Investors typically diversify global portfolios with broad international ETFs. But recent market volatility has caused investors to look more closely at various international opportunities. Some of the top-performing ETFs this year are European, including some individual-country ETFs and some broader European sector ETFs: Poland, Germany, Spain, European defense, and European financials. This note takes a look at the top-performing international ETFs, what they hold, and other interesting facts about these ETFs.

Select STOXX Europe Aerospace & Defense ETF (EUAD)

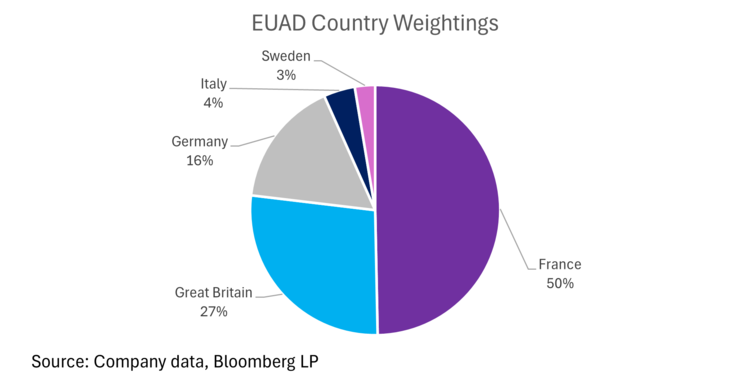

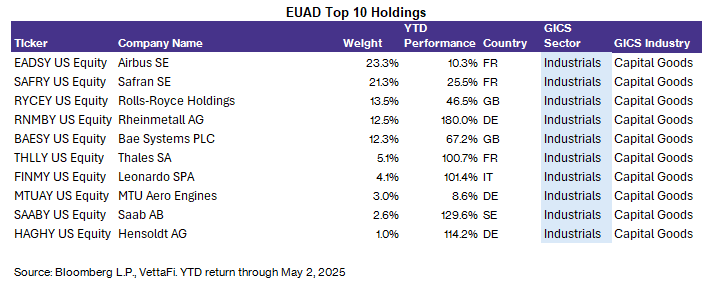

European defense has taken off as geopolitical tensions have increased and Europe plays “catch-up” with the U.S. on defense spending. In a previous note, I discussed this industry in detail. EUAD is the only pure-play U.S.-listed ETF that tracks the European defense sector. The ETF has only 13 holdings (these are American depositary receipts). Its top 5 holdings make up 83% of the ETF’s weight.

Its top holding is Airbus SE (EADSY) followed by Safran SA (SAFRY) — both French companies. The ETF has a heavy tilt toward France (50% of its weight) along with significant weight in Great Britain (27%) and Germany (16%). Broadly, all 13 of its holdings have been up YTD. However, several have seen YTD returns over 100%, including Rheinmetall AG (RNMBY) and Hensoldt AG (HAGHY).

EUAD has been up 52% so far YTD, with about $570 million net inflows. This ETF is relatively new (launched October 2024). Close peers (while not pure-play) include the Global X Defense Tech ETF (SHLD ) and the Themes Transatlantic Defense ETF (NATO ). Both have a significant exposure to European defense. But these two ETFs are largely U.S.-based (particularly SHLD which is over 50% U.S. stocks).

iShares MSCI Poland ETF (EPOL)

EPOL is up 44.2% YTD and has been almost consistently in the top performers this year. Poland is a relatively small market that is on the cusp of emerging and developed. It has strong growth prospects due to its central location and economic and political stability. The country has flown relatively under-the-radar, however, since Poland’s stocks are not really household names for the U.S. investor.

