impact, the market will likely see these wide swings and continue to be news driven.

Not all equities are built the same.

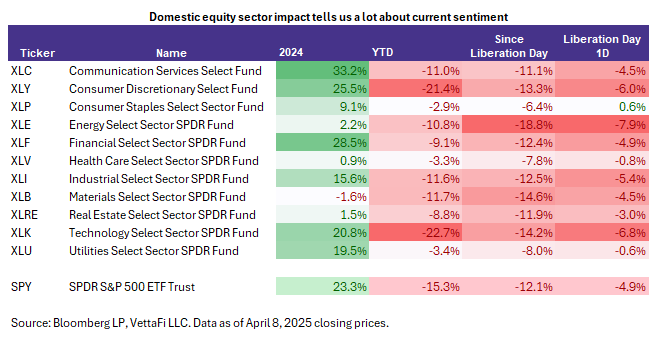

Broadly, U.S. equities have fallen even further after a tough 1Q. While it has been red across the board, certain sectors have been more affected than others. Growthier sectors like technology and consumer discretionary tend to pull back whenever there is economic weakness. That is the case here, but technology and consumer discretionary stocks also have the added factor of heavily leaning on manufacturing — particularly in Asia. Year to date, the Technology Select Sector SPDR Fund (XLK ) was down 23% YTD. The Consumer Discretionary Select Sector SPDR Fund (XLY ) was down 21%.

On the discretionary side, Nike (NKE), for example, has over 50% of its products produced in China and Vietnam. On the technology side, it’s interesting to note that semiconductors are exempt from reciprocal tariffs. But end products that use semiconductors, like Apple (AAPL) iPhones are affected by tariffs. And that results in a secondary effect. The VanEck Semiconductor ETF (SMH ) is down 26% YTD despite being a recent investor favorite in 2024.

On the defensive side, it is more about resilience rather than opportunities — and consumer staples, healthcare, and utilities have been somewhat resilient. The Consumer Staples Select Sector SPDR Fund (XLP ) is down only 3% YTD. The dynamic between staples and discretionary is always interesting during economic swings. That is because consumer staples businesses typically have more pricing power and can pass on those higher costs. Consumers typically cut back on discretionary spending in favor of essentials.

What does this mean? Even if you don’t have specific allocations to technology or discretionary names, be wary of overexposure to broad domestic equity ETFs, which typically have a heavy concentration to these sectors. For example, the SPDR S&P 500 ETF Trust (SPY ) has a 29% weight to technology. And the Vanguard Total Stock Market ETF (VTI ) has a 33% weight to technology.

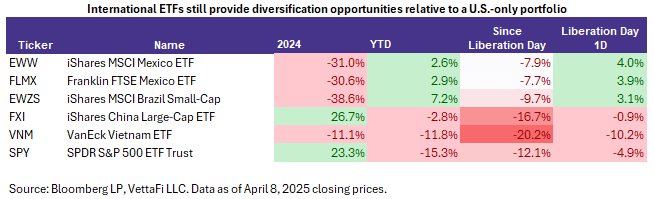

1Q put more eyes on international — now that’s getting more complex.

While the U.S. market saw a pullback in 1Q, international equity was thriving. Now international markets are also seeing a pullback. For reference, most of the deeply affected international ETFs are those with the highest tariffs — China and Vietnam. The iShares China Large-Cap ETF (FXI ) is down 17% since April 2. And the VanEck Vietnam ETF (VNM ) is down 20% during the same period. On a year-to-date basis, however, the pullback is less severe relative to the U.S. Year to date, FXI is down 3%, VNM is down 12%, and SPY is down 15%.

Some resilient spots exist internationally. Mexico — along with Canada — escaped the broad-based tariffs due to some existing trade agreements in North America. The iShares MSCI Mexico ETF (EWW ) is currently up 3% YTD. Additionally, the iShares MSCI Brazil Small-Cap ETF (EWZS ) is up 7% YTD. Brazil escaped with “only” a 10% tariff. That gives it an edge, assuming it can take advantage of its position this year.

International exposure will be a test for retail investors. With many retail investors recently adding to their international exposures in 1Q to counter the U.S. equity pullback, they may be tempted to exit. But note that YTD, most international equity has still held up better than U.S. equity, and diversification shouldn’t be timed for convenience.

Diversifiers work.

Also regarding diversification, Todd Rosenbluth, VettaFi’s head of research, recently wrote a note on portfolio diversifiers. As with international equities, hindsight is always 20/20. Investors often think of buying diversifiers after the fact instead of holding steady in a portfolio. It is recommended to hold a diversified portfolio to weather through all cycles of the economy — not just after the fact. While gold — the most well-known safe haven asset — also fell during the initial sell-off, it has held up more resiliently relative to equities. The SPDR Gold Shares (GLD ) is up 14% year-to-date.