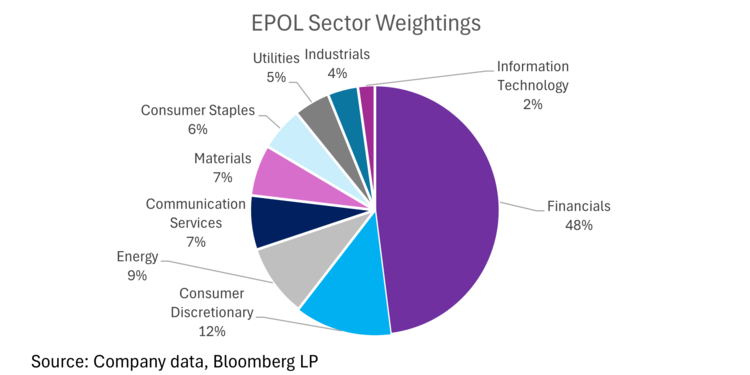

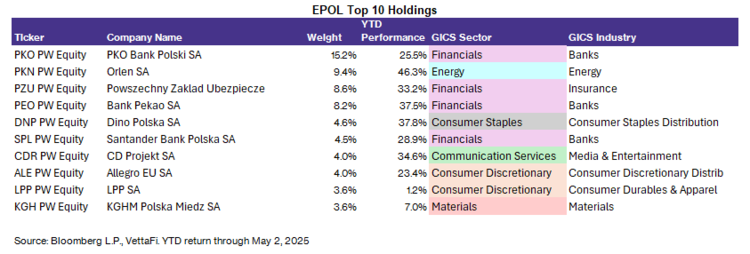

Despite its performance this year, it has only attracted around $116 million in net inflows. The fund has a total of $396 million in assets. Interestingly, 48% of the ETF is financials, followed by 13% consumer discretionary stocks. All but two of its 32 holdings are up YTD (and these two stocks are down only single digits). Most of its holdings are up double-digit percentages, including its top holding PKO Bank Polski (PKO PW), which has a 15% weight.

EPOL serves as a good option for investors wanting exposure to Poland as an under-the-radar opportunity. Currently, no other ETFs track this country. A competing fund — the VanEck Vectors Poland ETF (PLND ) — was closed in 2019. Additionally, broader international funds have very little to no exposure to Poland.

First Trust Germany AlphaDEX Fund (FGM)

FGM is up 34% YTD, yet has only $5 million in net inflows. Unlike most of the ETFs discussed in this note, there are several peer ETFs in this group. FGM is actually the smallest of its peers, with only $15 million in assets (which explains its low inflows). The iShares MSCI Germany ETF (EWG ) is the largest, with $2.4 billion in assets, with $1.3 billion in net inflows this year so far. Additionally, the Global X Dax Germany ETF (DAX ) and the Franklin FTSE Germany ETF (FLGR ) round out the group.

All three of FGM’s peers have similar YTD returns — around 27%, But, notably, FLGR has an expense ratio of only 9 basis points — very low compared to many other country ETFs. Most of the popular iShares country ETFs, for example, cost around 50 basis points. FGM has outperformed recently due to its methodology, which isn’t a traditional market capitalization weighting. This ETF uses the AlphaDEX stock selection methodology, which includes both growth and value factors.

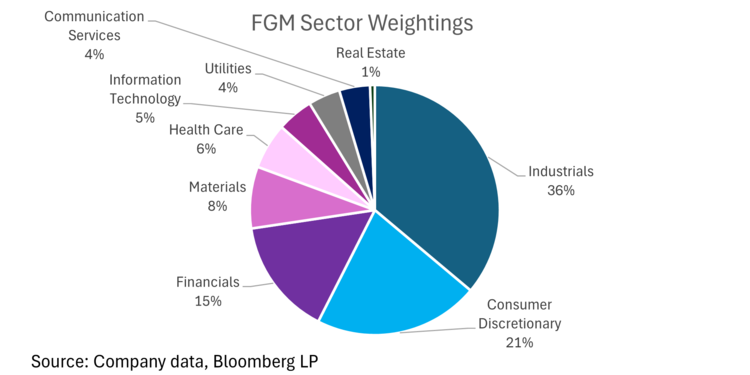

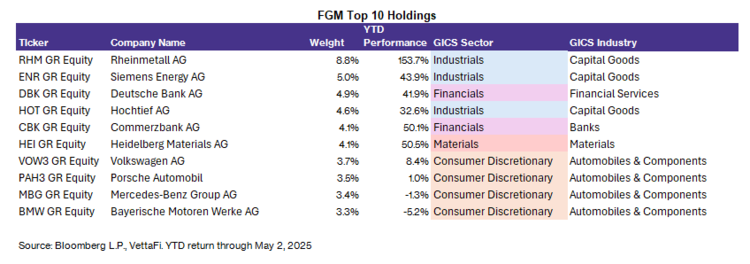

FGM is 36% industrials, 21% consumer discretionary, and 15% financials. Many of FGM’s top holdings are more common, household names including some of the large auto companies — Volkswagen AG (VOW3 GR), Porsche Automobile (PAH3 GR), and Mercedes-Benz Group (MBG GR), for example. While performance in the auto stocks has been lackluster due to tariff concerns, most of its other holdings are up YTD. Its top holding, Rheinmetall AG (RHM GR), which is a well-known European defense company, is up 154% YTD.

iShares MSCI Spain ETF (EWP)

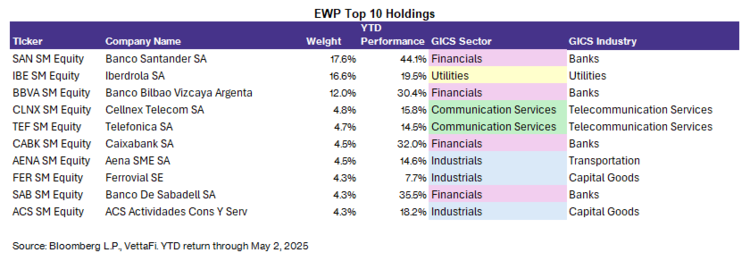

EWP is up 32% YTD, with around $100 million net inflows YTD. Since this is the only Spain ETF, it is relatively large, with around $1.2 billion in assets. It holds 17 stocks, including some well-known multinational banks. Its top holding, Banco Santander (SAN SM) has a weight of 17.6% and is up 44% YTD. Its third-largest holding is also an easily recognizable global bank, called Banco Bilbao Vizcaya Argentaria BBVA. (If that sounds familiar, its U.S. arm, BBVA, was acquired by PNC in 2021.) Like Banco Santander, BBVA is up 30% YTD on strong earnings and positive investor sentiment.