Opporunities to buy the dip (or 3x that).

It is rational to be afraid of volatility, but volatility can also create more opportunities. For certain areas that have strong long-term fundamentals — like semiconductors — the pullback could be an opportunity to buy the dip. Notably, Cathie Wood is finally buying Nvidia (NVDA) again for her flagship ARK Innovation ETF (ARKK ).

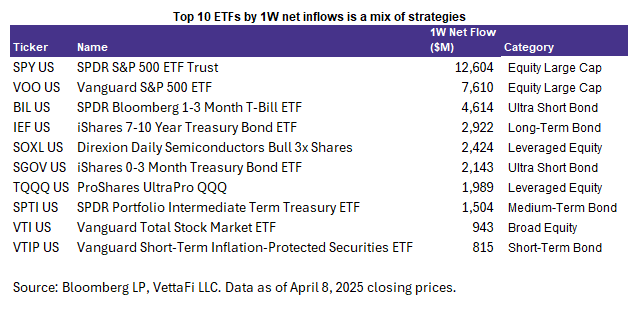

Additionally, some traders and investors are embracing the volatility and piling into leveraged products. The ProShares UltraPro QQQ (TQQQ ) and the Direxion Daily Semiconductors Bull 3x Shares (SOXL ) — both 3x leveraged ETFs — saw a large amount of inflows earlier this week. For certain investors, making a leveraged bet in a market with wide swings is more attractive than simply buying the dip.

ETFs provide many of these tools to investors.

Whether investors are hedging their risks or buying the dip, ETFs continue to be an attractive investment choice across various strategies. U.S. ETFs saw $24.7 billion in net inflows over the past week with a mix of equities, fixed income, and even 3x leveraged plays.

Final Thoughts: Are tariffs good or bad?

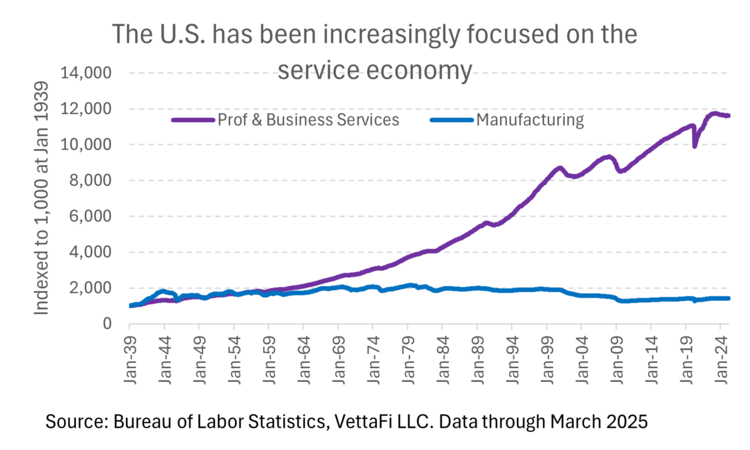

I don’t believe tariffs are good or bad. They are tools to control imports, manufacturing and supply chain footprints and theoretically can boost long-term growth. But this doesn’t come easy. The long-term trend has been moving from offshoring to nearshoring to reshoring. Offshoring was very popular for many years. It provided cheap labor and access to different parts of the global markets (i.e., access to more growth areas), while the U.S. focused on high value service sector jobs.

This started trending to nearshoring, or moving manufacturing to nearby areas like Mexico, where labor is still cheap but supply chains are more efficient. From there, the pandemic was a catalyst to reshoring — returning manufacturing directly to the U.S. The argument here was that we needed to bring back manufacturing jobs to the U.S. and simplify supply chains to avoid disruption. While U.S. labor costs more than foreign labor, other potential benefits may counteract the costs; for example, cheaper transportation costs, reduced U.S. trade deficit and a stronger U.S. dollar.

But implementation is often difficult. I spent a large part of my career analyzing supply chain companies, and supply chains are complex and don’t change overnight. Companies must deal with higher shipping costs, which eat into profits and earnings. They can also pass those costs to consumers, who ultimately suffer from pricing inflation. So, while tariffs are neither good nor bad, there are complexities that come with rapidly reshoring. And there are still a lot of uncertainties with how that implementation will work.

Bottom Line: While the best action is typically to stick to long-term goals, short-term fluctuations do matter. They help us decide what tactical allocations to make — whether that is to hedge our current portfolio or add to existing holdings. And they also set a precedent to prepare us better for the next big market event.

For more news, information, and strategy, visit ETFDB.