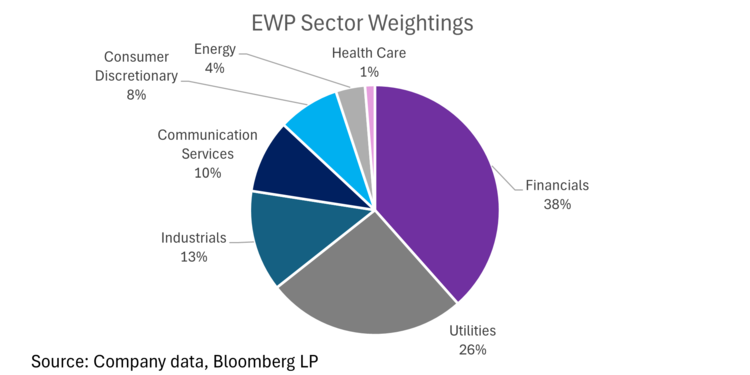

Aside from the banking industry, Spain’s economy is also known for its well-developed infrastructure. Likewise, EWP has a strong tilt toward defensive sector and infrastructure names, including 38% financials, 26% utilities, and 13% industrials. It has no allocation to technology (much like most European ETFs), which is a stark contrast versus the U.S. domestic market.

iShares MSCI Europe Financials ETF (EUFN)

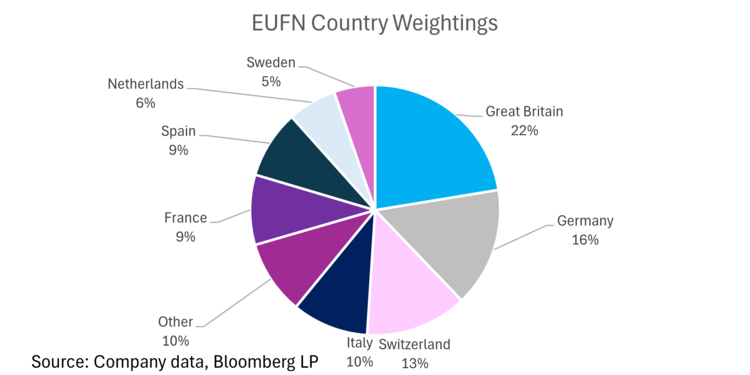

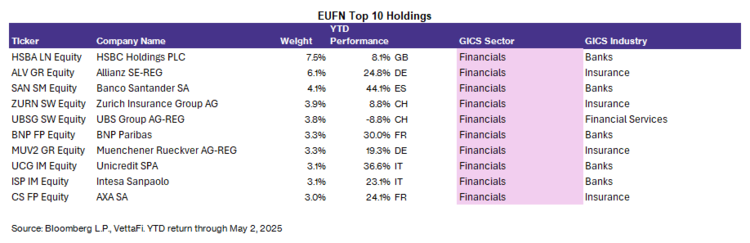

There aren’t many European sector ETFs besides EUAD and EUFN. While EUAD was launched last year, EUFN launched in 2010, which illustrates interest in this sector has been around for a while. So far the ETF has been up 30% YTD, with over $800 million in net inflows. Europe is known for its strong financial center. And despite its strength, this sector isn’t well-represented within global financials ETFs. The iShares Global Financial ETF (IXG ) is 54% U.S. Its largest European allocation is to the UK, with only 6%. (Also notable — EUFN is actually much larger than IXG despite having a narrower focus. EUFN has $3.2 billion in assets, while IXG has less than $500 million).

EUFN is also relatively diversified across countries. Its largest allocation is to Great Britain (22% of the ETF’s weight), followed by Germany (16% weight), and Switzerland (13%) weight. Additionally, EUFN is 49% — almost half — weighted toward banks. But other industries like insurance (29% of weight) and financial services (21%) are also strong. EUFN’s second-largest holding is the well-known insurance company Allianz (ALV GR), which has so far been up almost 25% YTD.

Bottom Line:

When looking for opportunities in the global equities market, an allocation to country ETFs or regional sector ETFs can help support a tactical approach to international investing. These areas are often not represented in broader global ETFs and can provide investors with additional opportunities beyond traditional international ETFs.

For more news, information, and analysis, visit VettaFi | ETFDB.